If you had asked me two years ago how I was doing with my finances, I’d have given you a confident smile and said, “Just fine, thank you.” And on the surface, that was true. My pension came in like clockwork, Social Security was reliable, and I lived in the same comfortable house my late wife, Clara, and I had paid off years ago. I thought I had it all figured out. But underneath that calm surface, a quiet panic was starting to bubble up. Every month, it felt like my checking account was evaporating, and I couldn’t figure out where the money was going.

The truth is, I was grappling with a classic case of overspending in retirement, but I was too proud to admit it, even to myself. This isn’t a story about fancy financial formulas or complex investment schemes. It’s the simple, honest story of how I confronted my spending habits and, in the process, found a level of peace of mind I hadn’t realized I was missing.

This is my personal story and is for informational or entertainment purposes only. It is not intended to be financial advice. Please consult with a qualified financial professional for advice tailored to your individual situation.

The Quiet Panic of an Empty Checking Account

For forty years, Clara had been our family’s Chief Financial Officer. She had a knack for it, with her little notebooks and her careful tracking of every dollar. After she passed, I took over the bills, and for the first few years, things seemed to run smoothly. I paid everything on time, and there was always enough money. Or so I thought.

The problem was, I wasn’t just paying the bills. I was also filling the empty hours. Loneliness is a funny thing; it can make you do things you don’t even notice. For me, it meant more lunches out at the local diner, just to have some company. It meant buying the latest gadget I saw advertised on TV, thinking it might be a fun new hobby. It meant keeping the premium cable package with a thousand channels I never watched, just in case. Each purchase was small, insignificant on its own. A $15 lunch here, a $40 gadget there. What was the harm?

The “uh-oh” moment, the one that finally snapped me out of my comfortable denial, came in the form of a beautiful, cream-colored envelope. It was an invitation to my eldest granddaughter’s wedding. I was overjoyed, my heart swelling with pride. I immediately started dreaming of the generous gift I wanted to give her and her new husband to help them start their life together. I imagined writing a check that would really make a difference for their down payment on a house.

Later that day, I sat down at my desk and logged into my online banking portal, ready to see what I could set aside. I clicked on my checking account, and the number staring back at me was a shock. It was far, far lower than I had expected. After the mortgage (which was paid), property taxes, and utilities were accounted for, there was barely anything left. I clicked over to my savings account, and my stomach dropped. It hadn’t grown an inch in over a year. In fact, I’d dipped into it twice for “minor emergencies” that were probably just poor planning.

The joy I felt about the wedding curdled into a cold, heavy dread. How could I, a man who had worked his whole life and owned his home, be in this position? The idea of giving my granddaughter a simple toaster when I had dreamed of giving her a nest egg was humiliating. It wasn’t about the money itself; it was about what it represented. It felt like I was failing, not just her, but Clara’s memory, too. That night, I knew I couldn’t keep pretending everything was “just fine.”

My Date with Three Highlighters and a Hard Truth

Admitting you have a problem is one thing; figuring out what to do about it is another. For a full week, I just stewed in my anxiety. I felt ashamed. I’m from a generation where you didn’t talk about money troubles. You just buckled down and handled it. But I didn’t even know what “it” was.

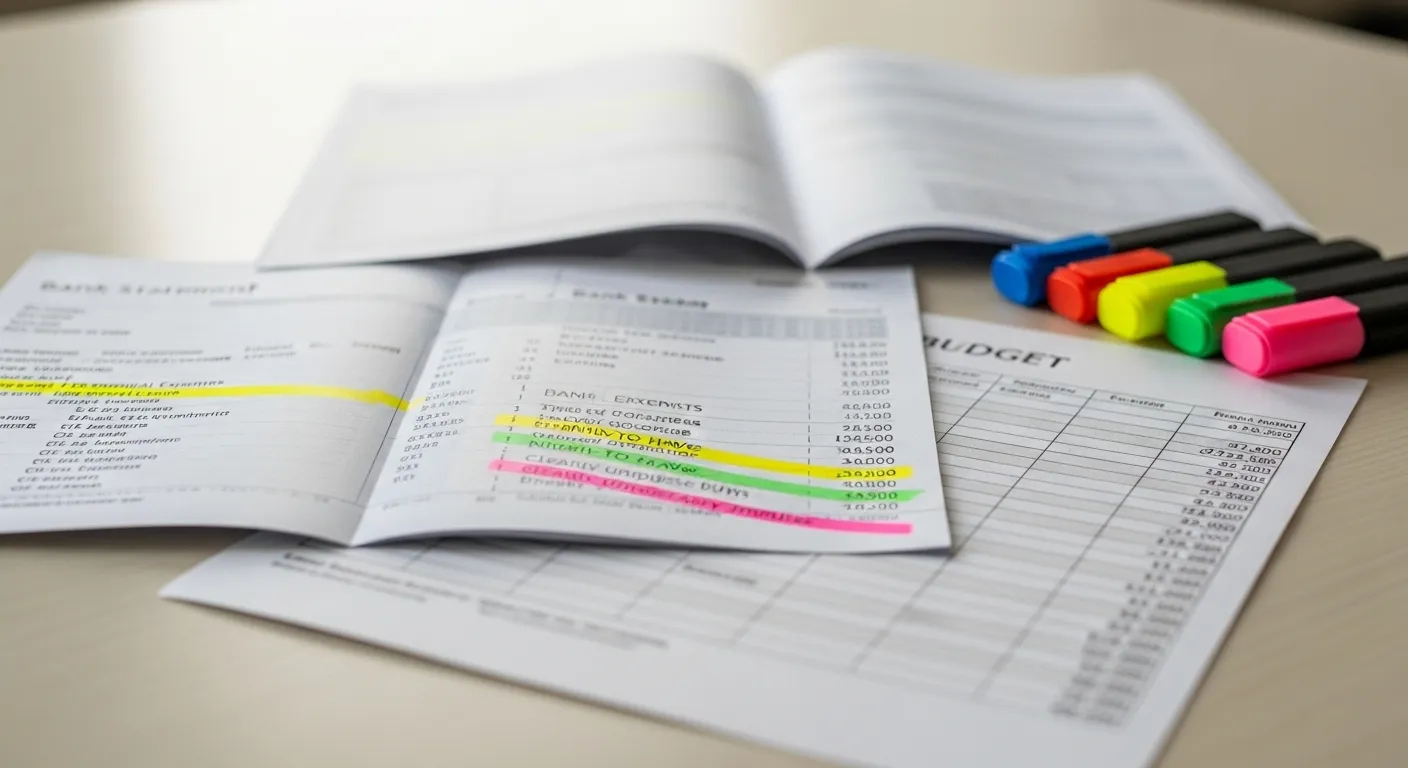

My first concrete step felt almost silly, but it turned out to be the most important one I took. I went to the office supply store and bought a pack of three highlighters: green, yellow, and red. Then, I went online and printed out the last three months of my credit card and bank statements. I spread them all out on the dining room table, the same table where Clara used to do her books, and poured myself a strong cup of coffee. This was my day of reckoning.

My system was simple:

- Green: Essential, non-negotiable expenses. Property taxes, utilities, insurance, groceries.

- Yellow: Things that were nice but not strictly necessary. My monthly lunch with my old work buddies, the basic cable package, a reasonable haircut.

- Red: The “what was I thinking?” expenses. The impulse buys, the daily diner trips, the streaming services I’d forgotten I’d subscribed to, the premium movie channels.

As my highlighters moved across the pages, a painful picture began to emerge. The sea of green was what I expected. The yellow was manageable. But the amount of red on those pages was staggering. It was a bloodbath of tiny, thoughtless purchases. I added it all up. The daily coffees and lunches alone were costing me over $250 a month. The unused subscriptions and premium channels were another $80. The random online purchases for things I used once and then forgot? That was another $100 or more some months. I wasn’t just overspending; I was hemorrhaging money on things that brought me fleeting, momentary satisfaction at best.

Seeing it all in black and white (and red) was brutal. There was no one else to blame. It was all me. But strangely, after the initial wave of shame passed, I felt a flicker of something else: control. The enemy wasn’t some mysterious force; it was right here on the paper in front of me. And if I could see it, I could fight it.

From Unconscious Spending to a Conscious Budget

My goal wasn’t to live like a monk. Retirement is supposed to be enjoyed, after all. My goal was to stop the unconscious spending and become a conscious spender. I needed a new plan, a proper retirement budgeting system that worked for me. I didn’t want to go back to Clara’s detailed notebooks—that wasn’t my style. I needed something simpler.

First, I tackled the “red” list. I spent an entire afternoon on the phone. I called the cable company, and with a bit of polite but firm negotiation, I downgraded to a basic package that still had my favorite news and sports channels, saving me $65 a month instantly. I logged into my computer and canceled three streaming services I hadn’t watched in months. That was another $45 back in my pocket. Total saved: $110.

Next was the food situation. I loved the camaraderie of the diner, but I had to admit it was a crutch. I made a new rule for myself: I could eat out with friends once a week, no more. For my other meals, I started planning. I rediscovered the joy of cooking, something Clara and I used to do together. I found it was a wonderful way to fill the late afternoons. I started making big batches of chili or soup that would last for several meals. This change alone, I estimated, would save me at least $150 a month. Total saved so far: $260.

The final piece of my monthly savings strategy was the most important. It was proactive, not reactive. I went to my bank and set up an automatic transfer. On the third of every month, the day after my Social Security was deposited, I had $300 moved automatically from my checking account into my savings account. The key was to “pay myself first.” By moving the money before I had a chance to spend it, it was out of sight, out of mind. It forced me to live on the rest, which, after my budget cuts, was more than enough.

The Surprising Richness of a Simpler Life

The first month was the hardest. I’d walk by the diner and my feet would almost turn in automatically. I’d see an ad on TV and have to physically stop myself from grabbing my tablet to look it up online. But I stuck with it. When I felt lonely, instead of going out to eat, I’d call my son or invite my neighbor, Bob, over for a coffee that I brewed myself. It turned out our conversations on my porch were just as good, if not better, than the ones at the diner, and a whole lot cheaper.

After three months of my new plan, I logged into my bank account again. This time, there was no dread. I looked at my savings account, and there it was: an extra $900. It felt like I had won the lottery. I hadn’t earned more money; I had simply become a better steward of what I already had. The feeling wasn’t just relief; it was empowerment.

When my granddaughter’s wedding day arrived, I was able to write her a check that made my heart sing. It wasn’t a fortune, but it was a meaningful, generous gift that I could give freely, without an ounce of financial worry. Seeing the look on her face was worth more than a thousand diner lunches.

Today, two years later, that automatic transfer is still happening every month. Saving money in retirement has become a habit, not a struggle. My savings account is healthier than it has been in a decade, and that security has given me a different kind of richness. It’s the richness of peace. It’s the freedom to say “yes” to a last-minute trip to see the grandkids, the comfort of knowing I can handle a surprise repair bill, and the quiet confidence of being in control of my own life.

If you’re in a situation like I was, my advice is simple. Don’t be ashamed. Be honest with yourself. Get those bank statements, grab a few highlighters, and face the truth. You might be surprised to find that a life of financial security isn’t about earning more—it’s about spending with purpose on the things that truly matter.

For expert guidance on senior health and finance, visit Alzheimer’s Association, American Heart Association and Benefits.gov.

|

Fact-Checked Content

Our editorial team reviews all content for accuracy and updates it regularly. Learn about our editorial process →

|

Leave a Reply