Leaving thousands of dollars on the table during retirement is a nightmare, yet millions of Americans do exactly that when they file for Social Security. The widely discussed but rarely understood strategy of coordinating delayed retirement credits with spousal benefits can unlock an extra $24,108 annually for many couples. You do not need a finance degree to capitalize on this approach; you just need patience and the right timing. By simply shifting your filing age and leveraging your spouse’s earning history, you can permanently boost your guaranteed monthly income. This straightforward optimization protects your lifestyle against inflation, rising healthcare costs, and unexpected expenses, ensuring you maintain a comfortable standard of living throughout your golden years.

1. This

2. chart

3. shows

4. how

5. delaying

6. Soc

Unpacking the Delayed Retirement Credit Strategy

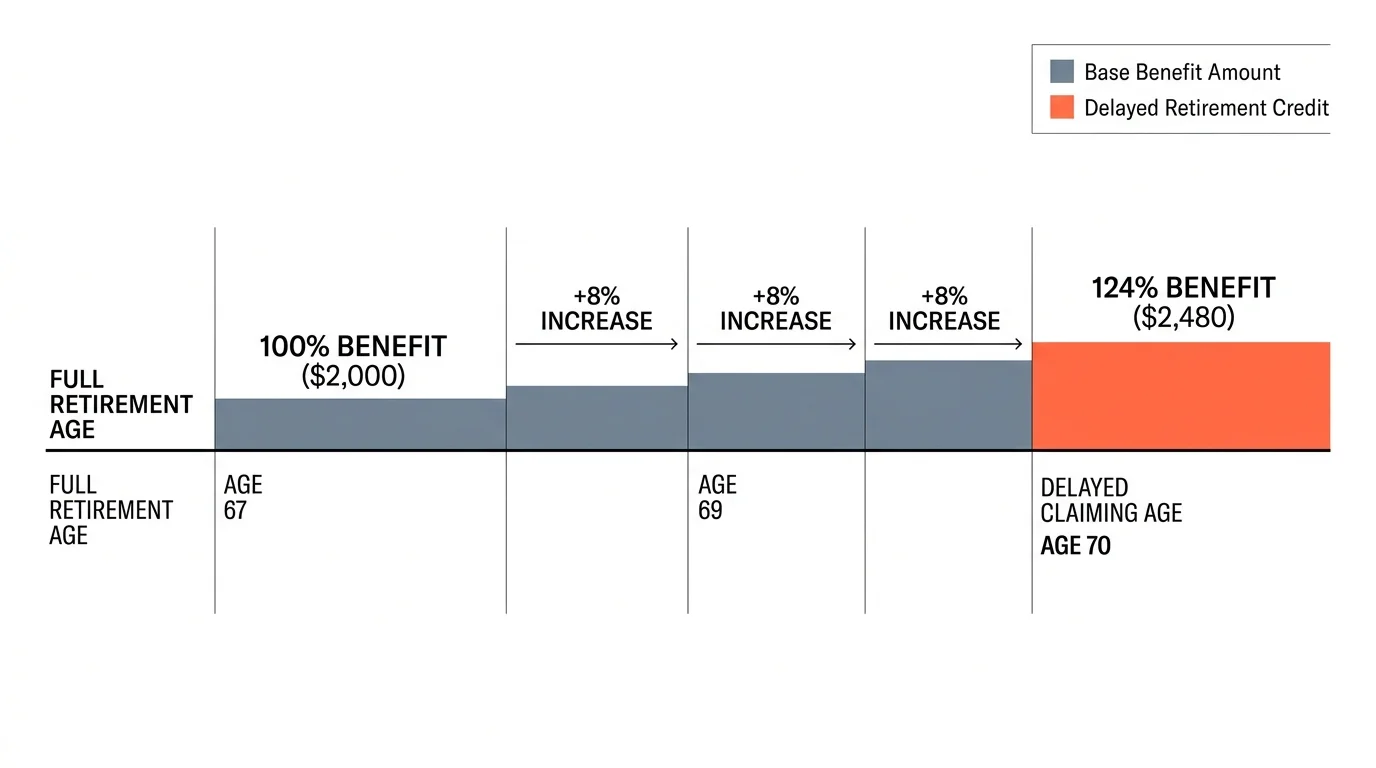

The foundation of this incredible financial boost lies in a rule known as the Delayed Retirement Credit. To understand this, you first need to know your Full Retirement Age. For anyone born in 1960 or later, your Full Retirement Age is 67. This is the age at which you are entitled to receive 100 percent of your earned monthly benefit. However, the system is designed to reward those who wait. For every single month you delay claiming your benefits past your Full Retirement Age, your payout increases.

This increase is not trivial. Over the course of a full year, delaying your claim results in an 8 percent guaranteed increase in your monthly check. If you wait from age 67 to age 70, your benefit grows by a staggering 24 percent. This increase is permanent and serves as one of the few guaranteed, risk-free returns available in the financial world. According to the Social Security Administration (SSA), delaying your benefits until age 70 maximizes your monthly payment, offering significant protection against outliving your savings.

Let us look at a practical example. Imagine your monthly benefit at age 67 is slated to be $2,000. By waiting just three years until age 70, that check swells to $2,480 per month. That translates to an additional $5,760 every single year for the rest of your life. When you apply this math to a household with two high earners, the combined extra income can easily exceed $20,000 to $24,000 annually. Over a twenty-year retirement, that simple act of waiting yields hundreds of thousands of dollars in extra cash flow, offering immense peace of mind.

How Spousal and Survivor Benefits Amplify Checks

The magic truly happens when you coordinate this delayed claiming strategy with your spouse. Social Security offers spousal benefits that allow a lower-earning spouse to claim up to 50 percent of the higher-earning spouse’s Full Retirement Age benefit. Understanding how to stagger your claims can dramatically change your retirement trajectory.

A highly effective approach for couples is the “split strategy.” In this scenario, the lower-earning spouse claims their benefits early—perhaps at age 62 or their Full Retirement Age—to provide the household with a steady stream of income. Meanwhile, the higher-earning spouse delays their claim until age 70 to rack up those 8 percent annual growth credits. This ensures that the largest possible benefit is left to grow untouched, maximizing the eventual payout for the household.

Furthermore, survivor benefits make this strategy absolutely essential for long-term planning. When one spouse passes away, the surviving spouse inherits the single largest benefit between the two. If the higher earner delayed their claim until age 70, they have locked in that permanently boosted amount for their surviving partner. Studies by AARP show that maximizing the higher earner’s benefit is one of the most effective ways to protect a surviving spouse from poverty later in life. By enduring a few years of tighter budgets early in retirement, you provide an enduring financial shield for the person you love.

The Hidden Cost of Claiming at Age Sixty-Two

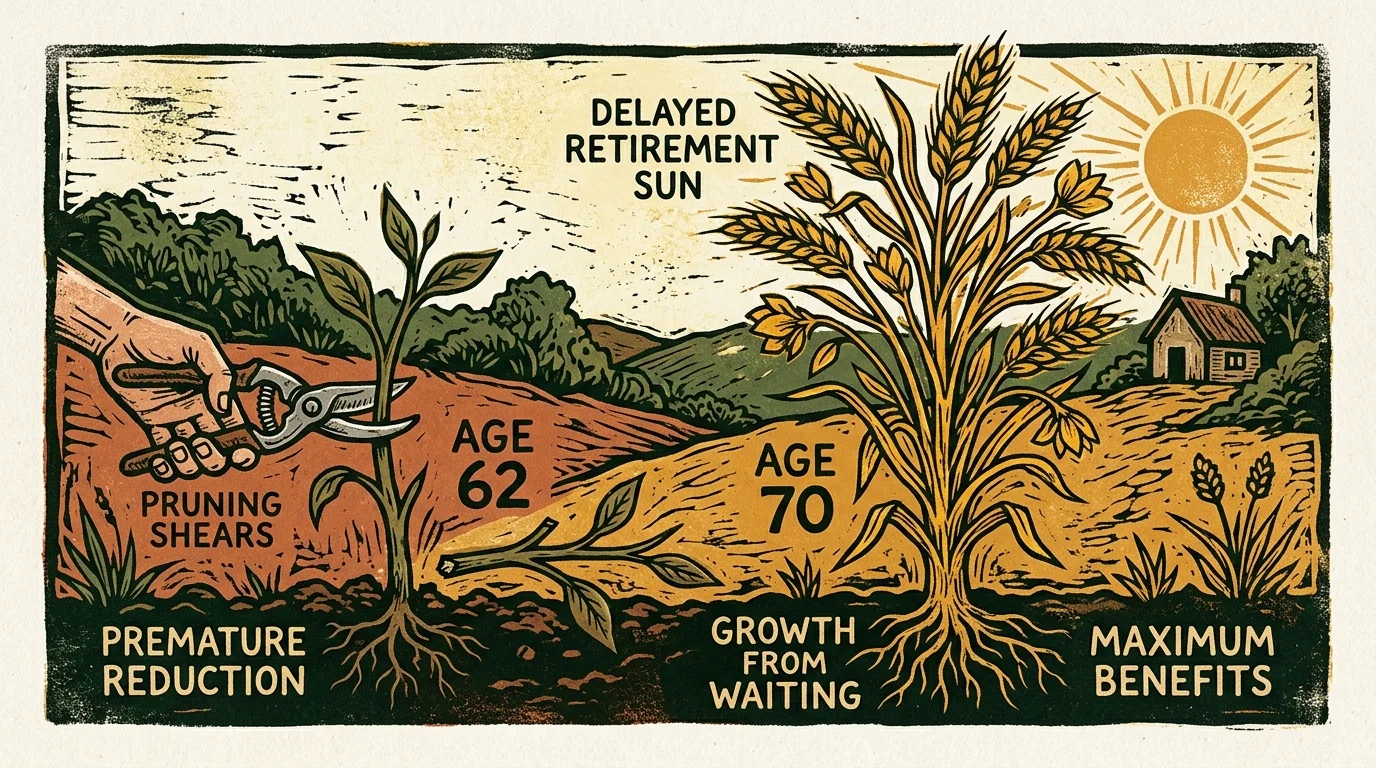

It is entirely understandable why so many seniors want to claim their benefits at age 62. You have worked hard for decades, and the prospect of finally receiving a check is tempting. Moreover, health concerns or unexpected job losses often force early retirement. If you need the money to keep a roof over your head or put food on the table, claiming early is absolutely the right choice for you.

However, if you have other savings to draw from, it is crucial to understand the permanent penalty of claiming at 62. Filing at the earliest possible age reduces your monthly benefit by up to 30 percent compared to what you would receive at your Full Retirement Age. A $2,000 benefit at age 67 instantly shrinks to just $1,400 if taken at age 62.

This reduction is permanent; your benefit will not magically increase to the full amount once you reach age 67. Additionally, if you continue to work while claiming benefits before your Full Retirement Age, you will be subject to the earnings test. The government will temporarily withhold a portion of your benefits if your income exceeds a certain annual limit. While you eventually get this money back in the form of higher payments later, the temporary reduction can be a nasty surprise for those expecting a full check while still working part-time.

Step-by-Step Guide to Maximizing Your Payout

You have the power to control your retirement income by taking a proactive approach. Making the right decision requires looking at your complete financial picture. Follow these practical steps to optimize your strategy:

- Create your online account: Your first step should always be to review your official earnings record. Set up your secure account online to view your estimated payouts at different ages and verify that your lifelong earnings have been recorded accurately.

- Calculate your break-even point: Determine how long you need to live for the higher payments at age 70 to offset the years of missed payments between 62 and 70. For most people, the break-even age falls around 80 to 82. If you have a family history of longevity, delaying is mathematically in your favor.

- Map out a bridge fund: If you plan to delay claiming until 70 but want to stop working at 65, you need a way to pay the bills for those five years. Use withdrawals from your 401(k), IRA, or personal savings to build a financial “bridge” that covers your living expenses while your government benefits grow.

- Coordinate with your spouse: Sit down together and map out who will claim when. Decide if the lower earner should file early to provide cash flow while the higher earner delays.

- Consult a fiduciary advisor: If your situation involves pensions, previous marriages, or complex tax issues, seek out a fee-only fiduciary planner to double-check your math before filing any paperwork.

Comparing Claiming Ages and Financial Outcomes

Sometimes, seeing the numbers laid out clearly is the best way to grasp the sheer magnitude of this decision. The table below illustrates how different claiming ages affect a standard base benefit of $2,000 at a Full Retirement Age of 67. Notice the vast gap between the earliest claiming age and the maximum claiming age.

| Claiming Age | Percentage of Full Benefit | Resulting Monthly Payout | Annual Income |

|---|---|---|---|

| Age 62 | 70% | $1,400 | $16,800 |

| Age 65 | 86.7% | $1,734 | $20,808 |

| Age 67 (Full Retirement Age) | 100% | $2,000 | $24,000 |

| Age 70 (Maximum Benefit) | 124% | $2,480 | $29,760 |

The difference between claiming at 62 and waiting until 70 is $12,960 per year for a single earner in this scenario. Multiply that over a 20-year retirement, and you are looking at $259,200 in extra income. For a dual-income household executing a coordinated strategy, the gap widens significantly, easily reaching the $24,108 annual difference that transforms a restrictive retirement into a comfortable, secure lifestyle.

Coordinating Your Strategy with Healthcare Costs

One of the most overlooked aspects of retirement income planning is the heavy burden of healthcare costs. Even with comprehensive coverage, out-of-pocket medical expenses tend to rise as you age. It is vital to understand the direct relationship between your monthly income and your medical premiums.

Once you enroll in Medicare, your Part B premiums are automatically deducted from your Social Security checks. Because Medicare premiums generally increase over time due to inflation and rising medical costs, they can slowly eat away at a smaller base benefit. If you claim early at 62 and lock in a permanently reduced check, future Medicare premium hikes will consume a much larger percentage of your take-home pay.

By delaying your claim and locking in a higher base payout, you create a buffer against medical inflation. According to Medicare.gov, understanding your expected out-of-pocket costs is essential for long-term budget planning. A robust, maximized monthly check ensures that even when premiums go up, you still have plenty of cash left over for groceries, utilities, and enjoying your retirement.

Tax Implications You Need to Watch Out For

A common and frustrating surprise for new retirees is discovering that the government can tax their benefits. Depending on your overall income level, up to 85 percent of your Social Security payments may be subject to federal income tax. The IRS uses a specific formula called “provisional income” to determine this taxability.

Your provisional income is calculated by taking half of your annual Social Security benefits and adding it to your other sources of income, such as pensions, part-time wages, and withdrawals from traditional IRAs or 401(k)s. If you are married filing jointly and your provisional income exceeds $44,000, up to 85 percent of your benefits become taxable. Single filers hit this threshold at just $34,000.

This is where strategic planning becomes incredibly valuable. As noted by experts at the Consumer Financial Protection Bureau (CFPB), managing your withdrawal sequence from different retirement accounts can help mitigate your tax burden. For instance, drawing down your taxable IRA balances during your early sixties—before you claim Social Security—can lower your required minimum distributions (RMDs) later in life, potentially keeping your provisional income below the taxation thresholds.

Common Social Security Mistakes to Avoid

Navigating the complex rules of government benefits is tricky, and well-meaning seniors frequently fall into traps that cost them dearly. One of the biggest mistakes is failing to consider the impact of a previous marriage. If you were married for at least 10 years and have not remarried, you may be eligible to claim benefits based on your ex-spouse’s earnings record. Many divorced individuals completely miss out on this lifeline simply because they do not know the rule exists.

Another prevalent trap involves falling victim to aggressive phone scams. Fraudsters frequently call older adults pretending to be government agents, claiming that a Social Security number has been suspended due to criminal activity. They will demand immediate payment via gift cards or wire transfers to resolve the issue. Remember this absolute truth: the government will never call you to threaten arrest or demand immediate payment over the phone. Always hang up and contact the official agency directly if you are concerned.

Finally, avoid making decisions based on generalized advice from neighbors or coworkers. Your health history, your savings, and your marital status are completely unique. What worked perfectly for your best friend might be a disastrous financial move for your specific situation. Take the time to map out your own numbers.

Frequently Asked Questions

Can I change my mind if I realize I claimed my benefits too early?

Yes, but you have a very narrow window to act. If you applied for benefits and realize it was a mistake, you can withdraw your application within 12 months of your initial claim. However, you are strictly required to repay every penny you and your family received during that time. You are only allowed to do this once in your lifetime.

Do I get any bonus if I delay my claim past age 70?

No, there is zero financial benefit to waiting beyond your 70th birthday. The delayed retirement credits completely stop accruing the month you turn 70. If you have waited that long, you should immediately file your application so you do not miss out on the money you have earned.

Will my monthly benefits keep up with inflation?

Yes, one of the greatest advantages of this income stream is the Cost-of-Living Adjustment (COLA). Each year, the government evaluates inflation rates and typically applies a percentage increase to your monthly checks to help maintain your purchasing power. A larger base benefit resulting from delaying your claim means you receive a larger absolute dollar amount from these percentage-based COLA increases.

How does earning a paycheck affect my benefits if I claim early?

If you claim benefits before your Full Retirement Age and continue to work, you are subject to the earnings limit. If you earn over a specific annual threshold, the government will withhold $1 in benefits for every $2 you earn above that limit. Once you reach Full Retirement Age, this penalty disappears entirely, and you can earn as much as you want without any reduction to your monthly check.

What happens to my benefits after I pass away?

Your personal benefits cease upon your death, but your surviving spouse is typically eligible for a survivor benefit. They will receive 100 percent of the monthly amount you were collecting, provided it is higher than their own benefit. This is why the higher-earning spouse delaying their claim is heavily encouraged; it leaves the largest possible monthly check for the widow or widower.

For additional senior resources, visit

National Institutes of Health (NIH),

Centers for Medicare & Medicaid Services (CMS),

Social Security Administration (SSA) and

Consumer Financial Protection Bureau (CFPB).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply