Living on a fixed income during retirement often requires stretching every dollar to cover daily expenses, housing, and healthcare costs. However, many older adults unknowingly miss out on extra monthly payments they have earned or qualify to receive. Beyond your standard Social Security payout, you might be eligible for additional checks ranging from veterans benefits and spousal support to specialized tax rebates and forgotten pension payouts. Identifying these hidden income sources can significantly ease your financial burden and provide much-needed breathing room in your monthly budget. By understanding the specific requirements for these supplemental programs, you can claim the funds you deserve and build a more comfortable, secure retirement.

Supplemental Security Income (SSI)

Many retirees assume that their monthly Social Security retirement benefit is the only federal support available to them. Supplemental Security Income (SSI) is a completely separate program designed to help those with minimal income and resources. Unlike standard retirement benefits—which are based on your lifetime earnings and work history—SSI is entirely needs-based. It is funded by general tax revenues, not Social Security taxes.

You may qualify for SSI if you are 65 or older, blind, or disabled, and you meet strict financial limits. The government sets a federal benefit rate each year, which establishes the maximum monthly SSI payment. For individuals who receive very small Social Security checks because they had low lifetime earnings, SSI can step in to bridge the gap. According to the Social Security Administration (SSA), you can receive both Social Security retirement benefits and SSI at the same time if your standard benefit falls below the SSI threshold.

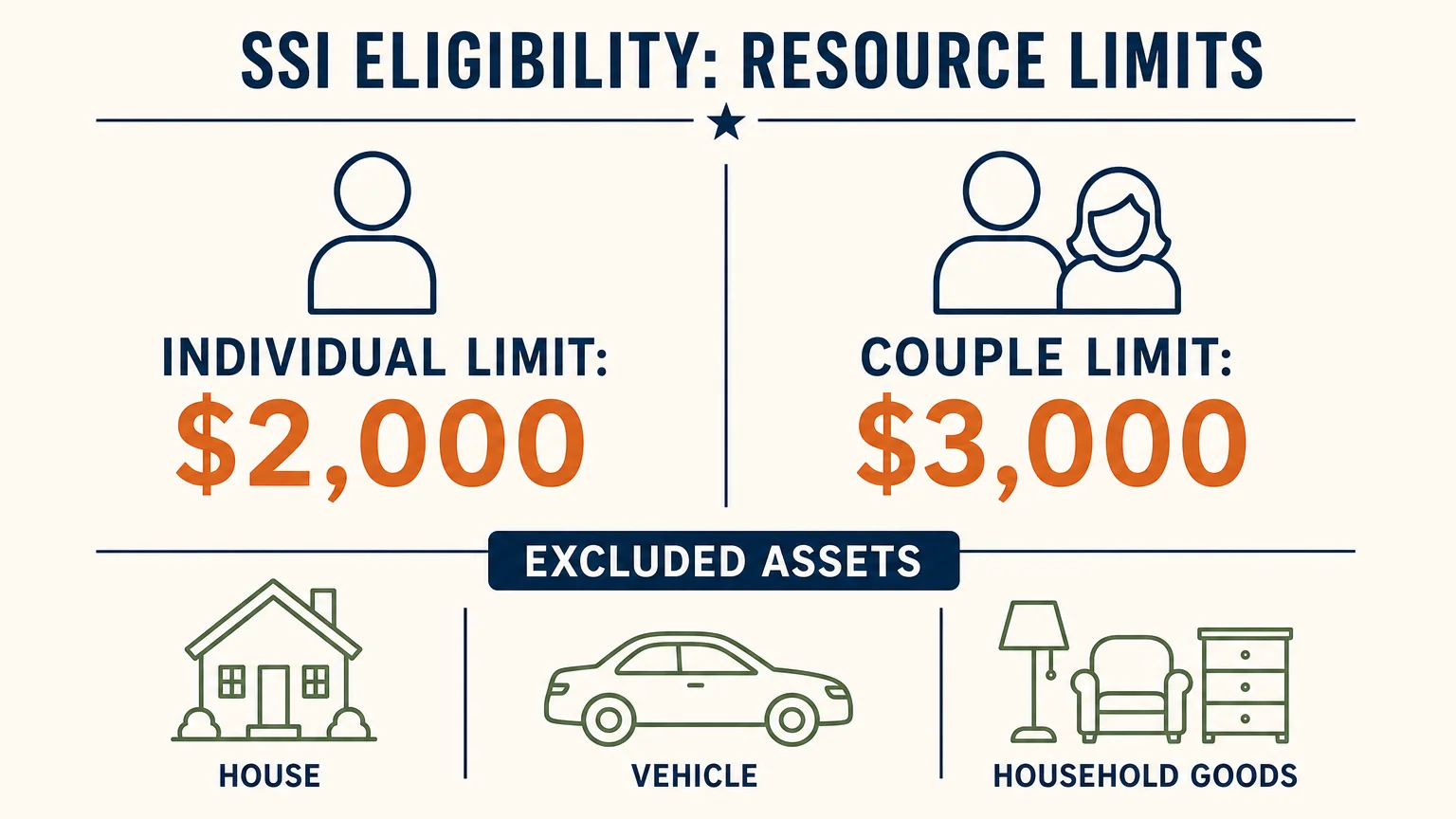

To qualify, your countable resources must not exceed $2,000 for an individual or $3,000 for a couple. Fortunately, the government does not count everything you own. Your primary residence, one vehicle, and everyday household goods are typically excluded from this limit. If you struggle to make ends meet each month, applying for SSI is a critical first step toward securing additional cash assistance.

Spousal and Survivor Benefits

Your marital history can play a massive role in the checks you receive during retirement. The Social Security system offers robust protections for spouses, widows, and even divorced individuals, yet many seniors fail to optimize these benefits. You might be entitled to a higher monthly payout based on your current or former partner’s work record rather than your own.

If you are married, you can claim up to 50 percent of your spouse’s primary insurance amount. If your own earnings record yields a smaller benefit than your spousal benefit, the government will automatically top up your check to match the higher spousal amount. This ensures that a lower-earning spouse is not financially penalized in retirement.

Survivor benefits offer an even stronger safety net. When a spouse passes away, the surviving partner can step into the deceased spouse’s shoes and receive up to 100 percent of their monthly benefit. You cannot receive both your own benefit and your survivor benefit simultaneously; you receive whichever is higher. This sudden adjustment often results in a larger single check for the surviving spouse, helping offset the loss of household income.

Divorced individuals frequently overlook their eligibility. If you were married for at least 10 consecutive years and have not remarried, you can claim benefits based on your ex-spouse’s record. Claiming this benefit has zero impact on your ex-spouse’s payout or the payout of their current spouse.

Veterans Affairs (VA) Benefits

Military service members who defended our country often qualify for substantial financial support later in life. Veterans Affairs (VA) benefits act as a vital supplementary income stream, but the application processes can be complex, causing some veterans to miss out.

The VA offers a Veterans Pension program for wartime veterans who meet specific age and income requirements. This pension provides monthly payments to veterans aged 65 and older who have limited financial resources. Furthermore, if you suffered an injury or illness connected to your military service, you might be eligible for VA Disability Compensation. These tax-free monthly payments are scaled based on the severity of your service-connected disability.

One of the most valuable, yet underutilized, programs is the Aid and Attendance (A&A) benefit. This is an additional payment added to the regular VA pension for veterans and survivors who require the regular assistance of another person to perform basic activities of daily living—such as bathing, dressing, or eating. It also applies if you are bedridden, reside in a nursing home due to mental or physical incapacity, or have severely limited eyesight. Aid and Attendance checks can provide thousands of extra dollars each year, making home care or assisted living much more affordable.

State Tax Rebates and Relief Programs

Federal checks receive the most attention, but state governments also distribute funds to older adults. State legislators frequently pass surplus budgets, inflation relief bills, or specialized property tax refunds aimed at easing the financial burden on seniors living on fixed incomes.

Property tax “circuit breaker” programs are incredibly popular across the United States. These programs provide a refund or a direct check to seniors whose property taxes exceed a certain percentage of their annual income. Even if you rent your home, some states offer renter’s rebates that simulate property tax relief, putting hundreds of dollars back into your pocket every year.

To find out what your state offers, you can research local department of revenue websites. You can also explore various state-level assistance programs by visiting Benefits.gov to determine your eligibility for regional tax rebates and direct payments. Missing the filing deadline for these state-specific programs is a common mistake; mark your calendar for local tax season to ensure you claim your relief check.

Pensions and Annuities

While traditional pensions are less common today than they were decades ago, many current retirees spent part of their careers working for companies or government agencies that still provide defined benefit plans. These plans guarantee a specific monthly payout for life, serving as an excellent companion to Social Security.

If you worked for multiple employers throughout your career, you might have vested pension benefits that you have forgotten about. It pays to retrace your work history, especially for companies you left decades ago. Some corporations undergo mergers or bankruptcies, transferring their pension obligations to the Pension Benefit Guaranty Corporation (PBGC), a federal agency that ensures retirees still receive their promised checks.

Annuities represent another form of guaranteed income, usually purchased through an insurance company. If you or your spouse bought a fixed annuity years ago, it will generate a steady monthly check once you activate the payout phase. Managing these dual income streams requires careful budgeting, as both private pensions and annuity distributions typically count as taxable income.

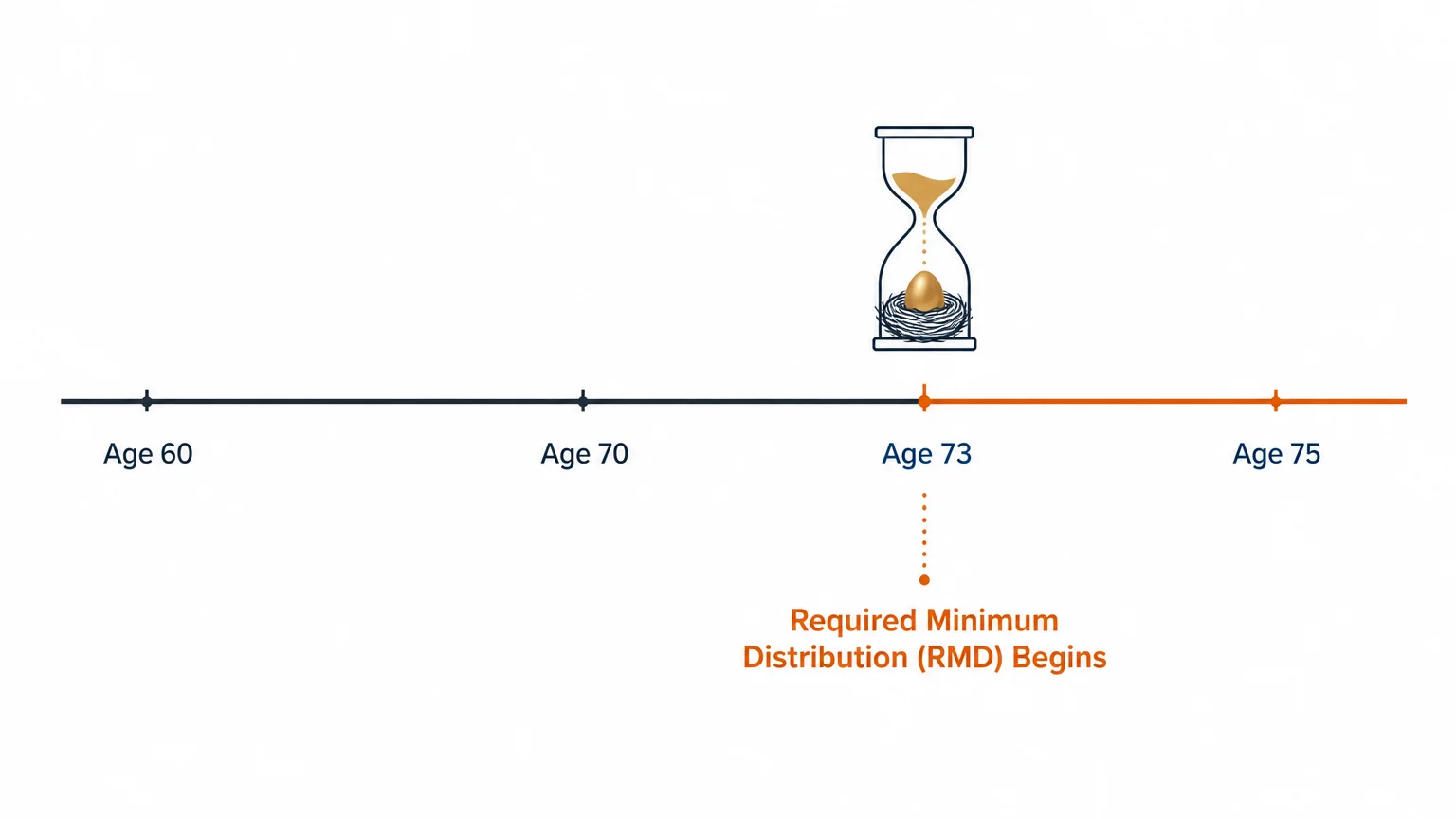

Required Minimum Distributions (RMDs)

Not all additional checks are optional. Once you reach a certain age—currently age 73—the federal government requires you to start pulling money out of your tax-deferred retirement accounts, such as Traditional IRAs and 401(k) plans. These mandatory withdrawals are known as Required Minimum Distributions (RMDs).

Because you avoided paying taxes on these funds when you originally contributed them, the IRS eventually wants its share. By forcing you to take an RMD, the government creates a taxable event. Your brokerage or financial institution will calculate the exact amount you must withdraw based on your account balance and your life expectancy, cutting you a check or depositing the funds directly into your bank account.

While an RMD acts as an extra income source, you must manage it carefully. Failing to take your full RMD by the December 31 deadline results in a harsh penalty. The IRS can levy an excise tax of up to 25 percent on the amount you were supposed to withdraw but did not. Working with a financial advisor can help you schedule your RMD checks efficiently to minimize the tax impact.

Nutrition and Utility Assistance

While not always distributed as a traditional paper check, government assistance programs that cover food and utility costs effectively put cash back into your bank account. By freeing up money you would otherwise spend on basic necessities, these programs act just like supplementary income.

The Supplemental Nutrition Assistance Program (SNAP) provides monthly funds on an Electronic Benefits Transfer (EBT) card, which you can use to purchase groceries. Many seniors assume they make too much money to qualify for SNAP, but the income deductions allowed for medical expenses and high housing costs often make older adults eligible even if their gross income seems too high.

The Low Income Home Energy Assistance Program (LIHEAP) is another critical resource. It issues direct payments to your utility provider to help cover the costs of heating and cooling your home. According to the Administration for Community Living (ACL), securing assistance with daily nutrition and utility costs helps older adults maintain their independence and stay in their homes longer without sacrificing their health or comfort.

Here is a quick overview comparing common supplemental income sources:

| Income Source | Who Qualifies? | Frequency | Tax Status |

|---|---|---|---|

| Supplemental Security Income (SSI) | Seniors 65+ with very low income/assets | Monthly | Generally Tax-Free |

| VA Aid and Attendance | Eligible veterans needing daily personal care | Monthly | Tax-Free |

| State Circuit Breaker Rebates | Homeowners/renters with high property tax burdens | Annually | Varies by State |

| Traditional IRA RMDs | Retirees aged 73 and older | Annually or Monthly | Fully Taxable |

How to Find Unclaimed Money

Millions of dollars in unclaimed funds sit in state treasuries across the country, waiting to be claimed by their rightful owners. Retirees frequently move, change their names, or simply forget about minor financial accounts over a long lifetime. When banks, insurance companies, or former employers cannot locate you, they turn the money over to the state government.

These forgotten funds can include:

- Uncashed dividend or payroll checks.

- Dormant savings or checking accounts.

- Refunds from utility companies or former landlords.

- Payouts from forgotten life insurance policies.

- Contents of abandoned safe deposit boxes.

You can search for these funds for free using state-sponsored unclaimed property websites. Always search under your current name, your maiden name, and any previous addresses where you lived. Reclaiming this money usually requires filling out a simple form and providing proof of identity, after which the state treasury will mail you a check for the missing balance.

Avoiding Financial Scams

Whenever there is talk of “extra government checks” or “hidden senior benefits,” scammers take notice. Criminals aggressively target older adults with schemes designed to steal sensitive personal information or drain their bank accounts.

A common tactic involves a phone call or email from someone pretending to be an agent from the Social Security Administration or Medicare. The scammer might claim that you are eligible for a sudden bonus check or an inflation relief grant, but insist that you must pay a processing fee or verify your bank account details first to receive the funds.

As noted by experts at the Consumer Financial Protection Bureau (CFPB), you should never pay a fee to claim a government benefit or prize. Legitimate government agencies will never demand payment via wire transfer, cryptocurrency, or retail gift cards. If you receive an unexpected call promising additional checks, hang up immediately. Navigate directly to the official government website and call their public helpline to verify the claim.

Keep these protective measures in mind:

- Never share your Social Security number with an inbound caller.

- Do not click links in text messages claiming your benefit check is pending.

- Check your mail carefully; verify unexpected physical checks with the issuing institution before cashing them to avoid fake check scams.

- Monitor your bank statements monthly for unauthorized small charges.

Frequently Asked Questions

Can I receive SSI and regular Social Security at the same time?

Yes, this is known as receiving “concurrent benefits.” If your standard Social Security retirement check is very low and you meet the strict income and asset requirements, you can receive an SSI check to supplement your monthly income up to the federal minimum standard.

Will my VA benefits reduce my Social Security payments?

No, your Veterans Affairs (VA) benefits do not affect your Social Security retirement payments. You can collect your full Social Security benefit alongside your VA Disability Compensation or VA Pension without any offsets or penalties.

Do I have to pay taxes on these additional checks?

It depends entirely on the source of the check. VA disability benefits, SSI, and most state inflation relief checks are generally tax-free. However, distributions from traditional pensions, annuities, and Required Minimum Distributions (RMDs) are usually taxed as ordinary income at the federal level.

How do I know if I have a forgotten pension?

If you suspect a former employer owes you pension benefits, start by contacting their human resources department. If the company went bankrupt or merged, search the Pension Benefit Guaranty Corporation (PBGC) database. The PBGC protects private-sector pensions and holds funds for missing participants.

What should I do if I receive a check in the mail I was not expecting?

Do not deposit or cash it immediately. Unsolicited checks are often the bait in “overpayment” scams, where the sender asks you to return a portion of the funds before the fake check inevitably bounces. Verify the source of the check by contacting the issuing bank or government agency directly using a verified public phone number.

For additional senior resources, visit

National Institutes of Health (NIH), Centers for Medicare & Medicaid Services (CMS), Social Security Administration (SSA), Consumer Financial Protection Bureau (CFPB) and Administration for Community Living (ACL).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply