You depend on Social Security as a foundational pillar of your retirement income, but recent headlines about funding gaps might leave you feeling uncertain. The 2026 Social Security Trustees Report has updated the timeline for the program’s trust funds, and understanding these projections is critical for your financial security. Instead of worrying about sensationalized news, you need clear facts about what changes are actually on the horizon. By examining the latest expert analysis and demographic shifts, you can make informed decisions to protect your long-term wealth. This guide cuts through the noise, breaks down the proposed legislative fixes, and offers concrete steps to help you build a resilient retirement strategy regardless of what happens in Washington.

Understanding the 2026 Social Security Trustees Report

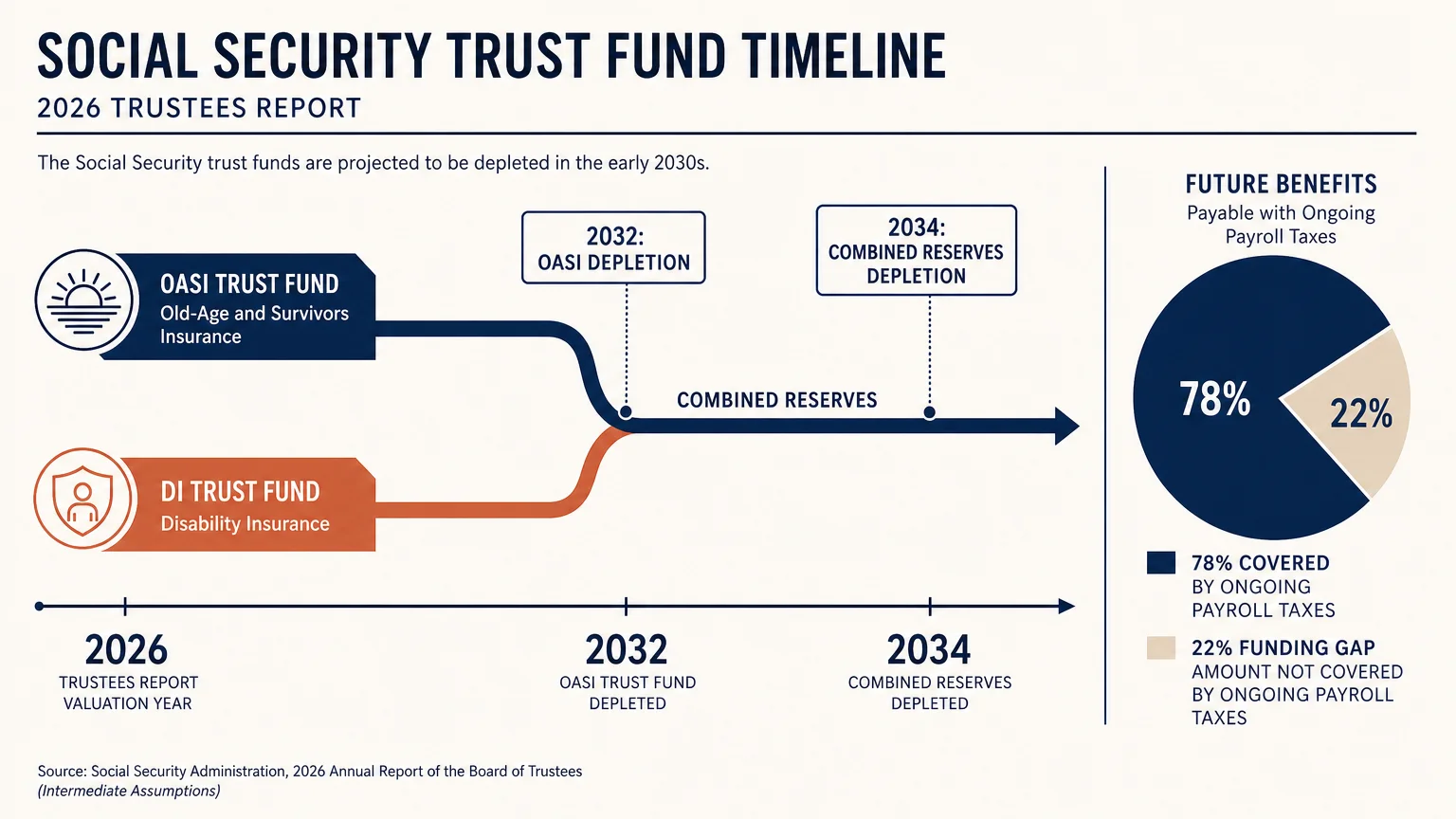

To grasp the future of your benefits, you first need to understand how the system holds its money. Social Security does not store all of its funds in a single giant bank account. Instead, the program relies on two primary trusts. The Old-Age and Survivors Insurance (OASI) trust fund pays your standard retirement and survivor benefits. Meanwhile, the Disability Insurance (DI) trust fund supports younger workers who can no longer perform their jobs due to severe medical conditions.

Recent projections published by the Social Security Administration (SSA) indicate that the combined reserves for these two funds face depletion by 2034. If you look exclusively at the OASI trust fund—the specific pool of money responsible for your monthly retirement checks—the forecast is slightly more pressing, with an estimated depletion date of 2032.

However, the word “depletion” causes unnecessary panic. Depletion does not mean the program is going bankrupt, nor does it mean your benefits will suddenly drop to zero. Social Security operates on a pay-as-you-go model. Today’s active workforce continually funds the program through payroll taxes taken directly out of their paychecks. Even if the reserve funds run completely dry, ongoing tax revenues will still pour into the system. Experts estimate these incoming taxes would be sufficient to cover approximately 78% of all scheduled benefits. While a potential 22% reduction is a serious issue that demands legislative attention, it is far from the total systemic collapse often portrayed on television.

You have worked hard for your benefits, and it is completely normal to feel concerned when you hear these dates. But by understanding the actual numbers, you can approach your retirement planning logically rather than reacting out of fear.

Why the Funding Gap Exists

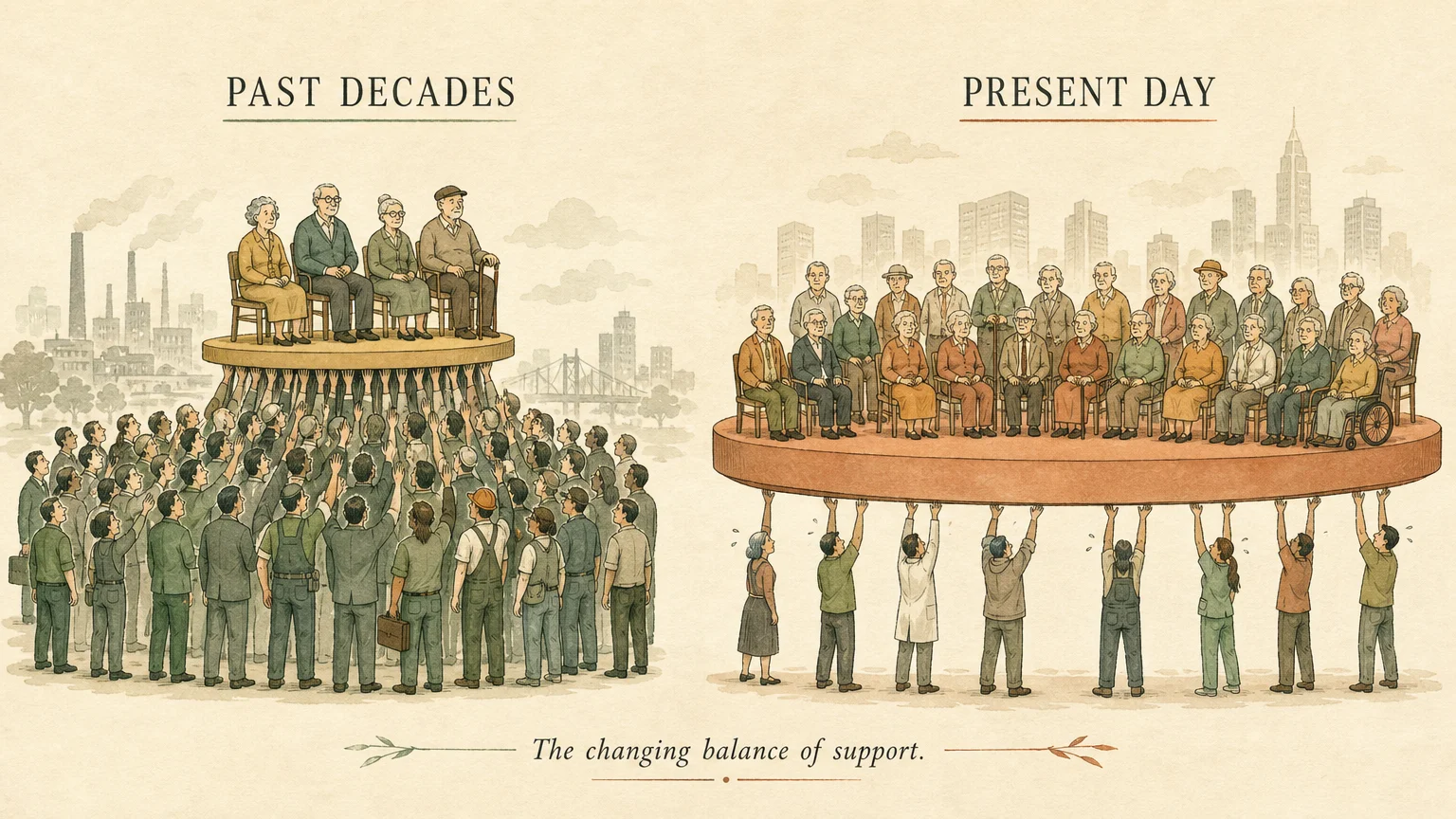

You might wonder how a program that has run successfully for decades suddenly faces a massive financial shortfall. The answer lies primarily in the shifting shape of the American population. When Social Security was designed, life expectancy was lower, and families were generally larger. Today, the math has changed dramatically.

The core issue revolves around the worker-to-beneficiary ratio. In the 1950s, there were more than a dozen workers paying taxes to support every single retiree. Today, as the massive Baby Boomer generation transitions out of the workforce, that ratio has plummeted to fewer than three workers per retiree. The 2026 Trustees Report highlights that the assumed ultimate fertility rate has dropped to just 1.75 children per woman. Because families are having fewer children, the future workforce is shrinking relative to the growing senior population.

Compounding the lower birth rates are recent shifts in immigration. Lower projections for temporary and permanent immigration mean fewer new, younger workers are entering the labor market to bolster the tax base. Additionally, the Congressional Budget Office recently projected that domestic deaths will surpass domestic births sooner than previously expected. This demographic squeeze means more money is flowing out of the trust funds than is flowing in.

Finally, experts point to growing income disparities as a contributing factor. Social Security taxes only apply to earnings up to a specific cap—which sits at $184,500 in 2025. Any income a worker earns above that threshold is exempt from the payroll tax. Because high earners have seen their wages grow much faster than middle-class workers, a significant and growing portion of national income now falls completely outside the taxable cap, further starving the program of vital revenue.

Proposed Legislative Solutions to Protect Benefits

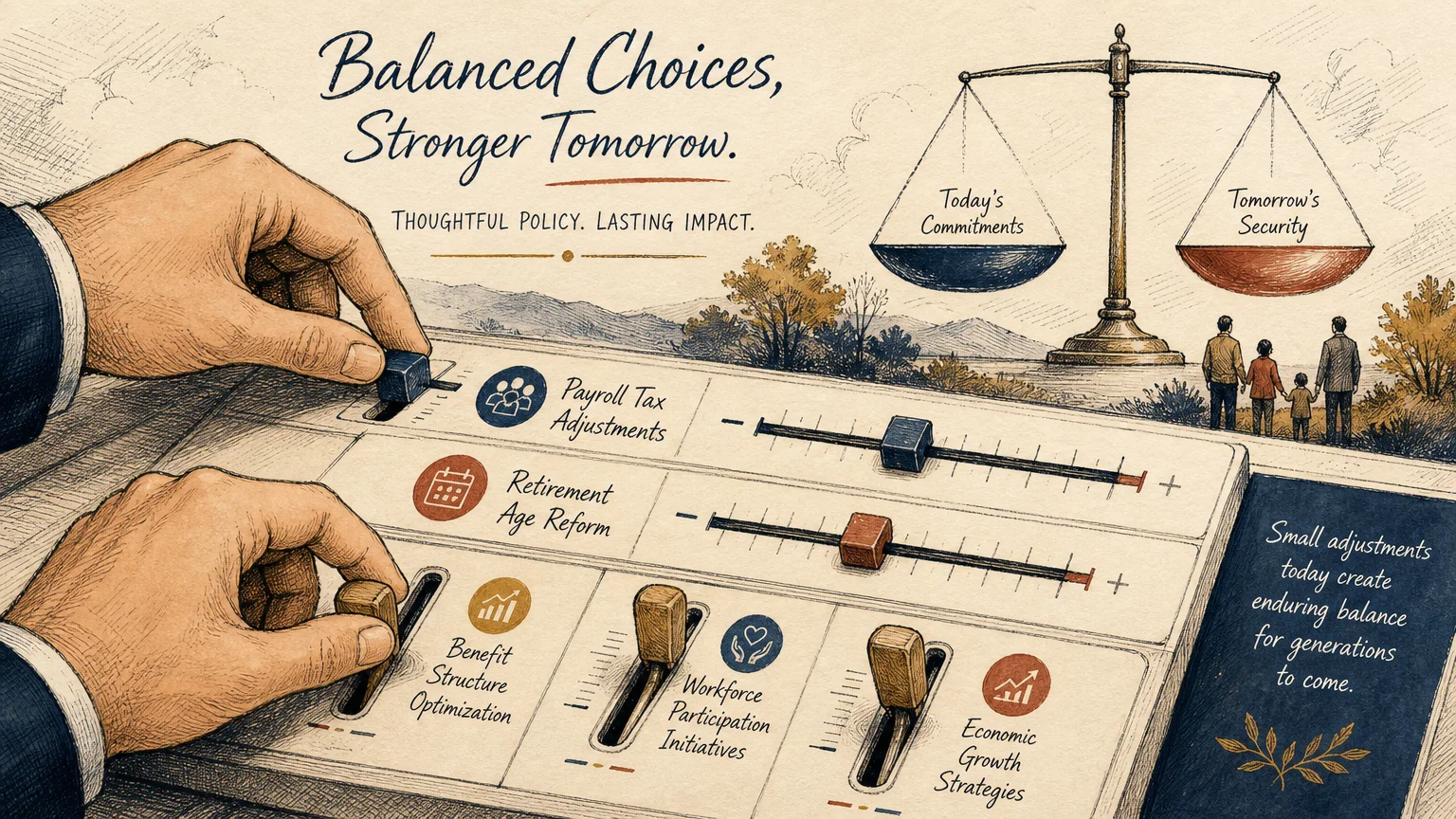

Because the fundamental problem is mathematical, the solutions must be mathematical as well. Congress basically has two levers to pull: they can increase the amount of money coming into the system, or they can decrease the amount of money flowing out.

Given the rapidly approaching 2032 and 2034 deadlines, lawmakers will soon have to make difficult choices. According to policy experts at AARP, Congress must act sooner rather than later to protect current retirees and allow future retirees enough time to smoothly adjust their financial plans. History shows that Congress often waits until the last minute to pass comprehensive reforms, but several prominent strategies are already being debated in Washington.

To help you understand what might be coming, here is a breakdown of the most widely discussed legislative proposals:

| Proposed Solution | How It Works | Potential Impact on Retirees |

|---|---|---|

| Raising the Full Retirement Age (FRA) | Gradually increasing the age at which you can claim 100% of your benefits from 67 to 68 or 69. | Future retirees would need to wait longer to receive full payouts. Those who still claim early at 62 would face steeper permanent reductions. |

| Increasing or Removing the Tax Cap | Raising the $184,500 earnings cap so higher-income workers pay Social Security taxes on more, or all, of their income. | This would bring massive revenue into the system without directly reducing benefits for middle- and lower-income seniors. |

| Modifying Benefits for High Earners | Adjusting the payout formula so that wealthy retirees receive slightly smaller monthly checks compared to middle-class workers. | Seniors with significant private wealth or high lifelong earnings would see reduced payouts, preserving the trust fund for those who rely on it most. |

| Increasing the Payroll Tax Rate | Raising the current 12.4% tax rate (split evenly between employer and employee) to a higher percentage. | Active workers would take home slightly less pay, but the immediate influx of cash would rapidly stabilize the trust funds. |

It is highly likely that any final legislation will involve a combination of these proposals. A balanced approach ensures that neither current retirees nor younger workers bear the entire burden of fixing the system.

How a Potential Benefit Reduction Could Impact Your Retirement

If partisan gridlock prevents Congress from passing any reforms, the law mandates an automatic, across-the-board benefit cut once the reserves are depleted. Based on current estimates, this cut would amount to approximately 22%. It is essential to look past the percentages and consider what this actually means for your daily life.

Imagine your monthly Social Security check is $2,000. A 22% reduction instantly removes $440 from your budget, bringing your payment down to $1,560. Over the course of a year, that is a loss of $5,280. For seniors living on a fixed income, losing over five thousand dollars annually can mean the difference between living comfortably and struggling to pay for basic necessities like utilities, groceries, and property taxes.

This potential reduction is especially concerning because it does not account for the rising cost of living. Healthcare costs, housing, and food naturally increase over time. Facing higher expenses with a significantly reduced income requires careful, proactive planning today.

Do not panic, but do be pragmatic. The likelihood of Congress allowing a 22% benefit cut to hit millions of voting seniors is incredibly low. Such an event would be political suicide for lawmakers. Nevertheless, smart retirement planning requires you to prepare for the worst while expecting the best. By acknowledging the worst-case scenario, you can stress-test your current financial strategy and find areas for improvement.

Actionable Steps to Safeguard Your Retirement Income

You cannot control what happens in Congress, but you can absolutely control how you prepare your own finances. Building a resilient retirement plan means creating multiple streams of income so that a disruption in any single area does not devastate your lifestyle.

To insulate yourself from potential future cuts, consider implementing the following strategies:

- Optimize your claiming age: If you are healthy and have sufficient savings to live on, delaying your Social Security application is one of the most powerful moves you can make. For every year you wait past your Full Retirement Age (up to age 70), your benefit permanently increases by 8%. Building a larger baseline benefit now means you will still have a robust income even if a percentage cut is applied later.

- Diversify your income streams: Do not rely on government benefits alone. Maximize your withdrawals from traditional IRAs, Roth IRAs, and 401(k) accounts. If you have a pension, factor it into your monthly budget. Some seniors also explore part-time consulting, turning a hobby into a small business, or purchasing fixed annuities to guarantee a steady flow of private income.

- Aggressively manage healthcare expenses: Healthcare is often a senior’s largest expense. To protect your cash flow, you must shop smart. Using the official plan finder tool on Medicare.gov allows you to evaluate and compare your Part D prescription drug plans and Medicare Advantage options every single year. Switching to a more cost-effective plan can free up hundreds of dollars in your budget.

- Build a liquid cash buffer: Maintain a dedicated emergency fund holding six to twelve months of essential living expenses in a high-yield savings account. If Congress implements a clumsy legislative fix that delays checks or temporarily reduces benefits, this cash buffer ensures you can pay your bills without liquidating your long-term investments at a loss.

- Downsize or leverage home equity: If you live in a large home that requires constant maintenance, downsizing can radically lower your property taxes, utility bills, and insurance premiums. Alternatively, exploring a reverse mortgage might provide a tax-free stream of income, though you should consult a fiduciary advisor before taking this complex step.

By taking these steps, you build a financial fortress around your retirement. A balanced, diversified approach ensures you can maintain your dignity and independence no matter how Social Security evolves.

Common Misconceptions and Scam Warnings

When the news cycle focuses on funding shortfalls, misinformation spreads rapidly. One of the most dangerous myths is the belief that you should rush to claim your benefits at age 62 before the money “runs out.” Claiming at 62 permanently slashes your monthly check by up to 30% compared to your Full Retirement Age amount. If you lock in that massive penalty out of fear, and then Congress later applies a structural reduction, your monthly payout will shrink to a dangerously low level. Always base your claiming decision on your health, your savings, and your marital status—not on alarming headlines.

Another prevalent misconception is that politicians have “stolen” the trust fund money. By law, the Social Security Administration must invest all surplus funds into special-issue U.S. Treasury bonds. These bonds are backed by the full faith and credit of the United States government and earn interest. The money has not been stolen; it is securely invested exactly as the law requires.

Unfortunately, fraudsters use headlines about trust fund depletion to frighten older adults. As noted by the Consumer Financial Protection Bureau (CFPB), scammers frequently exploit news cycles to steal your personal information. A criminal might call you, claiming to be an official from the Social Security Administration. They will assert that your benefits are about to be canceled due to the trust fund crisis, but offer to “protect” your account if you pay a fee or provide your Social Security number.

Never fall for these aggressive tactics. The real Social Security Administration will never call you out of the blue to threaten your benefits. They will never demand payment via gift cards, wire transfers, or cryptocurrency. If you receive a suspicious call, hang up immediately and contact the agency directly using their official public phone numbers.

Frequently Asked Questions

Will I lose my Social Security benefits completely in 2034?

No, you will not lose your benefits completely. Social Security is continuously funded by the payroll taxes of active workers. Even if the trust fund reserves are entirely depleted in 2034, incoming taxes are projected to cover roughly 78% of scheduled benefits. You will still receive a check, though it may be smaller if Congress fails to enact legislative reforms.

Should I claim my benefits early to avoid future cuts?

For most people, claiming early out of fear is a costly mistake. If you claim at age 62, you lock in a permanent reduction of up to 30%. Waiting until your Full Retirement Age or delaying until age 70 ensures a much larger baseline benefit. A larger baseline provides a better financial cushion if a percentage cut is eventually applied.

How do the proposed legislative changes affect seniors who are already receiving benefits?

Historically, Congress tries to shield current retirees and those nearing retirement from severe policy changes. During the major reforms of 1983, changes to the retirement age were phased in gradually over several decades. While nothing is guaranteed, most modern proposals focus on altering the rules for younger generations or raising taxes on current high-income earners, rather than cutting the checks of seniors already relying on the system.

Are my Medicare benefits tied to the Social Security trust fund?

No, Medicare is funded through separate trust funds. While the Medicare Hospital Insurance (Part A) trust fund faces its own financial challenges and deadlines, it operates independently of the Social Security Old-Age and Survivors Insurance (OASI) trust fund. A shortfall in Social Security does not automatically mean a direct cut to your Medicare coverage.

How can I find out exactly how much I am scheduled to receive?

The best way to understand your future benefits is to create a free, secure “my Social Security” account on the official SSA website. This portal provides you with personalized statements detailing your earnings history and projected monthly payouts at various claiming ages, allowing you to plan your retirement with accurate, real-time data.

For additional senior resources, visit

Centers for Medicare & Medicaid Services (CMS), Social Security Administration (SSA), Consumer Financial Protection Bureau (CFPB), Administration for Community Living (ACL) and Eldercare Locator.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply