Navigating your retirement finances often hinges on understanding how your benefits actually work, yet many seniors fall into traps caused by outdated or incorrect information. Social Security serves as the financial foundation for millions of older Americans, making it critical to separate fact from fiction before making permanent claiming decisions. A single misunderstanding about your full retirement age, spousal benefits, or taxation rules can cost you thousands of dollars over your lifetime. By clearing up the most widespread myths, you can maximize your monthly income, protect your surviving spouse, and plan your future with absolute confidence. Let us explore the exact rules you need to know to secure the benefits you spent a lifetime earning.

The Age You Claim Changes Everything

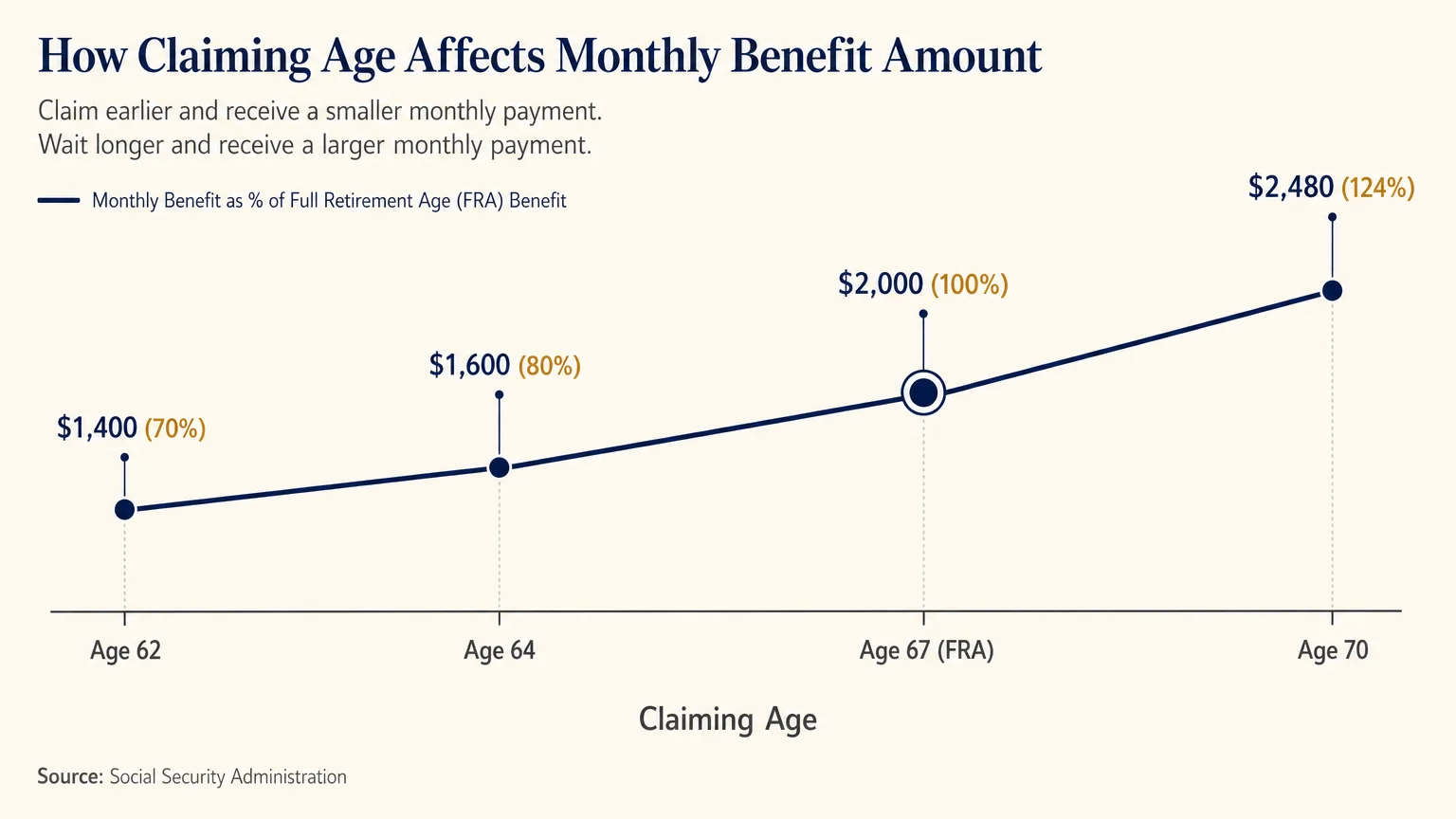

One of the most persistent misunderstandings surrounding retirement is the belief that claiming at age 62 is always the best financial decision. Many seniors fear the program will run out of money or simply want to access their cash as soon as possible. While taking early benefits provides immediate income, it severely reduces your monthly check for the rest of your life. Your Full Retirement Age (FRA) dictates when you are eligible to receive 100% of your earned benefit; depending on your birth year, your FRA falls between age 66 and 67.

Claiming at age 62 results in a permanent reduction of up to 30% of your monthly benefit. Conversely, waiting past your FRA triggers delayed retirement credits. According to the Social Security Administration (SSA), delaying your benefits beyond your full retirement age increases your monthly payment by 8% per year until you reach age 70. This guaranteed growth is difficult to match in traditional investment markets, making patience a highly lucrative strategy for seniors with average or above-average life expectancies.

Consider the concrete financial impact of your claiming age. The table below illustrates how a baseline benefit of $2,000 at a Full Retirement Age of 67 changes based on when you initiate your payments.

| Claiming Age | Percentage of Benefit Received | Monthly Payment (Based on $2,000 FRA) |

|---|---|---|

| Age 62 | 70% | $1,400 |

| Age 64 | 80% | $1,600 |

| Age 67 (FRA) | 100% | $2,000 |

| Age 70 | 124% | $2,480 |

Before rushing to file the moment you turn 62, evaluate your health, your family longevity, and your other sources of income. If you can draw down from an IRA or 401(k) to delay your Social Security application, you lock in a higher, inflation-protected income stream for your later years.

Working While Receiving Benefits

Many seniors want to transition slowly into retirement by working part-time. A widespread myth is that working while receiving Social Security completely disqualifies you from your benefits or causes you to lose that money permanently. The reality involves a specific set of rules known as the earnings test, which only applies if you claim benefits before reaching your Full Retirement Age.

If you take benefits early and continue to earn income from a job, you are subject to an annual earnings limit. For earnings above this limit, the government withholds $1 in benefits for every $2 you earn. In the year you reach your FRA, the limit increases significantly, and the withholding ratio changes to $1 for every $3 earned above the higher threshold. Once you reach the exact month of your Full Retirement Age, the earnings limit disappears entirely; you can earn a million dollars a year, and your Social Security check will not be reduced by a single penny.

The most important part of this rule is the part most seniors misunderstand: the withheld money is not gone forever. When you reach your FRA, the administration recalculates your benefit upward to account for the months your check was reduced. Over time, you recoup those withheld funds through higher monthly payments. Therefore, you should not let the fear of the earnings test completely deter you from working if a part-time job provides personal fulfillment and needed cash flow.

Spousal and Survivor Benefits Confusion

Marital status heavily influences your retirement income options, yet spousal and survivor benefits remain widely misunderstood. A common assumption is that a spouse who never worked outside the home—or who earned very little—cannot receive Social Security. The system provides a spousal benefit that allows a non-working or lower-earning spouse to claim up to 50% of the higher earner’s Full Retirement Age benefit.

To maximize this advantage, you must understand the dual entitlement rule. The government always pays your own earned benefit first. If your spousal benefit is higher than your own benefit, they add an additional amount to bring your total payment up to the spousal level. You cannot receive both your full individual benefit and the full spousal benefit simultaneously.

Divorced individuals frequently miss out on benefits due to lack of knowledge. If you were married for at least 10 consecutive years and have not remarried, you can claim benefits based on your ex-spouse’s earnings record. Your ex-spouse never needs to know you filed, and your claim does not reduce their benefit or the benefit of their current spouse.

Survivor benefits follow an entirely different set of rules that demand careful planning. When one spouse passes away, the surviving spouse inherits the higher of the two monthly checks, while the smaller check disappears. Research from AARP emphasizes that coordinating claiming strategies between spouses is essential to protect the surviving partner. If the higher earner delays claiming until age 70, they lock in the maximum possible survivor benefit for their widow or widower.

Taxes on Social Security Income

Retirees frequently experience a harsh wake-up call during their first tax season. The assumption that Social Security is entirely tax-free is fundamentally incorrect for millions of Americans. Whether you pay federal income taxes on your benefits depends on a specific formula called your “Combined Income” or “Provisional Income.”

You calculate your combined income by adding your Adjusted Gross Income (AGI), any nontaxable interest (such as municipal bond interest), and exactly half of your yearly Social Security benefits. Once you have that total, you compare it to the base thresholds established by the IRS.

- Single Filers: If your combined income falls between $25,000 and $34,000, you may have to pay income tax on up to 50% of your benefits. If your combined income exceeds $34,000, up to 85% of your benefits may be taxable.

- Joint Filers: If you and your spouse have a combined income between $32,000 and $44,000, up to 50% of your benefits may be taxable. If your combined income is more than $44,000, up to 85% of your benefits may be subject to income tax.

It is crucial to note that paying taxes on 85% of your benefits does not mean you surrender 85% of your check to the government. It means that 85% of your Social Security income is added to your taxable income and taxed at your normal marginal tax rate. Additionally, depending on where you live, you might also owe state income taxes on your benefits. Knowing these thresholds allows you to plan your withdrawals from traditional IRAs and 401(k)s strategically to minimize the tax impact on your Social Security.

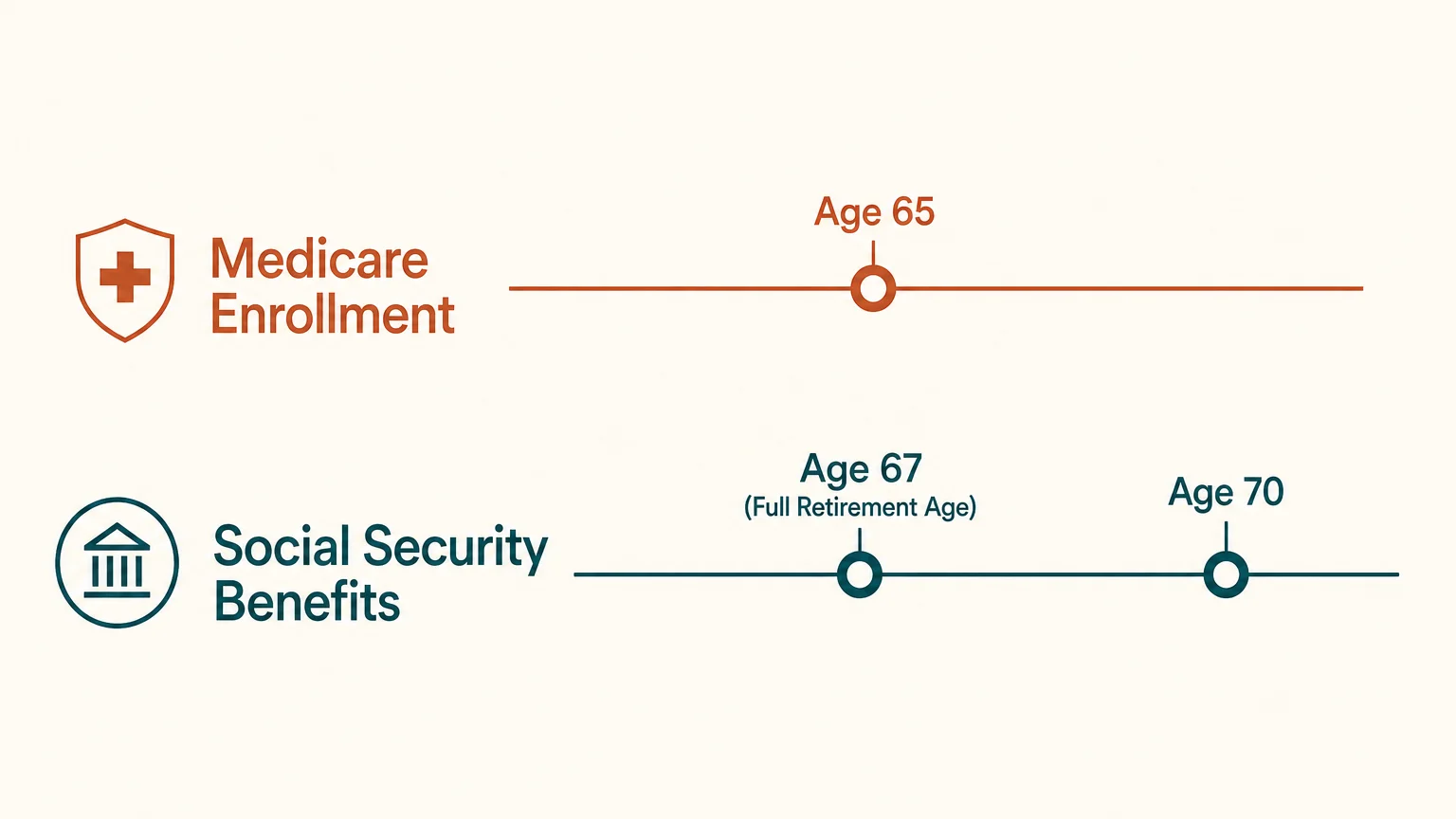

Medicare and Social Security Enrollment Differences

Because Medicare and Social Security serve the same demographic, seniors often blur the lines between the two programs. The most dangerous misunderstanding is assuming that applying for one automatically handles the other, or that the eligibility ages are identical.

Medicare eligibility begins firmly at age 65 for the vast majority of Americans. Social Security eligibility begins at 62, reaches full status between 66 and 67, and maxes out at 70. These different timelines create an administrative gap that trips up many retirees.

If you are already receiving Social Security benefits when you turn 65, the government will automatically enroll you in Medicare Part A (Hospital Insurance) and Part B (Medical Insurance). However, if you choose to delay your Social Security benefits to grow your monthly check, you must take proactive steps. According to guidelines provided by Medicare.gov, you must actively sign up for Medicare during your Initial Enrollment Period—a seven-month window surrounding your 65th birthday. Failing to enroll in Medicare on time because you were waiting to claim Social Security will result in permanent late enrollment penalties and potential gaps in your health coverage.

Keep these separate timelines clearly defined in your retirement plan. Set calendar reminders for your 65th birthday to handle Medicare, completely independent of when you plan to start your monthly income checks.

Cost of Living Adjustments Explained

Inflation devours purchasing power, making the Cost of Living Adjustment (COLA) a lifeline for retirees on fixed incomes. Yet, many seniors misunderstand how COLA is calculated and expect it to cover all their increased expenses perfectly. The adjustment is not a random percentage chosen by politicians; it is tied to a specific economic metric called the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

The government looks at the inflation data from July, August, and September of the current year and compares it to the same period from the previous year. If there is an increase, benefits rise by that percentage starting in January. If there is no inflation, or if prices drop, benefits stay exactly the same—they never decrease due to a negative COLA.

The primary disconnect seniors experience is that the CPI-W measures the spending habits of younger, working-age people. It heavily weights expenses like gasoline, electronics, and apparel. Seniors, however, spend a vastly disproportionate amount of their income on healthcare and housing. Because medical costs typically rise much faster than general inflation, the annual COLA often feels inadequate. Furthermore, when the COLA increases your gross check, Medicare Part B premiums usually increase at the same time and are deducted directly from your payment. This dynamic means your net cash increase might be substantially smaller than the headline COLA percentage suggests.

Common Scams Targeting Seniors

Financial predators ruthlessly target seniors by exploiting their reliance on Social Security. The complexity of the system makes it easy for scammers to trigger panic and compliance. Recognizing these fraudulent tactics is your strongest defense against financial devastation.

The most pervasive scam involves a phone call from someone claiming to be a government agent. The caller will state that your Social Security number has been “suspended” due to suspicious activity, a frozen bank account, or an outstanding warrant. They then demand immediate payment—often via wire transfer, cryptocurrency, or retail gift cards—to resolve the issue and restore your benefits. According to the Consumer Financial Protection Bureau (CFPB), government agencies will never demand payment over the phone or ask you to wire money to resolve an issue.

Protect yourself by adhering to these strict rules:

- The administration primarily communicates through formal letters sent via the U.S. Postal Service. They rarely call you unless you have an ongoing case and requested contact.

- Never provide your full Social Security number, bank account details, or Medicare number to an unsolicited caller.

- If you receive a threatening call, hang up immediately. Do not press “1” to speak to an operator, and do not trust the Caller ID, as scammers frequently spoof official phone numbers.

- Create a secure online account on the official government website to monitor your earnings record and check the status of your benefits safely.

How to Fix Social Security Mistakes

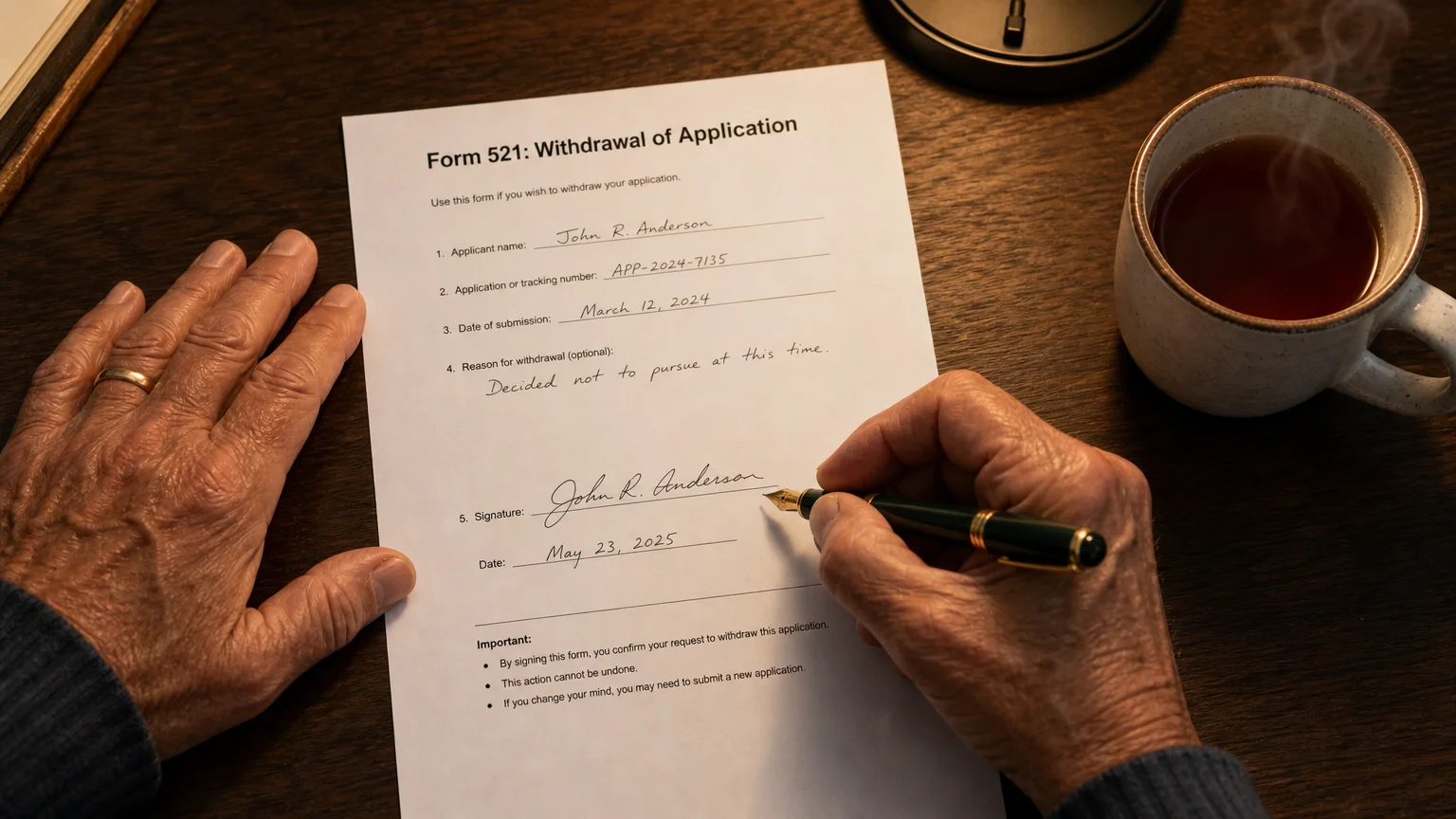

Making a decision about your retirement income can feel paralyzing because it seems painfully permanent. What happens if you claim early out of fear, but then secure a great part-time job or realize you have enough savings to wait? A major misunderstanding is the belief that you have absolutely no options once you receive your first check.

The system actually provides a “do-over” option, though it comes with strict conditions. If you change your mind within 12 months of your original application date, you can withdraw your claim using Form SSA-521. This action completely cancels your application, allowing your benefits to continue growing until you claim them again in the future.

The critical catch is that you must repay every single penny you and your family received based on your application. This includes your monthly checks, any spousal benefits paid on your record, and any Medicare premiums that were withheld from your payments. You only get one opportunity to withdraw your application in your lifetime.

If you miss the 12-month window, you have a second option once you reach your Full Retirement Age. You can voluntarily suspend your benefits. During the suspension period, you will not receive monthly checks, but your benefit will earn the 8% annual delayed retirement credits until age 70. This strategy allows you to boost your final permanent income and increase the future survivor benefit for your spouse, even if you initially claimed early.

Frequently Asked Questions

Do I pay Social Security taxes if I keep working after claiming?

Yes. If you continue to work for an employer or run a business, you must continue to pay FICA taxes on your earnings, regardless of your age or whether you are already receiving benefits. These taxes are mandatory for all earned income. However, these new earnings could potentially increase your benefit amount. The administration reviews your earnings record annually; if your current salary is higher than one of the 35 years used to calculate your initial benefit, they will recalculate and increase your monthly payment.

Will my benefits automatically increase when my spouse dies?

Survivor benefits are not always automatic, which causes immense frustration for grieving widows and widowers. If you are already receiving spousal benefits on your partner’s record, the administration will typically convert that to a survivor benefit automatically once the death is reported. However, if you are receiving benefits on your own work record and your deceased spouse had a higher benefit, you must proactively apply for survivor benefits to receive the higher amount. Always contact the administration directly to review your options following the passing of a spouse.

Can my children receive benefits if I retire?

Yes, under specific circumstances. If you are receiving retirement benefits, your unmarried children can receive monthly payments if they are under age 18 (or up to age 19 if attending elementary or secondary school full-time). Additionally, children who were severely disabled before the age of 22 can receive benefits based on your earning record indefinitely. The child’s benefit can be up to 50% of your full retirement amount, subject to a maximum family limit.

How do I apply for benefits when the time comes?

You have three practical ways to apply for your retirement benefits. The fastest and most convenient method is to apply online through the official government website. The online application typically takes about 15 to 30 minutes to complete. Alternatively, you can apply over the phone by calling the national toll-free number, or you can schedule an in-person appointment at your local office. Experts recommend submitting your application about four months before the date you want your benefit payments to begin to ensure a smooth transition.

For additional senior resources, visit

Alzheimer’s Association, American Heart Association and Benefits.gov.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply