Understanding how inflation impacts your Social Security check is essential for protecting your purchasing power in retirement. Rising costs at the grocery store, pharmacy, and gas pump can quickly drain a fixed income if you are not prepared. When everyday prices increase, your monthly benefits must stretch further, making proactive financial management crucial. Fortunately, the Social Security system includes built-in mechanisms designed to help your income keep pace with a changing economy. By learning exactly how inflation adjustments are calculated and discovering smart ways to manage your household budget, you can maintain your standard of living. Staying informed empowers you to make confident financial decisions, ensuring your retirement savings support you comfortably through shifting economic conditions.

The Basics of Inflation and Fixed Incomes

Inflation is a general increase in the prices of goods and services over time. When inflation occurs, every dollar you have buys a smaller percentage of a good or service; economists refer to this as a loss of purchasing power. For workers who receive regular raises, inflation might be manageable. However, if you rely entirely on a fixed income, rising prices present a unique challenge.

Living on a fixed income means your monthly inflow of money remains relatively static, while your outflow naturally increases due to external economic factors. You might notice this firsthand when you pay your winter heating bill or restock your pantry. A carton of eggs, a loaf of bread, or a prescription refill costs more today than it did five years ago. Without mechanisms to increase your income, your standard of living would steadily decline as your money loses its value.

Social Security remains the bedrock of retirement income for millions of Americans, specifically designed to provide a financial safety net. Understanding the interplay between everyday rising costs and your monthly benefits forms the foundation of smart retirement planning. You need to know how the government measures these cost increases and, more importantly, how those measurements directly translate to the dollar amount deposited into your bank account each month.

Navigating the Stress of Rising Prices

Financial discussions often focus entirely on numbers, percentages, and formulas; yet, the emotional toll of inflation requires equal attention. Watching the cost of essential goods climb month after month frequently triggers anxiety. You spent decades carefully planning and saving for retirement, and an unpredictable economy can make you feel as though your hard work is slipping away.

It is perfectly normal to feel stressed when the news constantly reports on high inflation rates. The fear of outliving your money ranks among the top concerns for older Americans. Acknowledging this stress serves as the first step toward regaining control. Rather than allowing economic headlines to induce panic, channel that energy into reviewing your financial habits.

Remember that the United States economy operates in cycles. We have experienced periods of rapid inflation in the past—most notably in the 1970s and early 1980s—and retirees successfully navigated those eras. You possess resilience and life experience. By focusing on the elements of your budget you can control and understanding the protections built into your retirement benefits, you can replace anxiety with confidence and actionable planning.

How the Cost of Living Adjustment Works

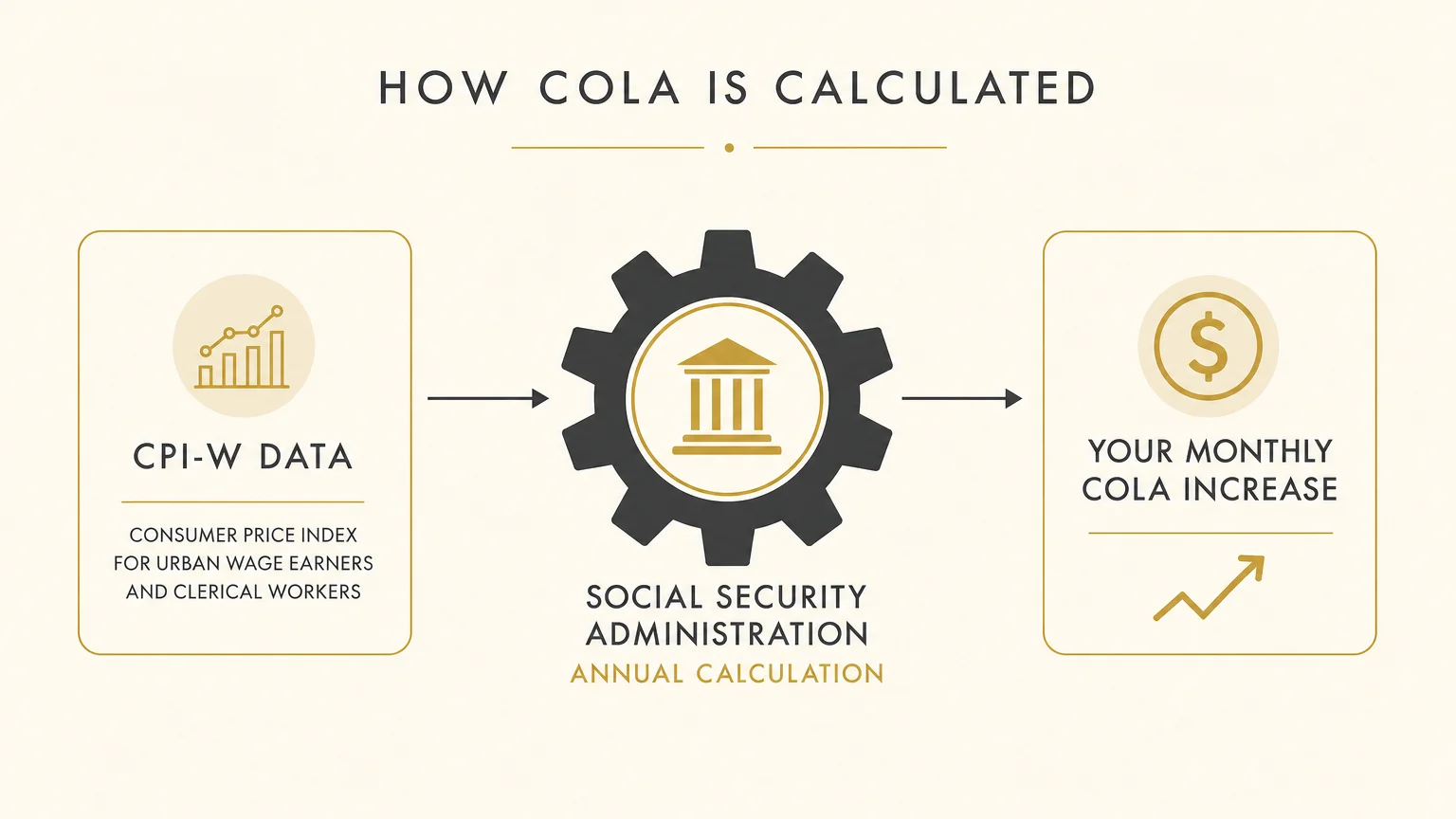

To prevent inflation from severely eroding the value of your benefits, the government implemented the Cost of Living Adjustment, commonly known as COLA. Before 1975, increasing benefits required a special act of Congress, which left retirees waiting years for financial relief. Today, COLA functions automatically, directly linking your benefits to the nation’s inflation rate.

According to the Social Security Administration (SSA), the annual COLA is determined by the percentage increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). The CPI-W measures the average change over time in the prices paid by urban wage earners for a market basket of consumer goods and services.

The calculation process follows a strict calendar. The government compares the CPI-W data from the third quarter of the current year—July, August, and September—to the third quarter of the previous year. If the index shows an increase, your benefits rise by that exact percentage starting the following January. If prices remain flat or decrease, your benefits do not go down; they simply remain the same for the upcoming year. This automatic adjustment stands as one of the most vital protections available to you in retirement.

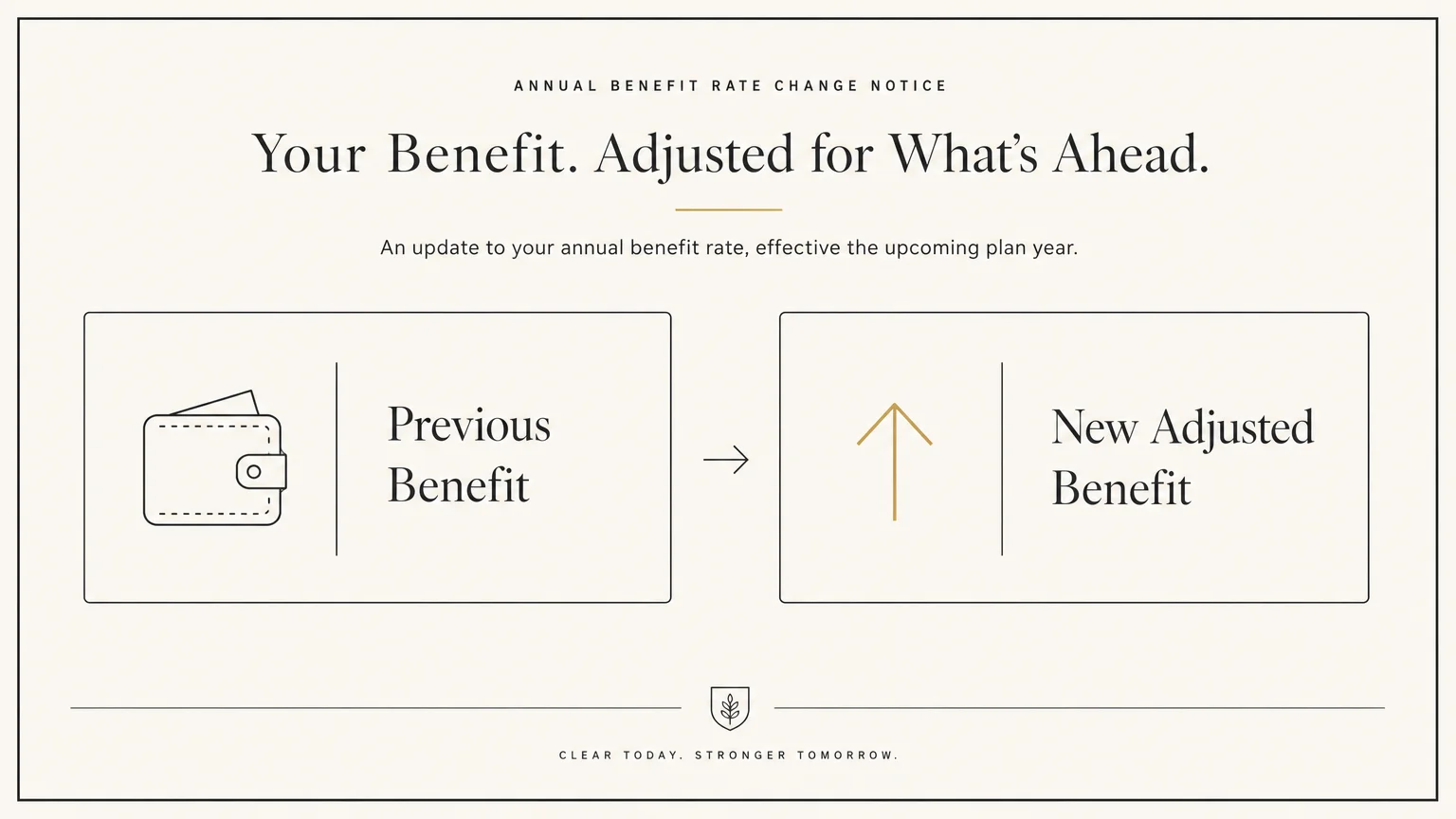

Understanding Your Annual Benefit Rate Change

Every December, you receive a physical letter or a secure digital message outlining your new benefit amount for the upcoming year. This document, the Notice of Benefit Rate Change, holds the key to understanding your exact monthly income. Reading this notice carefully ensures you know exactly how much money will arrive in your bank account.

The notice breaks down the math clearly. It shows your previous gross benefit amount, applies the new COLA percentage, and displays your new gross benefit. However, the gross amount rarely matches the net amount deposited into your account. The notice details specific deductions taken from your check before the money reaches you. The most common and significant deduction is your Medicare Part B premium, which covers your outpatient medical services and doctor visits.

If you prefer not to wait for the mail, you can view your COLA notice online. Creating a secure online account on the government’s portal allows you to review your benefit changes the moment they are finalized. Keeping this document filed with your vital financial records helps you accurately update your household budget for the new year.

Why Your Annual Adjustment Might Feel Insufficient

Despite the annual COLA increase, you might still feel like your check does not cover your expenses the way it used to. This frustration is incredibly common and stems from how the government measures inflation versus how you actually spend your money.

The CPI-W tracks the spending habits of younger, working-age individuals. These workers spend a larger portion of their income on things like gasoline, electronics, and apparel. Retirees, on the other hand, dedicate a significantly larger percentage of their budget to healthcare and housing. Healthcare costs traditionally rise much faster than general consumer goods. Because the COLA calculation relies on the CPI-W, it often underrepresents the actual inflation you experience in the medical and housing sectors.

Furthermore, rising Medicare premiums often consume a large chunk of your COLA increase. As noted by experts at the Centers for Medicare & Medicaid Services (CMS), standard Medicare Part B premiums adjust annually based on broader healthcare costs. If your Social Security check goes up by forty dollars, but your Medicare premium increases by twenty dollars, your net gain feels much smaller. Fortunately, a “hold harmless” provision protects most beneficiaries; if the Medicare premium increase exceeds your COLA increase, your net Social Security check will not decrease from the previous year.

The Real-Life Impact on Your Daily Retirement Expenses

To truly grasp what inflation means for your Social Security check, you must look at everyday expenses. A five percent inflation rate might sound small on the evening news, but it creates a compounding effect on your wallet. Let us review a hypothetical monthly budget comparison to illustrate how quickly rising prices impact a fixed income over a short period.

| Expense Category | Monthly Cost (Year 1) | Monthly Cost (Year 3 with 4% average inflation) | Net Change |

|---|---|---|---|

| Groceries & Household Supplies | $400.00 | $449.95 | +$49.95 |

| Utilities (Electric, Gas, Water) | $250.00 | $281.22 | +$31.22 |

| Out-of-Pocket Healthcare & Prescriptions | $300.00 | $337.46 | +$37.46 |

| Transportation & Auto Insurance | $150.00 | $168.73 | +$18.73 |

| Total Basic Monthly Expenses | $1,100.00 | $1,237.36 | +$137.36 |

As the table demonstrates, a moderate inflation rate adds nearly $140 to your basic monthly living expenses within just three years. Even if your Social Security check increases through COLA, those extra funds are immediately absorbed by the higher cost of simply keeping your lights on and feeding yourself. This clearly illustrates why relying solely on COLA is rarely enough; active budgeting remains essential.

Smart Budgeting Strategies to Combat Rising Prices

When inflation shrinks the power of your Social Security check, adopting defensive budgeting strategies helps protect your financial well-being. You cannot control the national economy, but you have complete control over your household spending. Evaluating your outgoings with a critical eye reveals opportunities to save money without drastically altering your lifestyle.

The Consumer Financial Protection Bureau (CFPB) recommends regularly reviewing your financial statements to identify areas where you can safely cut back or optimize your spending. Implementing a structured approach to your finances creates a protective buffer against unexpected price hikes.

- Audit Your Subscriptions: Review your bank statements for recurring charges. Cable packages, magazine subscriptions, and streaming services add up quickly. Cancel the services you no longer use regularly.

- Utilize Senior Discounts: Never hesitate to ask for a senior discount. Grocery stores, retail chains, and restaurants frequently offer specific days where older adults receive percentages off their total bill.

- Review Your Insurance Policies: Auto and homeowners insurance rates often creep up over time. Contact your agent annually to ensure you receive all applicable discounts, such as low-mileage reductions, or shop around for better rates.

- Explore Energy Assistance Programs: Utility costs represent a massive burden during high inflation. Look into the Low Income Home Energy Assistance Program (LIHEAP), which helps eligible seniors cover heating and cooling costs.

- Optimize Your Grocery Shopping: Switch to store brands, buy non-perishable items in bulk when they go on sale, and plan your meals around weekly digital coupons.

- Check Benefit Eligibility: Millions of older adults qualify for programs like the Supplemental Nutrition Assistance Program (SNAP) or Medicare Savings Programs but never apply. These programs can free up hundreds of dollars in your budget.

Protecting Your Wider Retirement Savings from Inflation

Your Social Security check likely forms just one part of your retirement income puzzle. If you have personal savings, IRAs, or a 401(k), you must ensure those assets do not lose their value while sitting in the bank. Stashing all your cash in a traditional checking account with a near-zero interest rate guarantees that inflation will slowly consume your purchasing power.

Research from AARP highlights the importance of maintaining a diversified portfolio, even in retirement, to outpace inflation. While you naturally want to keep a portion of your money in highly liquid, safe accounts for emergencies, leaving everything in cash exposes you to long-term economic risk.

Consider looking into inflation-protected assets. High-yield savings accounts or Certificates of Deposit (CDs) offer much better returns than standard checking accounts. Treasury Inflation-Protected Securities (TIPS) and Series I Savings Bonds are government-backed options explicitly designed to rise in value alongside inflation. Before making sweeping changes to your life savings, discuss your risk tolerance and income needs with a certified financial planner. They can help you structure your withdrawals so you draw down your assets efficiently, preserving your wealth for the years ahead.

Common Financial Pitfalls to Avoid When Prices Rise

High inflation often breeds financial panic, leading retirees to make hasty decisions they later regret. Scammers and aggressive salespeople closely monitor economic trends, utilizing the fear of rising prices to push predatory products onto vulnerable seniors.

One major pitfall involves falling for “inflation-proof” investment schemes. You might hear radio advertisements or receive mailers promising guaranteed double-digit returns through obscure cryptocurrency investments or overpriced physical gold coins. These investments often carry hidden fees, immense risks, and a lack of liquidity, meaning you cannot access your money when you actually need it to pay bills.

Another common mistake involves taking on high-interest debt to cover everyday expenses. Using credit cards to bridge the gap between your Social Security check and your living costs creates a dangerous cycle. As inflation rises, the Federal Reserve typically raises interest rates to cool the economy. Consequently, the interest rates on your credit cards skyrocket. What started as a small balance for groceries can rapidly snowball into unmanageable debt. If you find yourself unable to cover basic needs, seek out local community assistance programs rather than relying on credit cards.

Frequently Asked Questions

Do I need to apply or register to receive the annual COLA increase?

No, you do not need to take any action. The Social Security Administration applies the Cost of Living Adjustment automatically to your benefits. The increased amount will simply appear in your regular January payment each year that a COLA is enacted.

Will high inflation today reduce my future Social Security benefits?

No. High inflation triggers higher COLA increases, which permanently raises your base benefit amount for the future. Even if inflation cools down in subsequent years, your new, higher base amount remains intact. Social Security rules are specifically designed to ensure inflation does not diminish your hard-earned benefits.

What happens if inflation goes down? Do my benefits decrease?

If the inflation index shows negative growth—a rare event known as deflation—your Social Security benefits will not decrease. By law, your payment amount will remain exactly the same as the previous year. You will never see a reduction in your gross benefit due to fluctuating inflation rates.

Why does my neighbor receive a different COLA dollar amount than I do?

The annual COLA is a percentage, not a flat dollar amount. Because everyone’s base Social Security benefit differs—based on their lifetime earnings and the age they chose to claim benefits—the exact dollar increase varies from person to person. A 3% increase on a $1,500 monthly benefit equals $45, while a 3% increase on a $2,000 benefit equals $60.

Does working while receiving Social Security affect my COLA?

Working does not negatively affect your COLA. The percentage adjustment applies to your benefit regardless of your employment status. In fact, if you continue to work and pay Social Security taxes, your base benefit amount might even increase if your current earnings replace lower-earning years from your past work history.

For additional senior resources, visit

Alzheimer’s Association, American Heart Association and Benefits.gov.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply