Your monthly expenses climb higher every time you visit the grocery store or pay a utility bill, making your annual cost of living adjustment crucial to maintaining your independence. This inflation adjustment directly impacts your ability to afford basic necessities, healthcare, and housing on a fixed income. Understanding how the Social Security update works and how to maximize your retirement benefits gives you back control over your financial future. You deserve to feel secure, rather than constantly worrying about stretching your dollars further each month. We will break down exactly how this calculation affects your daily life, outline practical ways to manage rising costs, and show you how to protect your hard-earned financial stability against unpredictable economic shifts.

Understanding the Basics of COLA

You have likely heard the term thrown around on the news every autumn, but understanding the precise mechanics of your annual COLA increase requires a brief look behind the scenes. Congress established the Cost-of-Living Adjustment (COLA) in the 1970s to ensure that the purchasing power of your retirement benefits did not erode over time. Before this legislation, seniors had to wait for special acts of Congress to see any increase in their monthly checks, which often left older Americans struggling to afford basics during periods of rapid inflation.

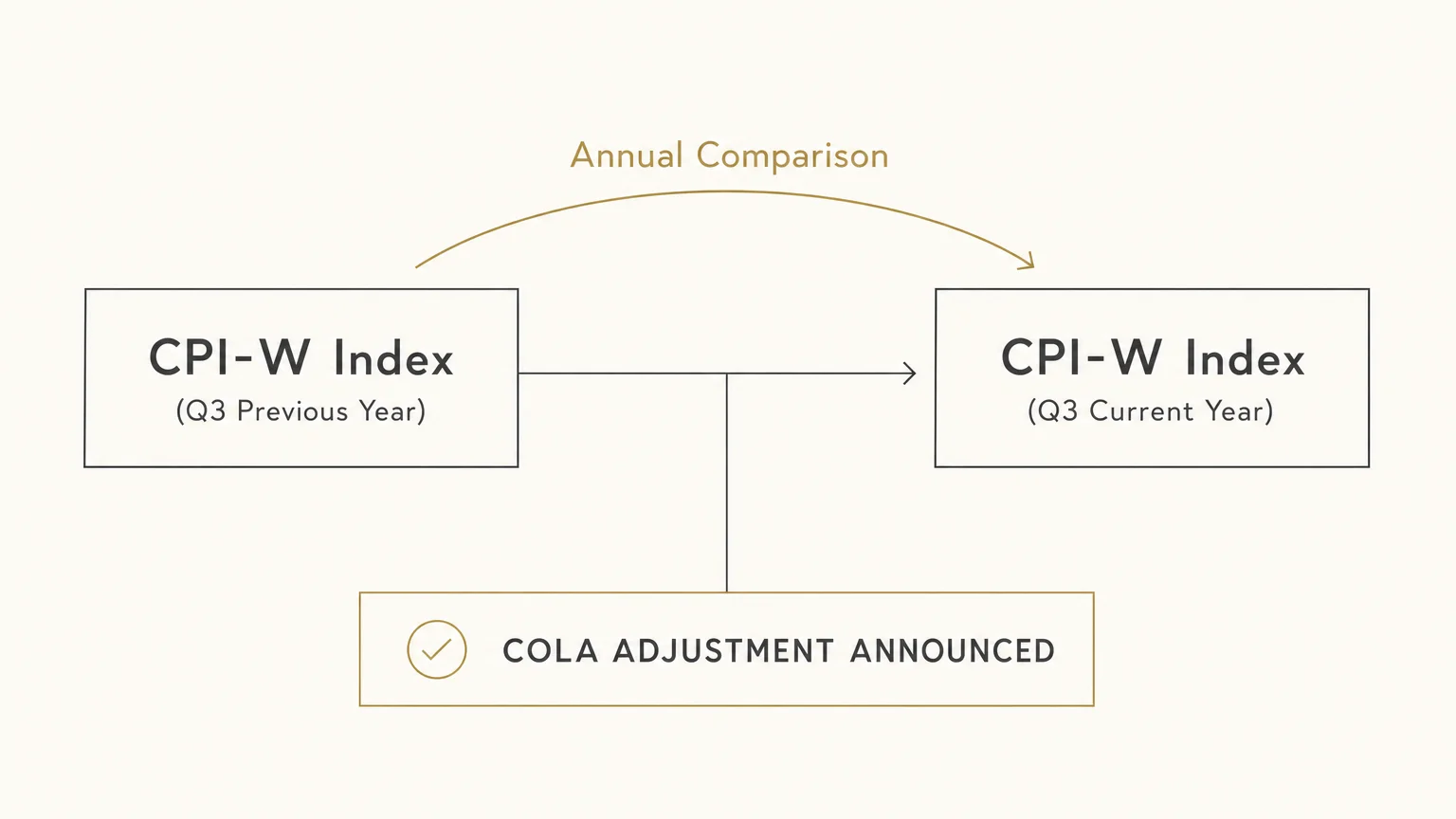

Today, the process is automatic and tied directly to national economic data. According to the Social Security Administration (SSA), the annual COLA is determined by changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). The government measures this index from the third quarter of the previous year to the third quarter of the current year. If prices go up, your monthly check goes up the following January. If prices remain flat or decrease, your check stays the exact same; the government never reduces your benefit due to negative inflation.

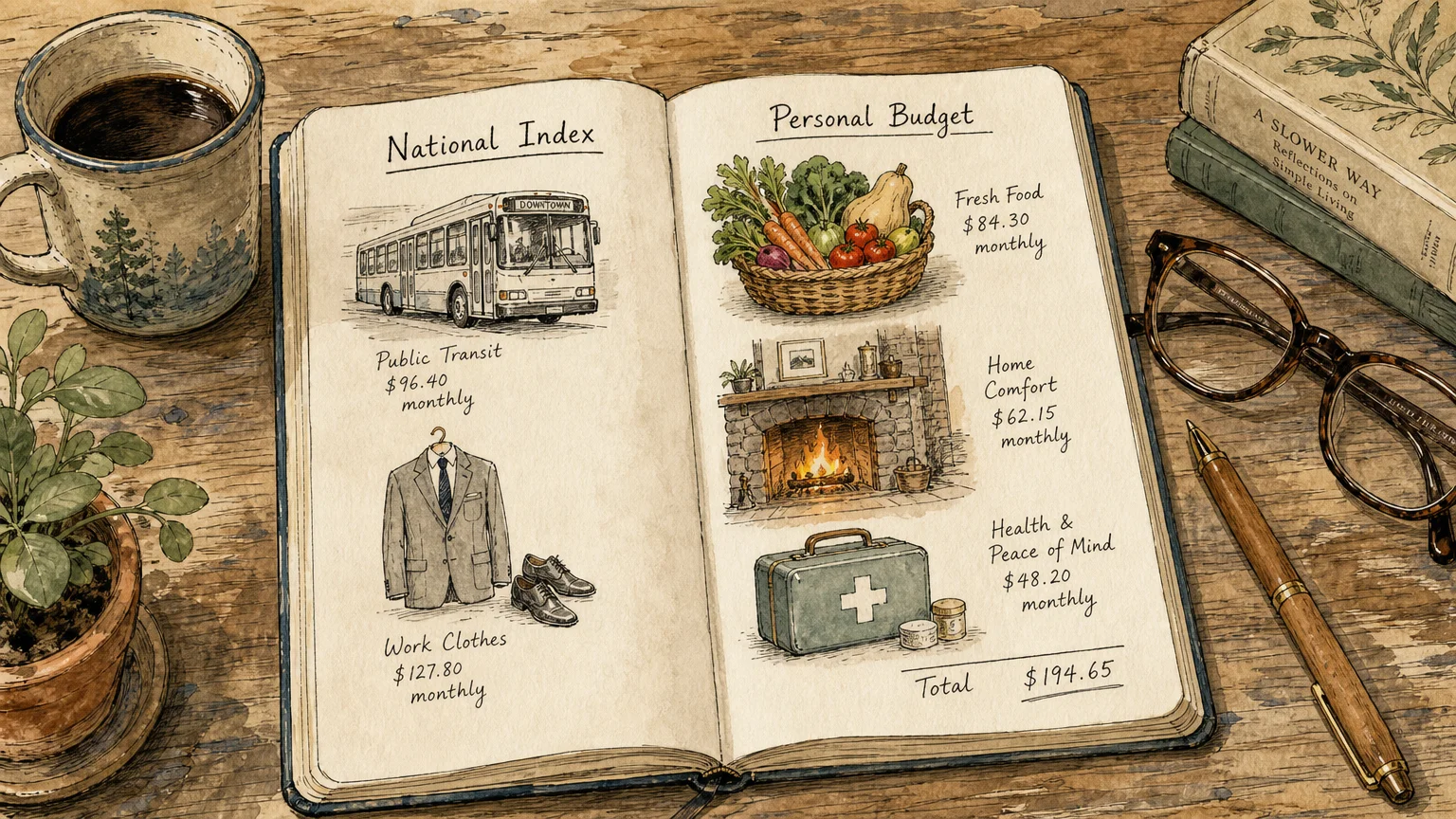

While this system provides a vital safety net, it does not always feel like enough when you actually go to spend your money. The formula measures the spending habits of urban wage earners—people who are actively commuting, buying work clothes, and paying for childcare. Your lifestyle as a retiree looks entirely different. You spend your money on different categories of goods and services, which means the official national inflation adjustment might not perfectly align with the actual price increases you face in your daily routine. Understanding this disconnect is the first step toward better financial planning.

How Inflation Impacts Your Retirement Benefits

When economists talk about inflation, they usually look at broad economic indicators, but for you, inflation is deeply personal. It is the extra fifty cents for a loaf of bread, the jump in your property taxes, and the steadily climbing cost of your prescription medications. Over the course of a twenty- or thirty-year retirement, these seemingly small price hikes compound dramatically, fundamentally altering how far your retirement benefits stretch.

To truly grasp why COLA matters more than ever nowadays, you must look at what financial experts call “purchasing power.” Purchasing power refers to the actual amount of goods or services one dollar can buy. If your Social Security check increases by three percent, but your actual household expenses jump by five percent, you effectively lose purchasing power. You might have more physical dollars hitting your bank account, but those dollars buy fewer items than they did the year before. Data from AARP highlights that older adults spend a significantly higher percentage of their income on out-of-pocket healthcare costs compared to younger demographics, making seniors uniquely vulnerable to price spikes in the medical sector.

Let us look closely at how the spending habits of seniors contrast with the broader population. The table below illustrates why the standard inflation metric often feels inadequate for retirees living on a fixed income.

| Expense Category | Impact on Urban Wage Earners (CPI-W) | Impact on Retirees (Actual Experience) |

|---|---|---|

| Transportation & Commuting | High impact (daily commuting, gas, wear and tear) | Lower impact (reduced driving, fewer commutes) |

| Healthcare & Prescriptions | Moderate impact (often subsidized by employers) | Very high impact (Medicare gaps, out-of-pocket costs) |

| Housing & Utilities | High impact (renting, upgrading homes) | High impact (property taxes, maintenance, heating) |

| Education & Childcare | High impact (tuition, daycare costs) | Minimal to no impact |

As you can see, the categories where prices rise the fastest—particularly healthcare and property taxes—make up the lion’s share of a retiree’s budget. This discrepancy explains the phenomenon known as “senior inflation.” It is why an official Social Security update might boast a historically high increase, yet you still find yourself struggling to balance the checkbook by the end of the month. Acknowledging this reality allows you to anticipate shortfalls and build a more resilient budget.

The Ripple Effect on Medicare Premiums

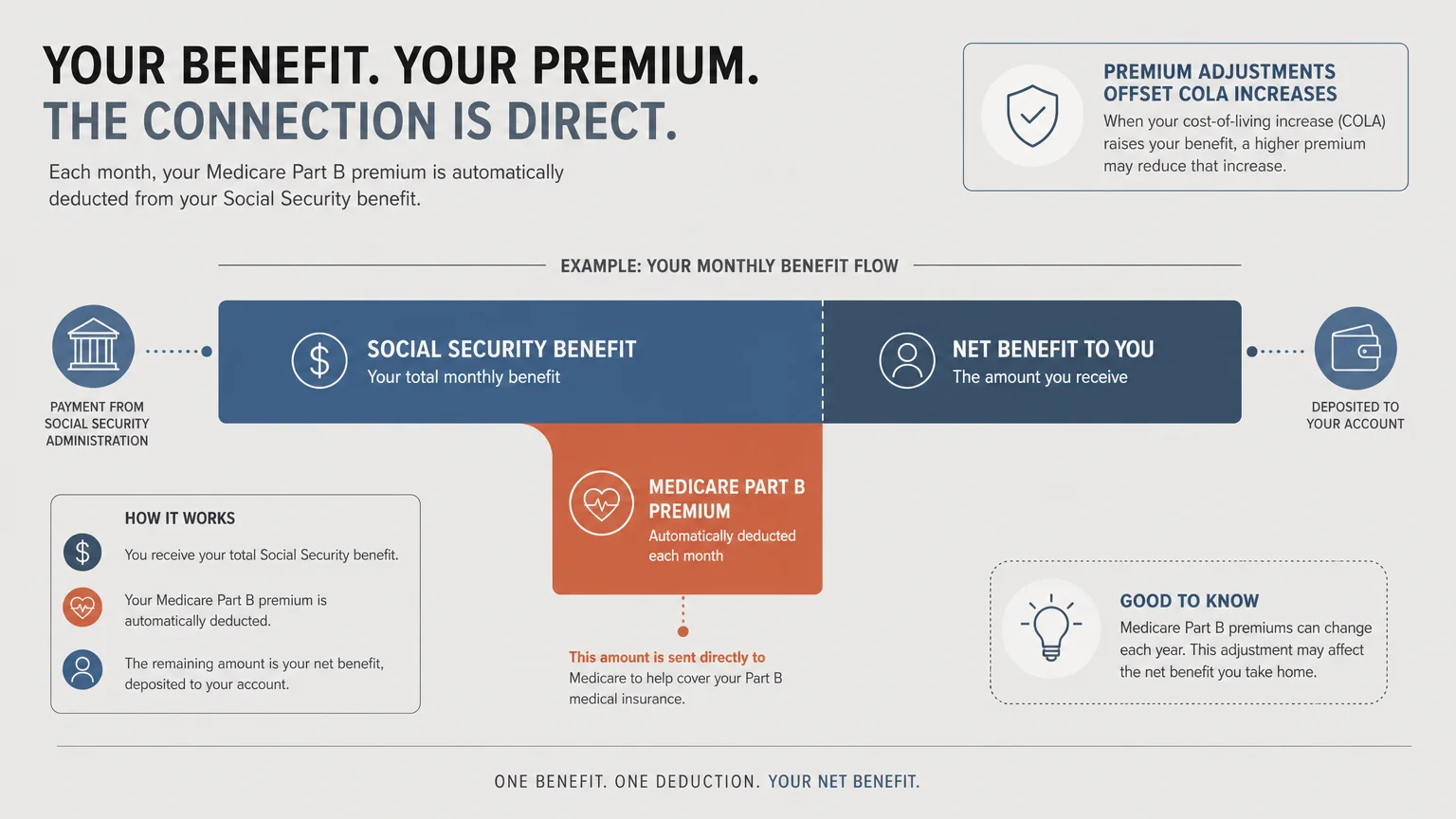

One of the most frustrating surprises for seniors occurs in January, right when the new COLA increase takes effect. You open your annual statement expecting a noticeable bump in your monthly deposit, only to find the actual cash increase is much smaller than the percentage announced on the evening news. The main culprit behind this shrinking check is usually Medicare.

For the vast majority of beneficiaries, standard Medicare Part B premiums are deducted directly from Social Security payments before the money ever reaches their bank account. When the government announces a cost of living increase for Social Security, they almost always announce premium hikes for Medicare Part B shortly afterward. Because healthcare costs consistently rise faster than general inflation, Medicare premiums tend to consume a disproportionate share of your annual adjustment.

Fortunately, federal law includes a protective measure known as the “hold harmless” provision. This rule guarantees that your standard Medicare Part B premium cannot increase by an amount that is larger than your COLA increase. In practical terms, this means your net Social Security check will never shrink from one year to the next due to standard Medicare premium hikes. If the Medicare premium goes up by twenty dollars, but your COLA only adds fifteen dollars to your check, the hold harmless provision caps your premium increase at fifteen dollars. You can find details on current premium rates through Medicare.gov, which outlines how your standard monthly premium might shift based on your income level.

While the hold harmless provision protects your current baseline income, it also means that in years with a low inflation adjustment, any extra money you were promised might immediately vanish to cover healthcare premiums. To navigate this, you should mentally separate your gross benefit from your net benefit. Treat your gross benefit as a calculation figure, but build your daily household budget strictly around your net deposit.

Calculating Your Personal Cost of Living

Because the national formula will never perfectly reflect your individual reality, you must take charge of tracking your personal cost of living. Creating a personalized inflation index empowers you to spot budget leaks early and adjust your spending habits before a minor shortfall turns into a significant financial crisis.

Do not let the idea of calculating an index intimidate you; you do not need an accounting degree to understand where your money is going. All you need is a willingness to review your financial statements and a systematic approach to tracking your expenses. Follow these specific steps to calculate how inflation impacts your unique household:

- Gather twelve months of statements: Pull your bank and credit card statements from January through December of the previous year. If you prefer physical copies, print them out; otherwise, utilize your bank’s digital tracking tools.

- Isolate your mandatory expenses: Highlight the bills you must pay to survive. This includes your mortgage or rent, property taxes, homeowners insurance, utilities, groceries, and medical expenses. Leave out discretionary spending like dining out or traveling for now.

- Compare year-over-year increases: Look at your mandatory expenses from January of last year compared to January of this year. Calculate the percentage difference. Did your grocery bill jump by ten percent? Did your property taxes rise by four percent?

- Factor in your COLA: Compare your personal expense increase against the official COLA rate for the current year. If your personal expenses rose by seven percent, but your benefit only increased by three percent, you have a four percent deficit that needs to be addressed through other income sources or budget cuts.

- Create an emergency buffer: Once you know your true cost of living, strive to build a liquid cash buffer equal to at least three months of these mandatory expenses. This buffer acts as your personal hold harmless provision against unexpected home repairs or medical emergencies.

By regularly auditing your expenses this way, you move away from generalized financial fear and step into active financial management. You will know exactly which bills are draining your resources and where you need to apply pressure—perhaps by negotiating a better rate on your car insurance or appealing a property tax assessment.

Common Pitfalls and Financial Scams to Avoid

As you navigate life on a fixed income, protecting the money you already have is just as important as maximizing your monthly benefits. Unfortunately, periods of economic uncertainty and the highly publicized announcement of the annual Social Security update create a breeding ground for opportunistic criminals. Scammers know that older Americans rely heavily on these adjustments, and they use this reliance to manufacture panic and steal personal information.

The Consumer Financial Protection Bureau (CFPB) warns that government impostor scams frequently spike around the time annual adjustments are announced. Criminals will call, email, or text seniors claiming to represent the Social Security Administration. The tactics vary, but the underlying message is always urgent and threatening. They might tell you that your Social Security number has been suspended due to fraudulent activity, or they might claim you must pay a processing fee to “unlock” or “activate” your new, higher benefit amount.

To safeguard your finances, keep these crucial truths in mind:

- The Social Security Administration will never call you out of the blue to threaten you with arrest or legal action.

- You never have to pay a fee, buy a gift card, or wire money to receive your annual cost of living adjustment. The process is completely automatic.

- Official communications regarding changes to your benefits will always arrive via formal physical mail or through your secure, verified online portal.

- Never click on links in unsolicited text messages claiming to offer a “bonus” cost of living check.

Another common pitfall involves aggressive investment salespeople who use the fear of inflation to push high-risk, illiquid financial products. While protecting your nest egg against inflation is a valid concern, you should be extremely wary of advisors selling complex annuities or speculative investments that lock up your money for decades with high surrender fees. Always demand a clear explanation of how the advisor gets paid, and seek a second opinion from a fiduciary—a professional legally bound to act in your best financial interest—before making major changes to your portfolio.

Smart Strategies to Stretch Your Fixed Income

When your personal cost of living outpaces your annual adjustment, you have to get creative. Relying solely on the government’s inflation adjustment is rarely a winning strategy for long-term comfort. Instead, you need proactive tactics to stretch your existing dollars further and reduce your outgoing cash flow.

One of the most effective strategies is actively auditing your recurring expenses. Many seniors pay for subscription services, premium cable channels, or landline phone services they rarely use. Take a hard look at your bank statements and ruthlessly cut any service that no longer brings you joy or essential utility. Redirect those reclaimed funds immediately into a high-yield savings account where they can earn a safe, respectable interest rate, putting your own money to work fighting inflation.

Another powerful tactic involves leveraging senior discounts and community resources. Never feel hesitant about asking for a senior discount at grocery stores, restaurants, or service providers; these discounts are specifically designed to help offset the pressures of living on a fixed income. Furthermore, many utility companies offer reduced rates or winterization grants for older adults. You can significantly lower your heating and cooling bills by requesting a free home energy audit from your local provider.

If housing costs represent your largest financial burden, you might need to consider larger lifestyle adjustments. Downsizing to a smaller, more energy-efficient home can drastically reduce your property taxes, utility bills, and maintenance costs. If moving is out of the question, explore local property tax relief programs. Many counties freeze property tax assessments for residents over a certain age or below a specific income threshold, but you usually have to apply for these programs proactively.

Finally, make sure you are utilizing all the federal and state assistance programs you qualify for. To discover local assistance programs that can offset these rising costs, you can explore Benefits.gov, a comprehensive tool for finding federal and state support tailored to your situation. Programs like the Supplemental Nutrition Assistance Program (SNAP) or the Medicare Savings Programs can free up hundreds of dollars in your monthly budget, providing a much larger financial cushion than a standard COLA increase ever could.

Frequently Asked Questions

When is the COLA increase announced each year?

The government typically announces the official adjustment for the upcoming year in mid-October. This timing aligns with the release of the Consumer Price Index data for September. Once announced, the Social Security Administration begins mailing official notices to beneficiaries in December, and you will see the new amount reflected in the check you receive in January.

Do I have to apply for my annual adjustment?

No, you do not have to fill out any paperwork, make any phone calls, or pay any fees to receive your annual adjustment. The process is completely automatic. If anyone contacts you claiming they need your personal information or a fee to process your increase, hang up the phone immediately—it is a scam.

Why did my monthly deposit decrease even though a COLA was announced?

If your actual bank deposit went down despite a positive inflation adjustment, the cause is usually related to changes in your Medicare Part B or Part D premiums, or an increase in your Medicare Income-Related Monthly Adjustment Amount (IRMAA). While the “hold harmless” provision protects most people from seeing a net decrease due to standard Part B premiums, it does not protect higher-income earners subject to IRMAA, nor does it cover increases in Part D prescription drug plan premiums.

If I claim my retirement benefits early at age 62, do I still get the annual adjustments?

Yes. Even if you choose to claim your benefits before your full retirement age, you are still fully eligible for every annual cost of living adjustment. In fact, the adjustments are applied to your primary insurance amount behind the scenes starting at age 62, even if you delay claiming your benefits until age 70. This ensures that the value of your base benefit keeps pace with inflation while you wait to claim.

Are Supplemental Security Income (SSI) recipients eligible for the same increase?

Yes, individuals who receive Supplemental Security Income (SSI) receive the exact same percentage increase as those receiving traditional retirement or disability benefits. The only difference is the payment schedule; the new, adjusted SSI payments typically begin on December 31st of the preceding year, while standard retirement benefit increases are paid in January.

For additional senior resources, visit

AARP, Alzheimer’s Association, American Heart Association, Benefits.gov and National Institute on Aging (NIA).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply