You rely on Social Security as the foundation of your retirement income, making any talk of changes from Washington naturally concerning. With the system’s trust funds facing a projected shortfall in the coming decade, Congress must eventually act to ensure it continues paying full benefits. Understanding these proposed reforms helps you prepare your personal finances for any future adjustments. Lawmakers are currently exploring various solutions, including raising the full retirement age, adjusting payroll taxes, and modifying benefit calculation formulas. Knowing these possibilities allows you to build a more resilient retirement strategy. This guide explains the realistic changes Congress might enact, separating political noise from factual policy proposals, so you can confidently secure your financial future.

Understanding the Social Security Trust Fund Shortfall

To understand why Congress might change Social Security, you first need to understand how the system funds your monthly payments. Social Security operates as a pay-as-you-go system. The payroll taxes collected from today’s workers immediately go toward paying the benefits of today’s retirees. For decades, the program collected more in taxes than it paid out in benefits, resulting in a surplus. The government placed this surplus into two specific trust funds: the Old-Age and Survivors Insurance (OASI) Trust Fund and the Disability Insurance (DI) Trust Fund.

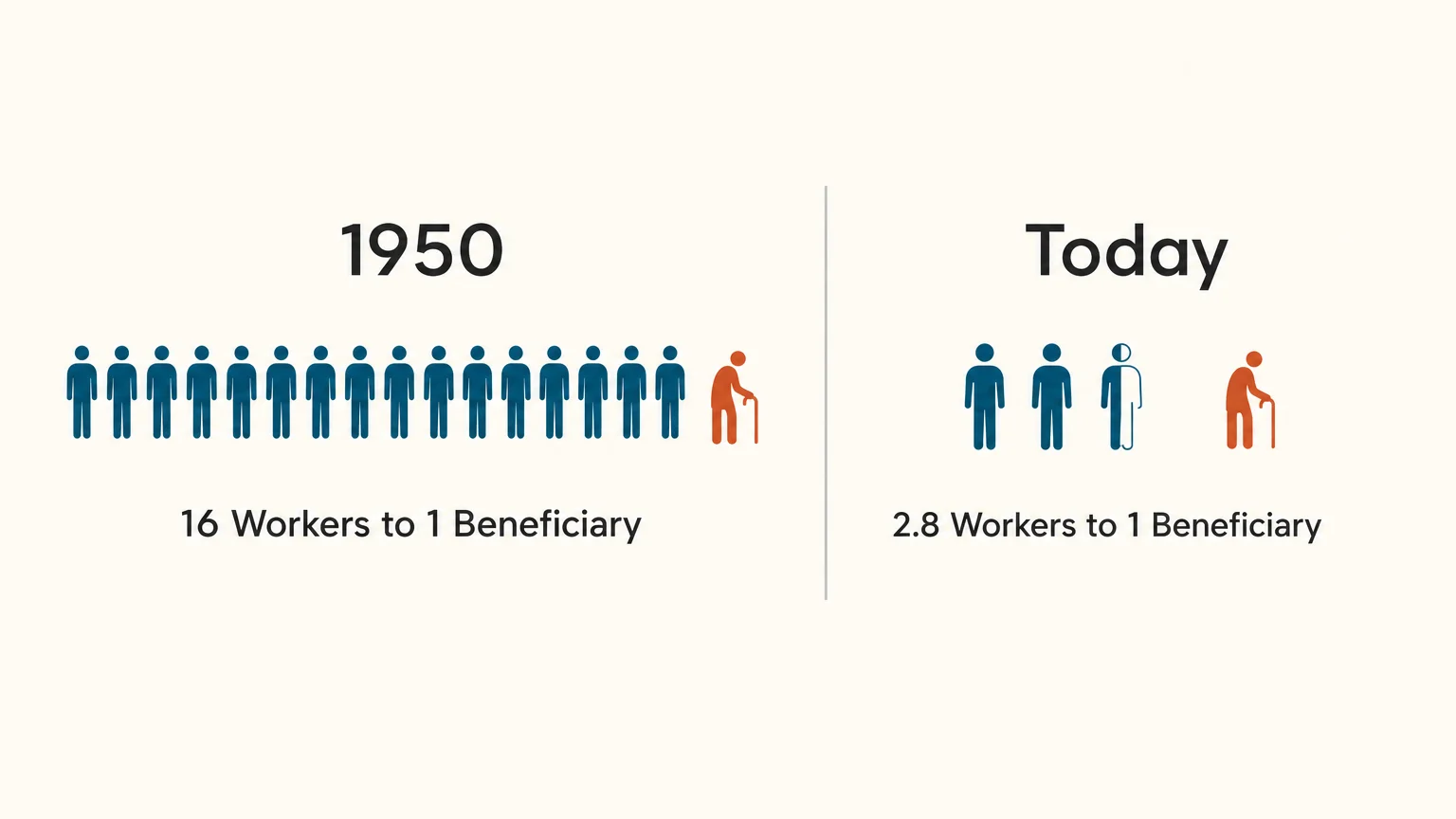

The core challenge today stems from shifting demographics. In 1950, approximately 16 workers paid into the system for every one person receiving benefits. Today, that ratio has dropped to roughly 2.8 workers per beneficiary, and it continues to shrink. People are living longer, healthier lives, while birth rates have steadily declined. Because of this imbalance, the system now pays out more than it brings in through payroll taxes alone, forcing it to draw from the accumulated trust fund reserves to make up the difference.

According to projections from the Social Security Administration (SSA), the reserve funds face depletion at some point in the mid-2030s. Depletion does not mean Social Security goes bankrupt or disappears. Even if the trust funds reach zero, ongoing payroll taxes will still cover approximately 80 percent of promised benefits. However, an automatic 20 percent reduction in benefits would be catastrophic for millions of seniors on fixed incomes. Congress holds the power to prevent this shortfall, and lawmakers have successfully enacted major reforms in the past to keep the program solvent.

Potential Changes to Retirement Age Requirements

One of the most frequently discussed proposals for reforming Social Security involves raising the full retirement age (FRA). Your FRA dictates when you can claim 100 percent of your earned monthly benefit. Congress previously raised the retirement age in 1983. Back then, they passed legislation to gradually increase the FRA from 65 to 67 for anyone born in 1960 or later. Because people enjoy longer lifespans today than they did in the 1980s, many lawmakers argue that the retirement age should increase again to reflect this reality.

Current proposals suggest pushing the FRA from 67 to 68, 69, or even 70 over several decades. While proponents argue this change aligns with modern life expectancies and encourages older Americans to remain in the workforce, opponents point out that a higher retirement age acts as a mathematical benefit cut for those who cannot physically continue working. If Congress raises the FRA to 69, claiming benefits at the earliest eligible age of 62 would result in a much steeper permanent reduction to your monthly check than the current penalty.

Consider the following impacts of raising the retirement age:

- Heavier penalties for early claimers: Currently, claiming at 62 with an FRA of 67 reduces your benefit by 30 percent. If the FRA moves to 69, claiming at 62 could reduce your starting benefit by 40 percent.

- Delayed maximum benefits: You currently earn 8 percent delayed retirement credits every year you wait past your FRA up to age 70. A higher FRA narrows the window you have to earn these lucrative credits.

- Disproportionate physical impact: Seniors working in physically demanding jobs—such as construction, nursing, or manufacturing—often face significant health hurdles that prevent them from delaying retirement, making an age increase particularly burdensome for blue-collar workers.

Adjustments to Payroll Taxes and Income Caps

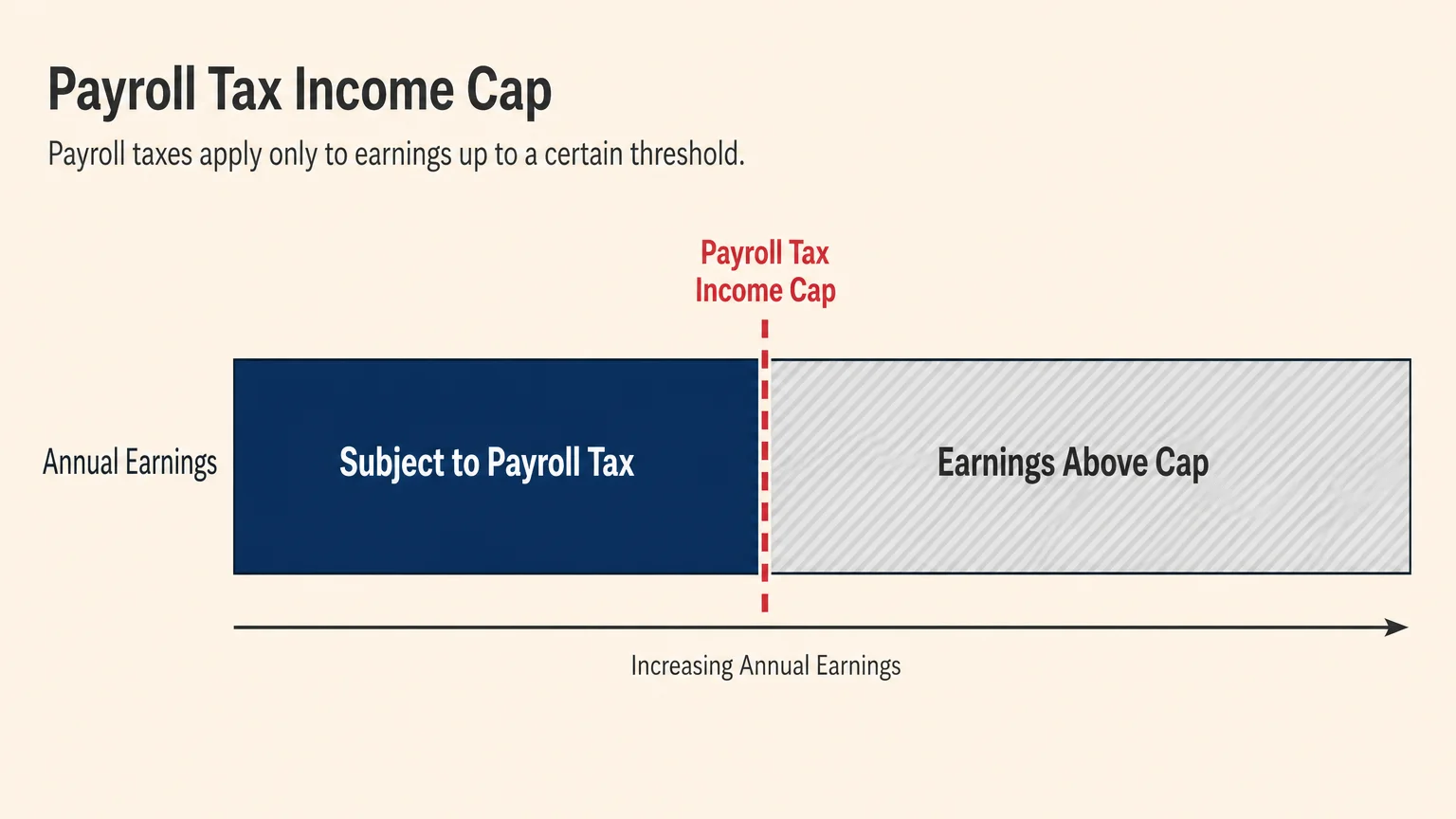

Rather than cutting benefits or forcing seniors to wait longer for their money, another path Congress might take involves increasing the revenue flowing into the system. The Federal Insurance Contributions Act (FICA) requires workers and employers to split a 12.4 percent tax on earnings. However, this tax does not apply to all income. Congress sets a specific wage cap every year; earnings above this threshold remain exempt from Social Security taxes.

Many policy experts advocate for adjusting this cap or raising the tax rate to shore up the trust funds. By generating more revenue from higher-earning individuals, the government can close the funding gap without altering the payouts for current or future retirees.

Lawmakers typically debate three distinct revenue-boosting strategies:

| Proposed Tax Strategy | How It Works | Potential Impact on the System |

|---|---|---|

| Eliminating the Wage Cap | Subjects all earned income, regardless of how high, to the 12.4% payroll tax. | Would eliminate a massive portion of the projected shortfall almost immediately, heavily impacting high-income earners. |

| Creating a “Donut Hole” | Keeps the current cap, exempts earnings up to a certain point (e.g., $400,000), then reapplies the tax on all earnings above that threshold. | Protects middle-class and upper-middle-class workers while ensuring the highest earners contribute more to the system. |

| Raising the Overall Tax Rate | Gradually increases the FICA tax rate from 12.4% to a higher figure, such as 14%, split evenly between employer and employee. | Spreads the burden across the entire working population, taking a slightly larger bite out of every worker’s paycheck. |

Modifying Benefit Calculations and Cost of Living Adjustments

Beyond changing ages and taxes, Congress could alter the internal math the Social Security Administration uses to calculate your starting benefit and your annual raises. These structural changes often fly under the radar because they involve complex formulas, but their impact on your wallet is significant.

One major proposal involves changing how the annual Cost of Living Adjustment (COLA) is calculated. Currently, COLA relies on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Some lawmakers propose switching to the “Chained CPI.” The Chained CPI assumes that when the price of one good rises, consumers will substitute it for a cheaper alternative—for instance, buying chicken when the price of beef skyrockets. Because it accounts for substitution, the Chained CPI generally grows at a slower rate than the standard CPI-W. Over a 20-year retirement, switching to the Chained CPI would result in noticeably lower cumulative benefit increases, slowly reducing your purchasing power over time.

Conversely, advocacy groups for seniors often push Congress to adopt the Consumer Price Index for the Elderly (CPI-E). The CPI-E heavily weighs the specific expenses older Americans face, primarily healthcare and housing costs, which typically rise faster than general inflation. Adopting the CPI-E would likely result in higher annual COLAs, though it would also drain the trust funds faster.

Another structural change involves means-testing. Means-testing would reduce or eliminate Social Security benefits for wealthy retirees who earn above a certain income threshold. Proponents argue that millionaires do not need a government safety net, and those funds should be preserved for seniors who rely entirely on their monthly checks. Opponents argue that means-testing transforms Social Security from an earned entitlement into a welfare program, potentially eroding widespread public support for the system.

Common Misconceptions About Social Security Reform

Whenever politicians debate Social Security, misinformation spreads quickly. Fear-inducing headlines can lead you to make panic-driven financial decisions. By understanding the realities of federal policy, you can plan your retirement with a clear, rational mindset.

Misconception: The government stole the Social Security money.

You will often hear that Congress raided the trust funds and replaced the cash with worthless IOUs. This is fundamentally untrue. By law, the Social Security Administration must invest all surplus funds into special-issue U.S. Treasury bonds. These bonds pay a guaranteed interest rate and are backed by the full faith and credit of the United States government. This is the exact same mechanism global banks and foreign nations use to store their wealth securely. The trust funds hold trillions of dollars in real, interest-bearing government debt.

Misconception: Current retirees will face immediate, severe benefit cuts.

Historically, when Congress enacts major retirement legislation, they create long phase-in periods. The 1983 reforms took nearly four decades to fully implement. Lawmakers face immense political pressure to protect seniors already receiving benefits or those nearing retirement age. Any changes to the full retirement age or benefit formulas will almost certainly target younger workers who have decades to adjust their savings strategies.

Misconception: Social Security is going bankrupt and will cease to exist.

As long as Americans continue working and paying payroll taxes, Social Security will continue issuing checks. The looming crisis is a funding gap, not a total collapse. The worst-case scenario—total legislative inaction—results in reduced payments, not zero payments.

Actionable Strategies to Protect Your Retirement Income

While you cannot control what Congress does, you can control your personal financial habits. Building a robust, diversified retirement plan ensures you can weather any potential policy shifts from Washington. Taking proactive steps today reduces your reliance on federal programs tomorrow.

First, aggressively manage and eliminate your debts. Entering retirement with a mortgage, car loan, or high-interest credit card debt requires a massive amount of fixed monthly income. According to the Consumer Financial Protection Bureau (CFPB), carrying debt into your senior years severely restricts your financial flexibility and limits your ability to absorb economic shocks. By paying down debt while you are still working, you lower your baseline living expenses, making it easier to survive on a slightly reduced Social Security benefit if necessary.

Next, focus on maximizing your personal savings. Contribute as much as possible to your 401(k), IRA, or health savings account (HSA). If you are over 50, take advantage of IRS catch-up contributions to rapidly inflate your portfolio balances. You should also explore reliable guidance from senior advocacy organizations. AARP provides excellent tools and calculators to help you estimate your future income needs and build a savings strategy that complements your projected government benefits.

Finally, consider your timeline for claiming benefits. If your health and employment situation allow, delaying your Social Security application past your full retirement age guarantees an 8 percent annual increase in your permanent payout up to age 70. This elevated baseline provides a powerful hedge against future inflation and potential legislative tweaks to the COLA formula.

Frequently Asked Questions

Will my current benefits be reduced if Congress changes the rules?

It is highly unlikely. Historically, Congress grandfathers in current beneficiaries and those nearing retirement age when making structural changes to Social Security. Politicians rely heavily on the senior voting bloc, making immediate cuts to existing retirees political suicide. Reforms like raising the retirement age generally target workers currently in their 30s and 40s.

When will Congress likely pass new Social Security legislation?

Lawmakers tend to delay difficult decisions until a deadline forces their hand. Because the trust funds are not projected to reach depletion until the early to mid-2030s, Congress may wait until we are much closer to that date to pass comprehensive reform. However, waiting increases the severity of the changes needed to fix the math.

Should I claim my benefits early just to lock them in before Congress acts?

Financial experts strongly caution against claiming early out of fear. Claiming at age 62 locks you into a permanent, significant reduction in your monthly income for the rest of your life. Because any future Congressional cuts would likely exempt those nearing retirement anyway, claiming early guarantees a lower income out of fear of a hypothetical future reduction.

How would raising the retirement age affect me if I am already 65?

If you are currently 65, any new legislation raising the retirement age will almost certainly not affect you. Your full retirement age is already locked in based on your birth year. The proposed changes to push the FRA to 68 or 70 are designed to phase in gradually for younger generations who have decades left in the workforce.

Can I find alternative financial assistance if Social Security does not cover my expenses?

Yes. If your current benefits leave you struggling to meet basic needs, you may qualify for state and federal assistance programs designed specifically for older adults. You can explore a comprehensive directory of housing, healthcare, and utility assistance programs by visiting Benefits.gov to determine what supplemental support you are eligible to receive.

For additional senior resources, visit

Administration for Community Living (ACL),

Eldercare Locator and

AARP.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply