Navigating taxes in retirement feels like learning a brand-new language, but mastering it keeps more of your hard-earned money in your pocket. Once you leave the workforce, the rules governing how your income is taxed completely change, often leaving seniors overpaying the government simply because they do not know their options. The tax code is packed with hidden deductions, special age-based exemptions, and strategic loopholes specifically designed to benefit older adults. By understanding these lesser-known strategies, you can legally reduce your taxable income, protect your retirement savings, and stretch your monthly budget further. Let us explore the most powerful tax-saving strategies you can start using today to secure your financial independence.

Secret 1: Your Social Security Benefits Might Be Completely Tax-Free

Many retirees assume that because they paid taxes on their income during their working years, their Social Security benefits will be completely tax-free. Unfortunately, this is not a blanket rule; however, with careful planning, you can legally shield a significant portion—or even all—of your benefits from the IRS.

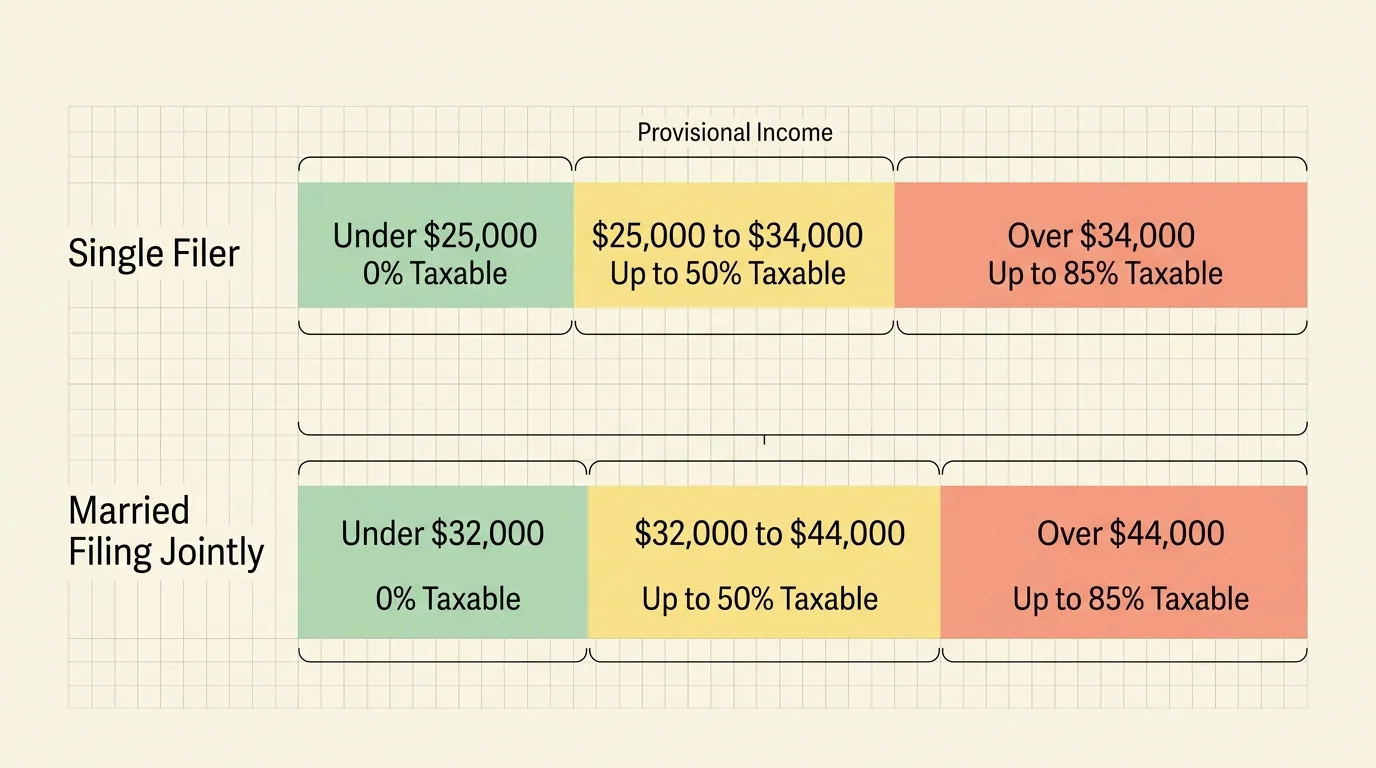

The IRS uses a specific formula called “Provisional Income” to determine if your Social Security is taxable. To calculate your provisional income, you take your Adjusted Gross Income (AGI), add any nontaxable interest you earned (like municipal bonds), and then add exactly half of your yearly Social Security benefits.

According to the Social Security Administration (SSA), if your combined provisional income falls below certain thresholds, you owe zero federal income tax on your benefits. If you cross these lines, up to 85% of your benefits become taxable. Understanding these limits is critical for managing your withdrawals from other retirement accounts.

| Filing Status | Provisional Income Threshold | Amount of Benefits Subject to Tax |

|---|---|---|

| Single Filer | Under $25,000 | 0% |

| Single Filer | $25,000 to $34,000 | Up to 50% |

| Single Filer | Over $34,000 | Up to 85% |

| Married Filing Jointly | Under $32,000 | 0% |

| Married Filing Jointly | $32,000 to $44,000 | Up to 50% |

| Married Filing Jointly | Over $44,000 | Up to 85% |

To keep your provisional income low, consider drawing from a Roth IRA for your living expenses. Because Roth IRA withdrawals are completely tax-free, they do not count toward your provisional income. This simple adjustment can keep you below the threshold and protect your Social Security checks.

Secret 2: You Get a Bigger Standard Deduction Just for Turning 65

Reaching your 65th birthday comes with several financial milestones, and one of the most immediate benefits is an automatic tax break from the IRS. The standard deduction is a specific dollar amount that reduces the income you must pay taxes on. For seniors, the IRS offers an “extra” standard deduction simply for aging.

If you or your spouse is 65 or older at the end of the tax year, you are entitled to a higher standard deduction amount than younger taxpayers. If both you and your spouse are 65 or older and file a joint return, you get to claim this additional amount twice. This is particularly helpful because it reduces your taxable income right off the top, without requiring you to itemize complicated deductions.

To ensure you receive this benefit, you must check the specific boxes on Schedule 1 of Form 1040 that indicate your age or your spouse’s age. Many seniors who use automated tax software miss this entirely if their birthdate is entered incorrectly. Always double-check your return before filing to confirm your standard deduction matches the higher senior rate.

Secret 3: Medicare Premiums Count as Deductible Medical Expenses

Healthcare is often one of the largest expenses in retirement. While the IRS allows you to deduct out-of-pocket medical expenses, you can only do so if they exceed 7.5% of your Adjusted Gross Income (AGI). For many people, crossing this 7.5% threshold seems impossible, but retirees have a distinct advantage: Medicare premiums count toward this total.

According to Medicare.gov, your regular premiums for Medicare Part B (medical insurance), Part D (prescription drug coverage), and even Medicare Advantage plans are completely eligible as deductible healthcare expenses. When you combine these ongoing premiums with your co-pays, dental work, vision care, and hearing aids, reaching the 7.5% threshold becomes much easier.

Keep a diligent record of these eligible expenses throughout the year:

- Monthly Medicare Part B and Part D premiums deducted directly from your Social Security checks.

- Out-of-pocket costs for prescription medications and insulin.

- Payments for eyeglasses, eye exams, and contact lenses.

- Costs associated with hearing aids and their maintenance.

- Home modifications required for medical reasons, such as installing a wheelchair ramp or grab bars in your shower.

If you plan a major medical expense—like elective joint surgery or purchasing expensive hearing aids—try to bundle those expenses into a single calendar year. By stacking your medical costs, you maximize your chances of easily exceeding the 7.5% limit and unlocking a massive tax deduction.

Secret 4: You Can Give to Charity and Skip the Tax Bill Completely

Once you reach age 73, the IRS mandates that you begin taking Required Minimum Distributions (RMDs) from your traditional IRAs and 401(k)s. This forced income is fully taxable and can push you into a higher tax bracket, causing a frustrating chain reaction that might increase your Medicare premiums and the taxes on your Social Security benefits.

However, there is a brilliant workaround for charitably inclined seniors: the Qualified Charitable Distribution (QCD). A QCD allows you to transfer funds directly from your IRA to a qualified IRS-approved charity. Because the money goes straight to the charity, it is never counted as taxable income to you—yet it fully counts toward satisfying your RMD for the year.

To execute a QCD properly, follow these strict rules:

- You must be at least 70½ years old to make a QCD, even though RMDs do not start until 73.

- The funds must be transferred directly from your IRA custodian to the charity. If the check is made payable to you and you deposit it first, the tax benefit is completely lost.

- You can transfer up to a specific annual limit (which is indexed for inflation, reaching over $100,000 per year) without paying a dime in federal taxes on the distribution.

This is a powerful tool for seniors who want to support their favorite causes, tithe to their church, or fund local community programs without unnecessarily inflating their own taxable income.

Secret 5: Working Past 73 Can Pause Your Required Minimum Distributions

If you love what you do and decide to continue working past the traditional retirement age, you might be dreading the mandatory taxes that come with Required Minimum Distributions. Many seniors assume that turning 73 means you must drain your retirement accounts no matter what. This is true for traditional IRAs, but workplace retirement plans have a secret escape hatch.

If you are still employed at age 73 and beyond, you can generally delay taking RMDs from your current employer’s 401(k) or 403(b) plan until you officially retire. This is known as the “still working” exception.

There are a few critical caveats to this rule. First, it only applies to the retirement plan of the company you are currently working for; you still have to take RMDs from any traditional IRAs or 401(k)s left behind at previous employers. Second, you cannot own 5% or more of the company you work for. If you are a business owner or partner, this exception does not apply to you.

By leaving your funds in your current employer’s 401(k) while you continue to earn a salary, your investments enjoy more time to grow tax-deferred, and you avoid compounding your tax burden during your highest-earning final years of employment.

Secret 6: Downsizing Your Home Can Yield Massive Tax-Free Cash

Your home is likely one of your largest assets. If you are considering downsizing to a smaller property, moving into an active adult community, or relocating closer to your grandchildren, you might be worried about the capital gains taxes associated with selling a home that has appreciated in value over several decades.

The IRS offers an incredibly generous tax break for homeowners known as the Section 121 exclusion. If you sell your primary residence, you can exclude up to $250,000 of the profit from your taxable income if you file as a single taxpayer. If you are married and filing jointly, that exclusion doubles to a massive $500,000.

To qualify for this tax-free windfall, you must pass the “ownership and use” tests. You must have owned the home and lived in it as your primary residence for at least two out of the five years immediately preceding the sale. The two years do not even need to be consecutive.

This means you can sell your family home, pocket hundreds of thousands of dollars in pure profit, and pay absolutely zero federal income tax on that gain. The proceeds can then be used to purchase a more manageable home, fund a comfortable retirement lifestyle, or help support your family.

Secret 7: Spousal IRAs Let You Save Even Without Earned Income

Standard IRS rules dictate that you must have earned income—meaning wages from a job or self-employment—to contribute to an Individual Retirement Account (IRA). Pensions, Social Security, and investment dividends do not count as earned income. This rule often penalizes couples where one spouse retires earlier than the other or where one spouse was a lifelong homemaker.

The secret loophole here is the “Spousal IRA.” If you are married and file a joint tax return, the IRS allows the working spouse to fund an IRA for the non-working or retired spouse. The working spouse simply needs to have enough earned income to cover the total contributions made to both accounts.

This strategy allows a household to double their tax-advantaged retirement savings. For example, if you are fully retired but your spouse is still working full-time, your spouse can contribute the maximum annual limit to their own IRA, and then contribute the exact same maximum amount to a separate IRA in your name. This is an excellent way to continue building wealth and reducing your joint taxable income even after you have personally stopped working.

Secret 8: Strategic Roth Conversions Control Your Future Tax Bracket

A Roth conversion involves moving money from a traditional, tax-deferred IRA into a Roth IRA. When you make this move, you must pay income taxes on the amount you convert in the current year. While paying taxes voluntarily sounds counterintuitive, doing it strategically during your early retirement years is a brilliant way to lock in low tax rates for the rest of your life.

Many retirees experience a “gap” in income between the day they stop working and the day they claim Social Security or begin forced RMDs. During these gap years, your taxable income might drop drastically, placing you in the lowest possible tax brackets.

This is the perfect time to perform a strategic Roth conversion by “filling the bracket.” You convert just enough money from your traditional IRA to a Roth IRA to reach the top edge of your current low tax bracket, being careful not to spill over into a higher one.

For example, if you have $20,000 of “room” left in the 12% tax bracket, you can convert exactly $20,000. You pay a modest 12% tax today, but once that money is in the Roth IRA, it grows completely tax-free forever. More importantly, when you withdraw it later in life, it will not count as taxable income, protecting you from future tax hikes and keeping your Medicare premiums low.

Secret 9: Your State Might Not Tax Your Retirement Income At All

Federal taxes are only half the battle; state taxes can heavily influence how far your retirement savings stretch. The secret to maximizing your income might simply be changing your geographic location. The tax landscape across the United States is incredibly diverse, and some states are aggressively competing to attract retirees through favorable tax codes.

Research from AARP highlights that a significant number of states completely exempt Social Security benefits from state income taxes. Furthermore, several states have no income tax whatsoever, meaning your 401(k) withdrawals, pensions, and Social Security are entirely shielded from state-level taxation. States like Florida, Texas, Nevada, and Wyoming fall into this highly desirable category.

However, income tax is not the only metric to watch. When evaluating a state’s tax friendliness, you must look at the overall tax burden. A state might have zero income tax but make up for it with exorbitantly high property taxes or sales taxes. Before relocating, consult with a financial advisor to calculate how a specific state’s comprehensive tax structure will impact your personal monthly budget.

Secret 10: The Government Offers Free, Specialized Tax Prep for Seniors

Paying hundreds of dollars to a CPA or navigating confusing tax software is stressful, especially when you are on a fixed income. Many seniors do not realize that the IRS funds grant programs specifically designed to provide free, trustworthy tax preparation services to older Americans.

The Consumer Financial Protection Bureau (CFPB) advises seniors to take advantage of the Tax Counseling for the Elderly (TCE) program. This program provides completely free tax counseling and preparation to individuals aged 60 and older. The volunteers who run these clinics are IRS-certified and receive specialized training on pension rules, retirement account distributions, and age-specific deductions.

In addition to TCE, the Volunteer Income Tax Assistance (VITA) program offers free help to people who make below a certain income threshold, persons with disabilities, and limited-English-speaking taxpayers. These programs operate in community centers, libraries, and senior centers across the country during tax season. You can easily find a location near you by using the locator tool on the IRS website.

Common Tax Mistakes and Scams Targeting Retirees

Because seniors often have substantial nest eggs and rely on complex financial systems, they are prime targets for fraudsters and predatory practices. Protecting your wealth requires vigilance and a clear understanding of how the IRS actually operates.

One of the most devastating mistakes you can make is falling for an IRS impersonation scam. Scammers will call, text, or email you claiming to be IRS agents. They use aggressive language, threatening you with immediate arrest, deportation, or license revocation if you do not pay a “back tax” immediately via gift cards, wire transfers, or cryptocurrency. The real IRS will never initiate contact via email or text message, nor will they demand payment in gift cards. Official IRS communication always begins with a physical letter sent through the U.S. Postal Service.

Another major pitfall is trusting “ghost preparers.” These are unscrupulous individuals who charge a fee to prepare your taxes but refuse to sign the return as the preparer. They often promise wildly inflated refunds by inventing fake deductions or claiming credits you do not qualify for. When the IRS inevitably flags the fraudulent return, the ghost preparer disappears, and you are left facing severe audits, penalties, and interest on the unpaid taxes.

Finally, a common innocent mistake is missing the deadline for Required Minimum Distributions. If you forget to take your RMD by December 31st, the IRS imposes a penalty on the amount you were supposed to withdraw but did not. While this penalty was recently reduced from 50% to 25% (and sometimes 10% if corrected quickly), it is still an entirely avoidable loss of your retirement funds. Set up automated distributions with your brokerage to ensure you never miss a deadline.

Frequently Asked Questions

At what age do I no longer have to file a tax return?

There is no specific age at which you are legally exempt from filing taxes. Your requirement to file is based entirely on your gross income, filing status, and whether that income exceeds the standard deduction for your age group in that tax year. If your only source of income is Social Security, you typically do not need to file, but if you have pensions, part-time work, or large investment withdrawals, you must continue filing regardless of your age.

What happens if I make a mistake on my tax return?

If you realize you made an error—such as forgetting to claim your higher senior standard deduction or failing to report a 1099 form—do not panic. You can file an amended tax return using Form 1040-X. You generally have up to three years from the date you filed your original return, or two years from the date you paid the tax, to submit an amendment and claim any refunds owed to you.

Are my reverse mortgage payments considered taxable income?

No, reverse mortgage payments are not taxable. The IRS considers these payments to be loan advances, not earned income or investment returns. Because it is borrowed money that will eventually be repaid (usually when the home is sold), it does not increase your taxable income and will not affect the taxation of your Social Security benefits.

Is life insurance taxable when paid out to a beneficiary?

Generally, life insurance proceeds paid to a beneficiary upon the death of the insured are completely tax-free. You do not have to report the payout as gross income. However, if the life insurance company holds the funds for a period and pays you interest on the death benefit, the interest generated is considered taxable income and must be reported.

Are veterans’ benefits taxed by the IRS?

No, the IRS does not tax benefits paid through the Department of Veterans Affairs (VA). This includes disability compensation, pension payments, education grants, and housing allowances. You do not need to include these VA benefits in your gross income calculations on your tax return.

For additional senior resources, visit

Centers for Disease Control and Prevention (CDC), Medicare.gov, National Institute of Mental Health (NIMH), National Institutes of Health (NIH) and Centers for Medicare & Medicaid Services (CMS).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply