Navigating the rules of retirement income often feels like deciphering a foreign language, and widespread rumors only make the process more stressful. Relying on outdated or incorrect advice about your benefits can cost you thousands of dollars over your lifetime and jeopardize your financial security. Separating fact from fiction empowers you to make informed decisions about when to claim, how to maximize your monthly checks, and what rules apply if you choose to keep working. By understanding the real mechanics behind the system, you can build a reliable retirement strategy that protects your hard-earned money and provides lasting peace of mind.

Myth: The System Is Going Bankrupt and Will Disappear

One of the most persistent and anxiety-inducing rumors you will hear is that the system is completely broke and will vanish before you receive your checks. This fear causes many seniors to panic and claim their benefits as early as possible, assuming they need to grab what they can before the money disappears. Understanding how the program is actually funded reveals why this fear is largely unfounded.

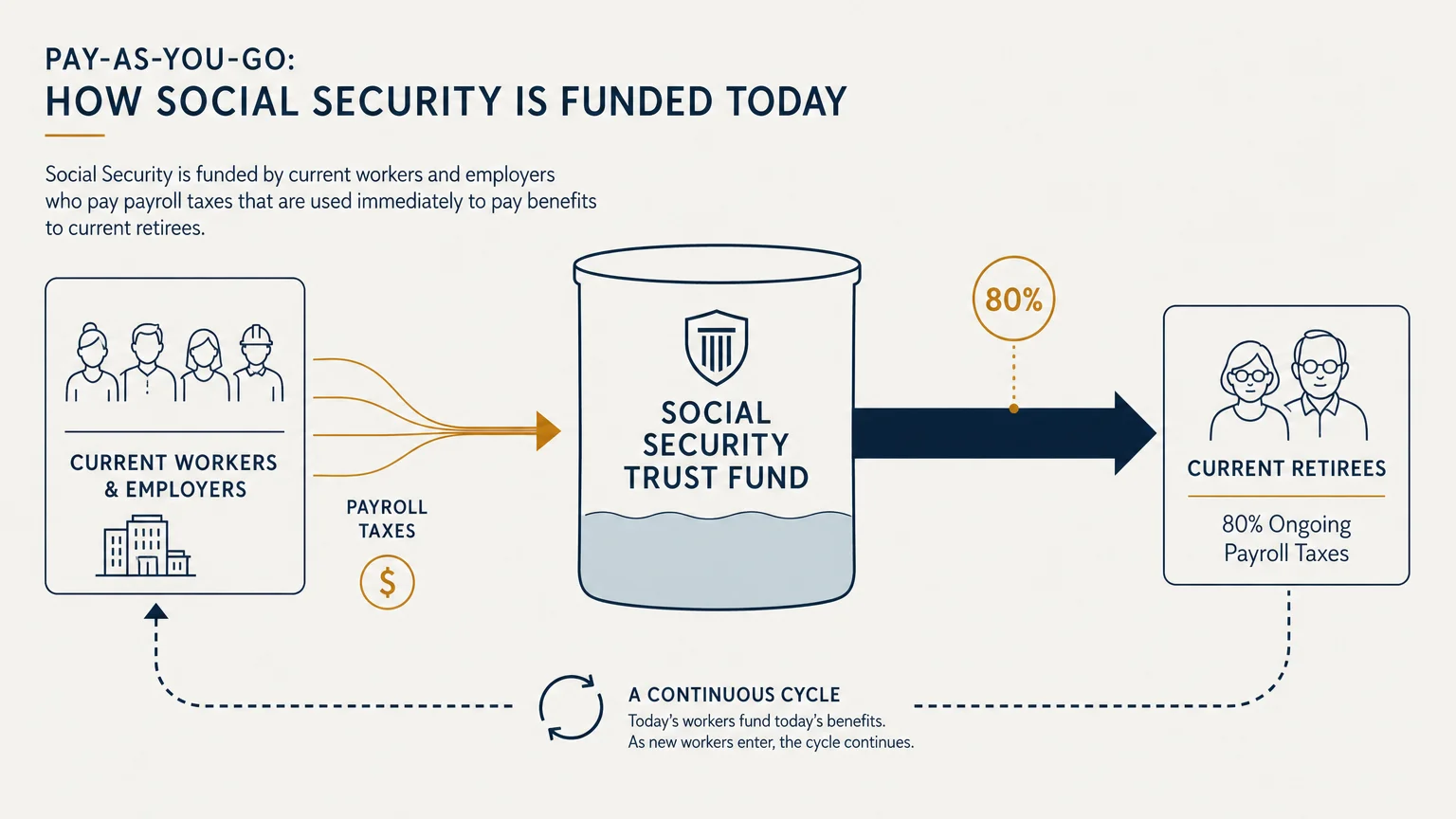

The program operates primarily as a pay-as-you-go system. Current workers and their employers pay payroll taxes, which immediately go toward paying benefits for current retirees. As long as Americans continue to work and pay taxes, money will continually flow into the system. It is not an individual savings account that can hit zero and close its doors.

The confusion stems from news about the trust fund reserves. The program does hold surplus reserves, built up over years when tax revenues exceeded benefit payouts. These reserves are indeed projected to run low in the coming decade. However, even if the surplus completely depletes, ongoing payroll taxes will still cover the vast majority of promised benefits—typically estimated around eighty percent. Congress also has numerous legislative options to bridge this gap, such as adjusting the payroll tax rate, raising the earnings cap, or modifying the retirement age for younger generations.

Making lifelong financial decisions based on sensational headlines can be a costly mistake. Base your retirement planning on the facts of the program as it stands today, rather than worst-case scenarios.

Myth: Your Full Retirement Age Is Always Sixty-Five

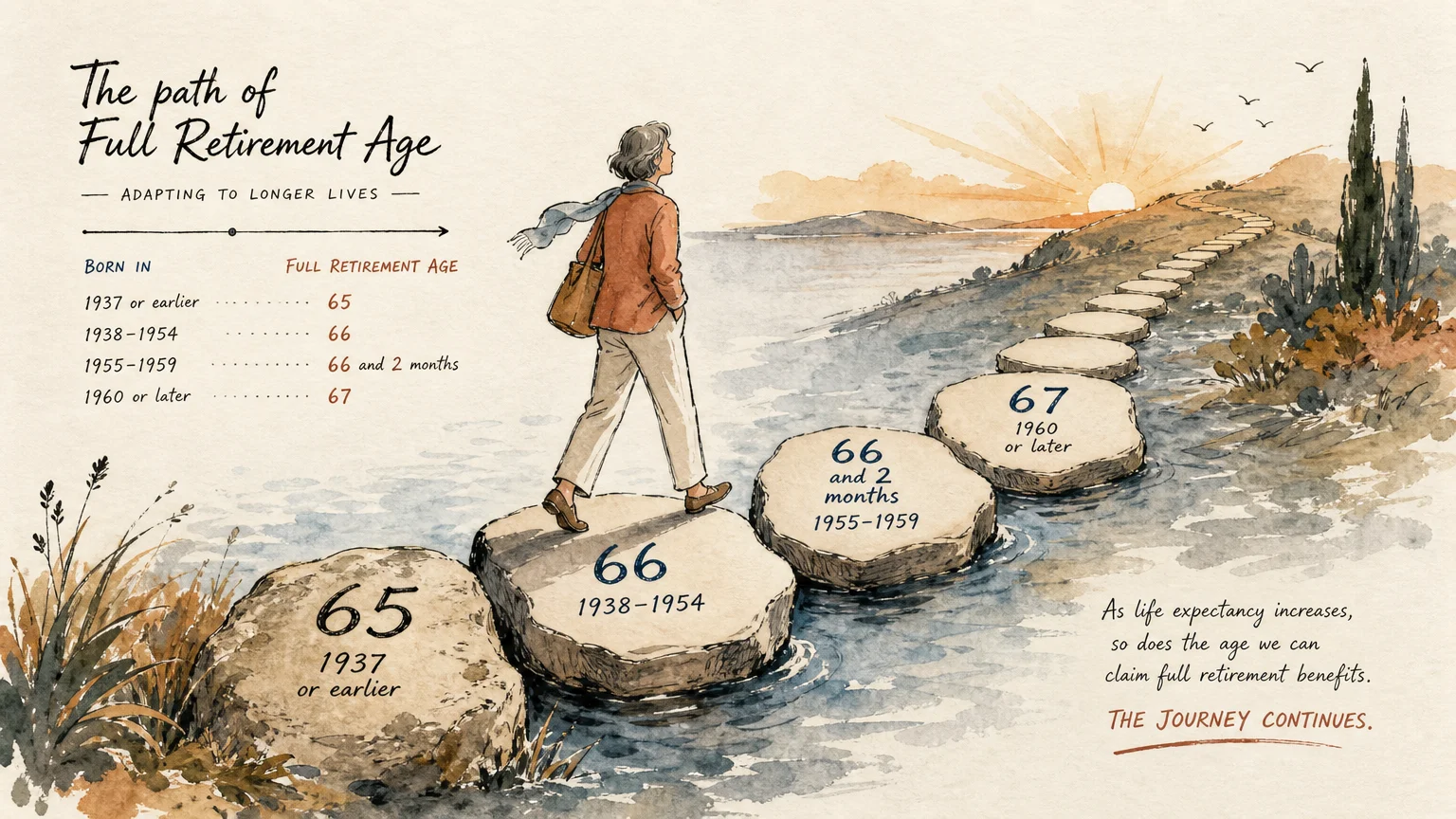

For generations, age sixty-five stood as the golden milestone for retirement. It was the age when Americans expected to stop working, collect their gold watch, and receive their full government pension. Because this number is so deeply ingrained in our culture, many people still incorrectly assume that sixty-five remains their Full Retirement Age (FRA).

Congress changed the rules decades ago to account for increasing life expectancies. Your FRA—the age at which you are entitled to one hundred percent of your earned benefit without early filing reductions—now depends entirely on your birth year. If you claim your checks before reaching this specific age, your monthly payout will be permanently reduced.

To plan accurately, you need to know your exact FRA. The table below outlines the full retirement age based on your birth year:

| Birth Year | Full Retirement Age |

|---|---|

| 1943 – 1954 | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 and later | 67 |

If you were born in 1960 or later, your full retirement age is sixty-seven. Claiming at sixty-five means you are claiming early, which triggers a permanent reduction in your monthly income. Knowing your specific target age allows you to calculate exactly how much money you will receive and helps you coordinate your retirement dates with your actual financial needs.

Myth: Claiming Early Makes Financial Sense for Everyone

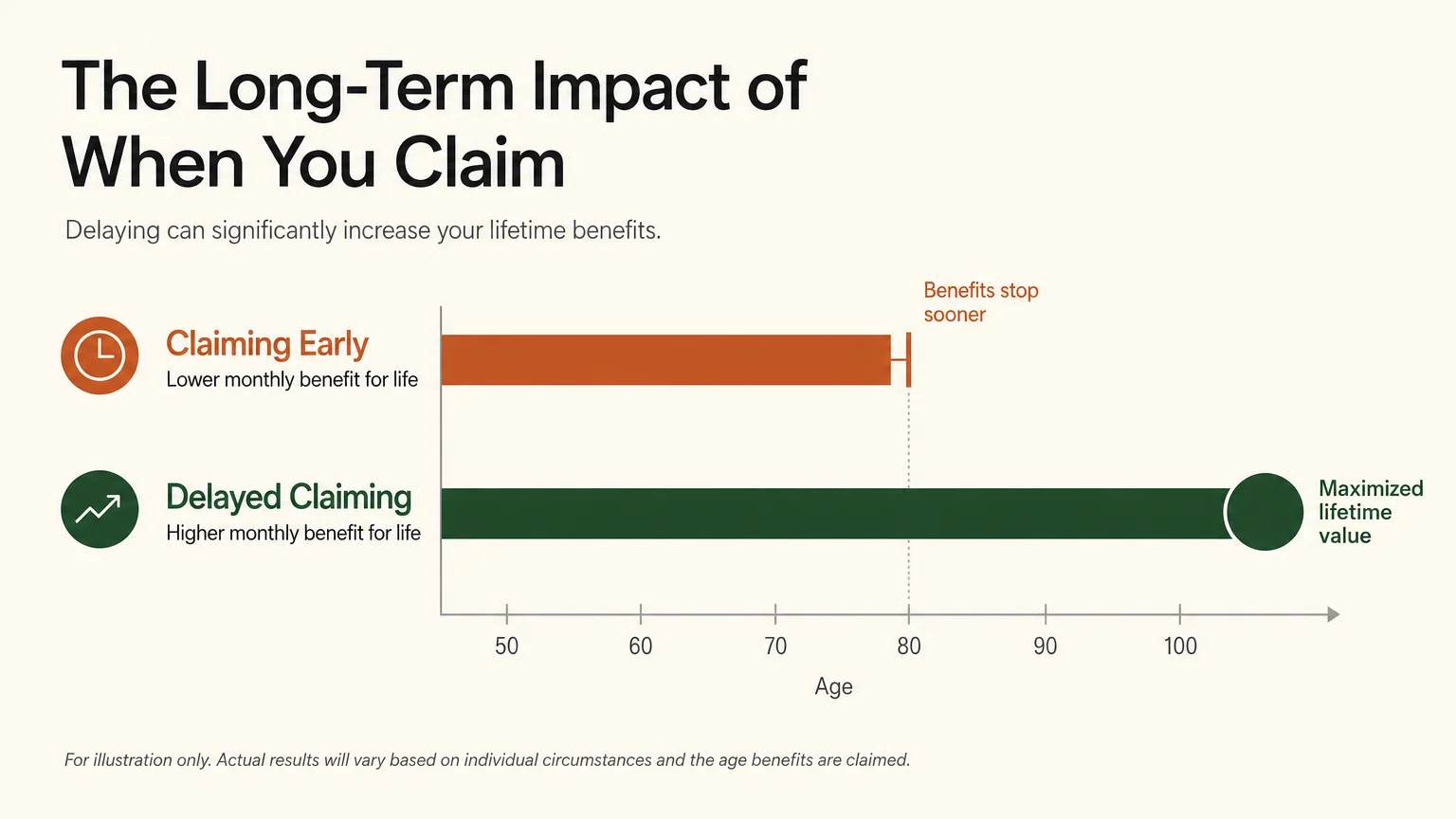

You will often hear advice suggesting you should claim your benefits at age sixty-two—the earliest possible age—because “it is your money and you should get it as soon as you can.” While claiming early is the right choice for some individuals, particularly those with serious health issues or pressing financial emergencies, treating it as a universal rule is a major misconception.

Claiming at age sixty-two permanently shrinks your monthly check by up to thirty percent compared to waiting for your Full Retirement Age. Conversely, delaying your claim past your FRA earns you delayed retirement credits. Your benefit grows by eight percent for every year you wait, up until age seventy. A benefit that pays one thousand dollars at your FRA could grow to one thousand two hundred and forty dollars simply by waiting.

As noted by experts at the Consumer Financial Protection Bureau (CFPB), deciding when to claim is one of the most important financial choices you will make, and delaying can significantly increase your monthly payout, helping protect against outliving your savings.

When considering when to file, you must factor in your life expectancy and your marital status. If you are the higher earner in your marriage, delaying your claim not only increases your own monthly check but also maximizes the survivor benefit your spouse will receive if you pass away first. A surviving spouse inherits the higher of the two benefits received by the couple. Filing early permanently reduces the financial safety net left for your widow or widower.

Myth: Working While Receiving Benefits Means You Lose Money Forever

Many seniors want to transition slowly into retirement by working part-time. However, a common myth holds that if you work while receiving benefits, the government will confiscate your checks and you will never see that money again. This misunderstanding stems from confusion surrounding the Retirement Earnings Test.

The earnings test only applies if you claim benefits before reaching your Full Retirement Age and continue to work. Under this rule, if your earned income exceeds an annual limit set by the government, your benefits are temporarily reduced. Specifically, the government withholds one dollar in benefits for every two dollars you earn above the limit.

The crucial word here is “withheld”—not lost. The money is not gone forever. Once you reach your Full Retirement Age, your monthly benefit is recalculated to account for the months your checks were withheld. Your future monthly payments will be increased, allowing you to gradually recoup the withheld funds over your remaining lifetime.

Furthermore, the month you reach your Full Retirement Age, the earnings test disappears entirely. You can earn an unlimited amount of money from an employer or a business, and your monthly checks will not be reduced by a single penny. Understanding this mechanism allows you to comfortably work part-time in your early sixties without fearing you are permanently throwing away your hard-earned benefits.

Myth: You Cannot Claim Benefits on an Ex-Spouse’s Record

Divorce disrupts many financial plans, but it does not necessarily erase your retirement safety net. A prevalent myth suggests that once a marriage ends, you forfeit any right to your former spouse’s earnings record. In reality, the program includes specific provisions to protect divorced individuals, particularly those who may have stayed home to raise children or earned significantly less than their partners.

You can claim divorced spousal benefits if you meet a specific set of criteria. First, your marriage must have lasted for at least ten consecutive years. Second, you must currently be unmarried. Third, you must be at least sixty-two years old. If you meet these conditions, you may be eligible to receive up to fifty percent of your ex-spouse’s Full Retirement Age benefit amount.

You will only receive this spousal benefit if it is higher than the benefit you are entitled to based on your own work history. The system will automatically pay you the higher of the two amounts, but not both.

One of the greatest fears people have regarding this rule is that filing on an ex’s record will negatively impact the ex-spouse or their new family. This is completely false. Your claim has absolutely zero effect on your ex-spouse’s monthly check, nor does it reduce the benefits available to their current spouse. In fact, your ex-spouse will not even be notified that you have filed a claim on their record. Gathering your marriage certificate and final divorce decree is a simple, proactive step to ensure you receive all the income you are legally owed.

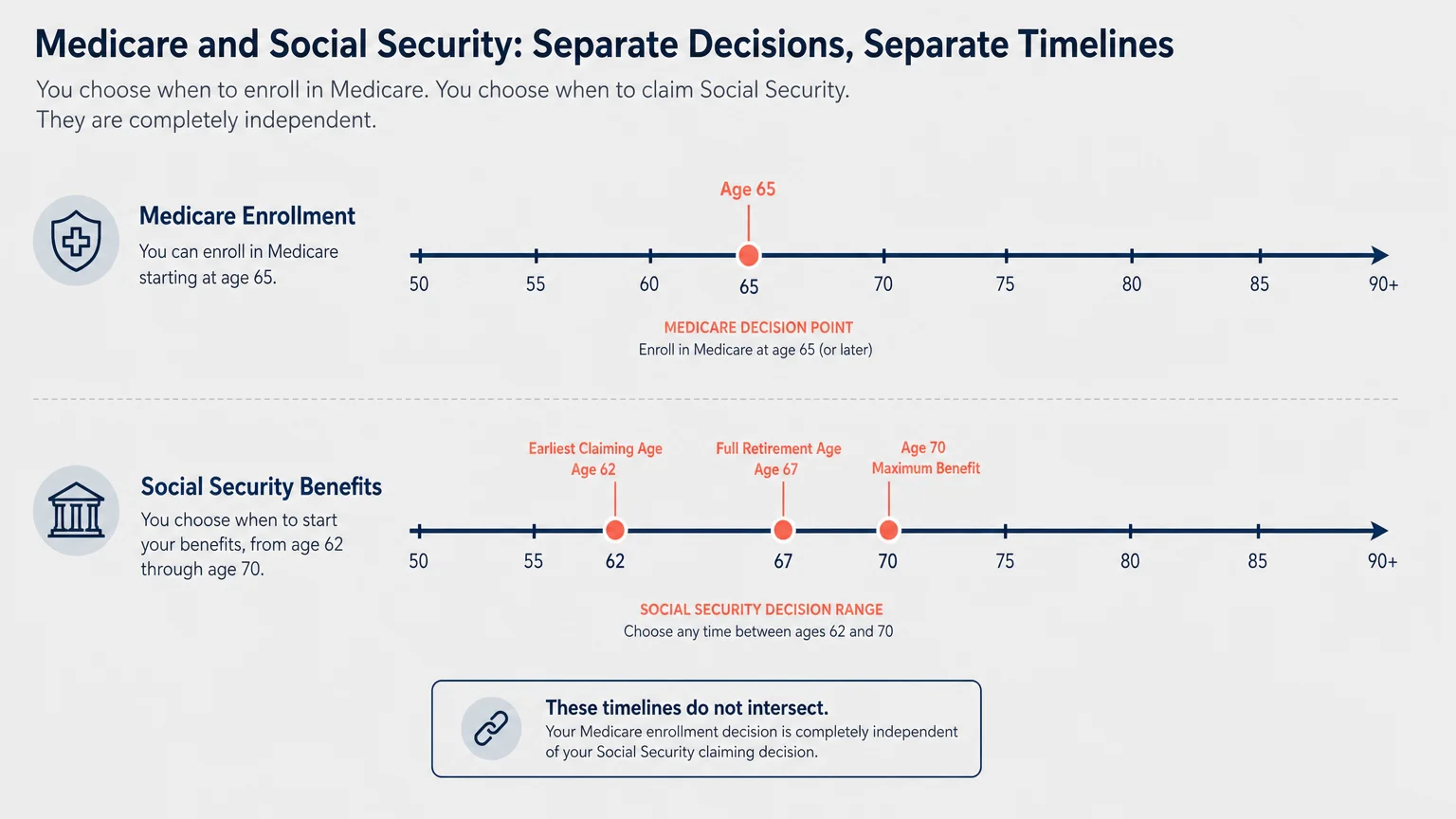

Myth: Medicare and Social Security Must Start at the Same Time

Because Medicare and retirement income are the twin pillars of American senior planning, they are frequently confused as a single package deal. Many people mistakenly believe they must start both programs at the exact same time. This myth causes seniors to either claim their income too early just to get health insurance, or delay their health insurance and incur massive penalties because they want to delay their income.

These are two distinct programs with entirely different timelines. You can begin claiming retirement income anywhere between ages sixty-two and seventy. Medicare, however, is strictly tied to age sixty-five for the vast majority of Americans.

Your Initial Enrollment Period for Medicare begins three months before your sixty-fifth birthday, includes your birthday month, and extends for three months afterward. You must handle your Medicare enrollment during this window, regardless of whether you have filed for monthly retirement checks.

The official guidelines at Medicare.gov explain that missing your Initial Enrollment Period for health coverage can result in lifelong late enrollment penalties, regardless of when you plan to claim your retirement checks.

If you wait to enroll in Medicare Part B until you finally claim your income at age seventy, you could face a permanent, cumulative penalty added to your monthly health insurance premiums. Treat your health insurance timeline and your income timeline as separate decisions. You can confidently sign up for Medicare at sixty-five while allowing your income benefits to grow until a later date.

Protecting Yourself From Social Security Scams

Where there is money, there are criminals looking to steal it. Scammers are well aware of the anxiety surrounding retirement planning, and they aggressively target seniors with sophisticated fraud schemes. Believing the myth that government agents will call you with urgent threats puts your finances in severe danger.

A common tactic involves a phone call from someone claiming to be a government agent. They will assert that your Social Security number has been “suspended” due to suspicious activity, or that you are facing imminent arrest for tax evasion. The caller then demands immediate payment to resolve the issue, often insisting you buy prepaid gift cards, send wire transfers, or deposit cash into cryptocurrency ATMs.

According to the Social Security Administration (SSA), government employees will never threaten you with arrest, suspend your number, or demand immediate payment via wire transfer, gift cards, or cryptocurrency.

To protect yourself, keep these concrete rules in mind:

- Never trust caller ID: Scammers use software to spoof official phone numbers, making it look like the government is actually calling.

- Do not confirm personal details: If someone calls asking you to verify your personal information to unfreeze your account, hang up immediately.

- Official communication is slow: Genuine problems with your benefits are communicated via official letters sent through the U.S. Postal Service, not through aggressive phone calls or text messages.

- Take control: If you are worried there might be a legitimate issue with your account, hang up the phone. Look up the official, verified phone number for the agency yourself, and call them directly to inquire.

Creating your secure online account through the official government portal is an excellent defensive move. By establishing your login credentials, you prevent identity thieves from creating an account in your name and redirecting your monthly payments to their own bank accounts.

Frequently Asked Questions

Do I have to pay taxes on my Social Security benefits?

Yes, depending on your total overall income, a portion of your benefits may be subject to federal income tax. To determine this, you must calculate your “provisional income,” which includes half of your benefit amount plus all your other taxable income and non-taxable interest. If this combined total exceeds certain thresholds—currently twenty-five thousand dollars for individuals or thirty-two thousand dollars for married couples filing jointly—up to eighty-five percent of your benefits could be taxed. Many states, however, do not tax these benefits at the state level.

What happens to my benefits if I move to a foreign country?

If you are a United States citizen, you can generally receive your monthly checks in most countries around the world. The government will direct deposit your funds into a bank account just as they would if you lived in the U.S. However, there are specific countries—such as Cuba and North Korea—where the government is legally prohibited from sending payments. If you plan to retire abroad, review the official international payment guidelines to ensure your destination country is approved.

Can I change my mind after I start claiming my benefits?

Yes, but you have a very limited window to do so. If you file for benefits and quickly realize it was a mistake—perhaps you decided to go back to work or realized you prefer to let your benefits grow—you can withdraw your application. You must do this within twelve months of your initial claim, and you are only allowed one withdrawal per lifetime. Crucially, you must repay every single dollar you and your family members received before your application can be canceled.

Will my monthly payments keep up with inflation?

Yes, the program is designed to help your purchasing power keep pace with rising costs. Each year, the government calculates a Cost-of-Living Adjustment (COLA) based on inflation metrics from the Department of Labor. If inflation rises, your monthly check will increase starting the following January. While the COLA may not always perfectly match your personal household expenses, it provides vital protection against the long-term erosion of your retirement income.

Do my benefits automatically pass on to my children when I die?

Generally, your standard retirement benefits do not automatically pass to adult children. The program is primarily designed to support you and your surviving spouse. However, there are exceptions. If your children are unmarried and under the age of eighteen (or up to nineteen if attending high school full-time), they may be eligible for survivor benefits. Additionally, a child who became strictly disabled before the age of twenty-two can receive lifelong survivor benefits based on your earnings record.

For additional senior resources, visit

Medicare.gov, National Institute of Mental Health (NIMH) and National Institutes of Health (NIH).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply