Skyrocketing rent, soaring property taxes, and rising utility bills push many older adults to the financial breaking point, yet billions in government housing assistance go unclaimed every year. You do not have to drain your life savings to keep a safe roof over your head. Unlocking these financial lifelines begins with knowing where to look and understanding the strict eligibility rules. Whether you need urgent home repairs, a subsidized apartment, or monthly help covering your heating costs, local and federal grants exist specifically to protect your independence. Here are ten overlooked senior housing assistance programs that can dramatically lower your living expenses, along with the exact steps you must take to secure your benefits today.

Section 202 Supportive Housing for the Elderly

The Department of Housing and Urban Development (HUD) funds a specialized program designed strictly for seniors called Section 202 Supportive Housing for the Elderly. Unlike generic low-income apartments, these complexes are built exclusively for older adults and provide on-site service coordinators. These professionals act as advocates, helping you secure additional benefits, coordinate transportation to medical appointments, and arrange meal deliveries right to your door.

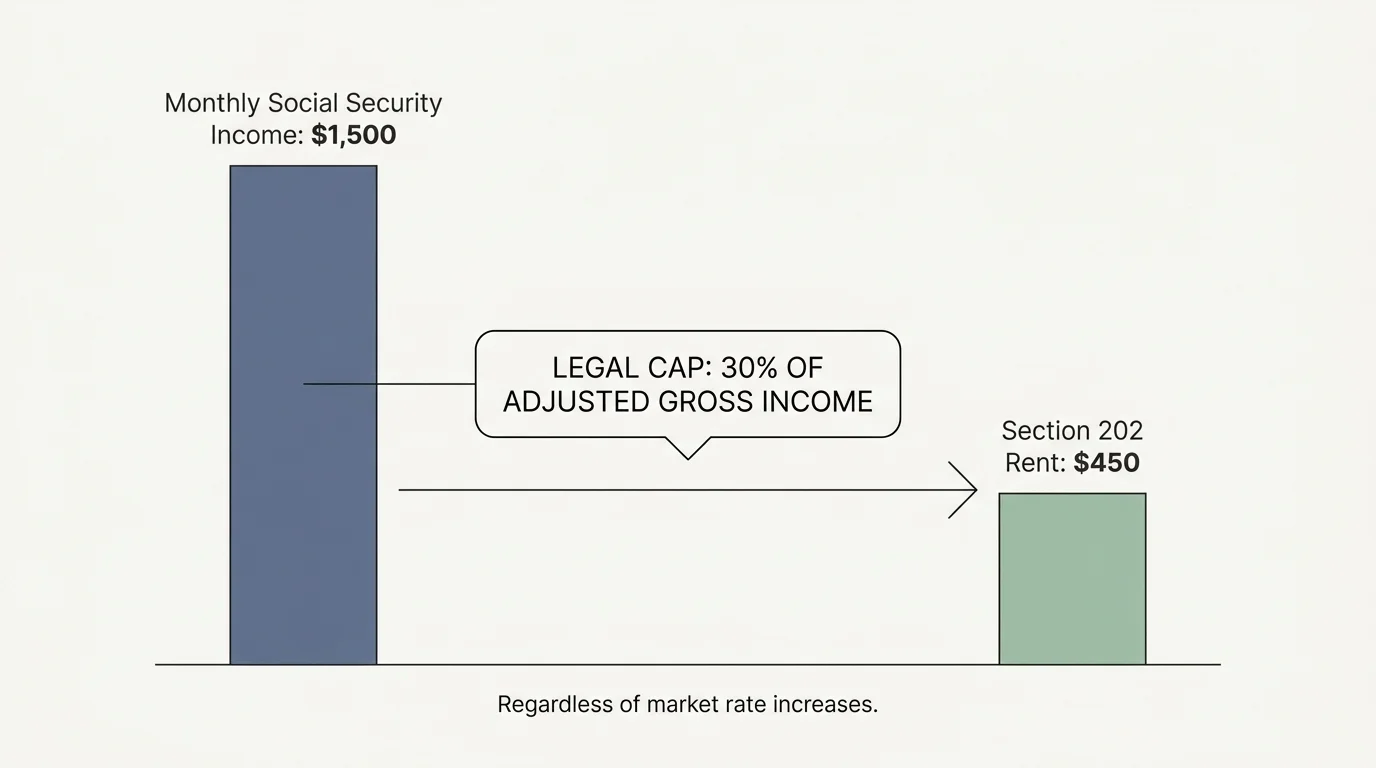

The financial structure of Section 202 housing offers incredible protection against inflation. Your rent is legally capped at 30% of your adjusted gross income. If your only income is a monthly Social Security check of $1,500, your rent will never exceed $450 per month—regardless of how high market rates climb in your city.

To qualify, you must meet the following criteria:

- At least one member of your household must be 62 years of age or older.

- Your household income must fall below 50% of the median income for your area.

- You must be able to live independently, though you can use in-home care services.

Because these communities offer such high value, waiting lists can be long. You should apply to multiple Section 202 properties simultaneously. You must contact the management offices of individual properties to request an application, rather than applying through a centralized government office.

HUD Housing Choice Vouchers (Section 8)

The Housing Choice Voucher program, commonly referred to as Section 8, is the federal government’s primary program for assisting very low-income families and the elderly to afford decent, safe housing in the private market. Instead of forcing you to move into a designated public housing complex, this program allows you to find your own apartment, townhome, or single-family residence, provided the landlord agrees to accept the voucher.

Once approved, your local Public Housing Agency (PHA) pays the housing subsidy directly to your landlord on your behalf. You are then responsible for paying the difference between the actual rent charged and the subsidized amount. Like Section 202 housing, your portion of the rent and utilities is generally capped at 30% of your adjusted monthly income.

Here is a simplified example of how a Housing Choice Voucher dramatically changes a senior’s monthly budget:

| Expense Category | Without Housing Voucher | With Housing Voucher |

|---|---|---|

| Monthly Fixed Income | $1,800 | $1,800 |

| Total Monthly Rent | $1,200 | $1,200 |

| Senior’s Rent Payment (30% of income) | $1,200 | $540 |

| Government Subsidy Payment | $0 | $660 |

| Income Remaining for Food, Meds, etc. | $600 | $1,260 |

You must apply through your local PHA. Many local agencies offer preference points to older adults, moving you higher up the waiting list ahead of younger, able-bodied applicants.

USDA Section 504 Home Repair Program

If you own your home but struggle to afford urgent repairs, you may be living with dangerous safety hazards simply because you lack the cash to fix them. The United States Department of Agriculture (USDA) offers the Section 504 Home Repair Program specifically to help low-income rural residents maintain their properties.

The definition of “rural” is incredibly broad; many suburban neighborhoods on the outskirts of major cities qualify for USDA assistance. This program offers two distinct types of financial help:

- Grants up to $10,000: Available exclusively to homeowners aged 62 and older. This money never has to be repaid, provided you do not sell the property for three years. It must be used to remove health and safety hazards, such as replacing a collapsing roof, installing a wheelchair ramp, or upgrading a dangerous electrical system.

- Loans up to $40,000: Available to very-low-income homeowners of any age. The interest rate is fixed at an unbeatable 1% for 20 years, making the monthly payments exceptionally affordable.

You can even combine a grant and a loan for up to $50,000 in total assistance. To apply, you must contact your local USDA Rural Development office and provide proof of homeownership, income statements, and quotes from licensed contractors.

Low Income Home Energy Assistance Program (LIHEAP)

Heating and cooling costs are a massive burden for seniors on fixed incomes. The Low Income Home Energy Assistance Program (LIHEAP) provides federally funded, state-administered grants to help you cover these exact expenses. According to Benefits.gov, this program is designed to keep families safe and healthy by managing costs associated with home energy bills, energy crises, and minor energy-related home repairs.

LIHEAP funds do not go directly into your bank account. Instead, the administering agency sends the money straight to your utility provider, resulting in a credit on your monthly bill. The program provides two main types of help:

- Standard Assistance: A one-time annual grant applied to your main heating or cooling source.

- Crisis Assistance: Emergency funds dispersed rapidly if you receive a shut-off notice or are completely out of heating fuel during the winter.

Because LIHEAP is a block grant, funding is finite. Once a state spends its annual allocation, no more grants are issued until the next fiscal year. You should submit your application the very first week the program opens in your state—typically in October or November.

Weatherization Assistance Program (WAP)

While LIHEAP helps pay your utility bills, the Weatherization Assistance Program (WAP) permanently reduces your energy consumption by upgrading your home for free. Administered by the Department of Energy, WAP provides comprehensive home energy efficiency updates to low-income households.

When you are approved for WAP, a professional energy auditor will come to your home to conduct a thorough inspection. They will use specialized equipment to find air leaks, test the efficiency of your furnace, and check your insulation levels. Based on their findings, licensed contractors will arrive to perform the necessary upgrades at zero cost to you.

Common free upgrades include:

- Blowing heavy insulation into your attic and exterior walls.

- Repairing or entirely replacing an aging, inefficient furnace or central air conditioning unit.

- Installing heavy-duty weatherstripping around doors and windows.

- Upgrading an old water heater.

By drastically reducing the amount of energy required to heat and cool your home, you lock in permanent monthly savings. Older adults are placed on a priority waiting list for this program, meaning your application will be processed faster than general inquiries.

Medicaid Home and Community-Based Services (HCBS)

Many seniors are forced out of their homes and into nursing facilities simply because they can no longer perform basic daily tasks like bathing, cooking, or safely moving around the house. Medicare provides excellent medical insurance, but as noted by Medicare.gov, standard Medicare does not cover the cost of long-term custodial care.

This is where Medicaid steps in. Medicaid offers Home and Community-Based Services (HCBS) waivers designed specifically to keep you out of a nursing home. If you qualify medically and financially, the state will pay for supportive services delivered right to your front door.

HCBS waivers can pay for:

- A home health aide to visit daily to help you dress, bathe, and manage medications.

- Major home modifications, such as widening doorways for a wheelchair or installing a walk-in shower.

- Adult day care programs that provide meals and supervision while family caregivers are at work.

Every state has different names and income limits for their waiver programs. You must apply through your state’s Medicaid office and undergo a functional assessment by a nurse to prove you require a “nursing home level of care” but can be kept safe at home with assistance.

Veterans Aid and Attendance Benefit

If you or your late spouse served during a period of wartime, you may be entitled to a massive, tax-free monthly payout that most veterans never know exists. The Veterans Aid and Attendance (A&A) benefit is an enhanced pension added to your regular VA pension if you require the aid of another person to perform basic activities of daily living.

This is not a housing program in the traditional sense, but it is one of the most powerful ways to afford housing and care in your later years. The funds can be used to pay for in-home caregivers, adult day care, or the monthly rent at an assisted living facility. For a married veteran in 2024, the maximum A&A benefit can exceed $2,700 per month. A surviving spouse can receive over $1,400 per month.

To qualify, you must meet strict financial asset limits and prove that you require assistance with daily tasks such as bathing, dressing, or eating. Alternatively, you qualify automatically if you are bedridden, reside in a nursing home due to mental or physical incapacity, or have severe visual impairment.

State Property Tax Relief Programs

For seniors who have paid off their mortgages, property taxes remain the single biggest threat to their financial stability. As home values skyrocket, municipal tax assessments follow, leaving seniors with tax bills they simply cannot pay. Fortunately, almost every state offers specialized property tax relief programs for older adults.

These programs generally fall into three categories:

- Property Tax Freezes: Once you reach a certain age (usually 65) and fall below an income threshold, your home’s assessed value is locked in. Even if your home triples in value over the next decade, your tax bill remains based on the frozen assessment.

- Homestead Exemptions: A set dollar amount or percentage is deducted from your home’s assessed value before taxes are calculated. If your home is assessed at $200,000 and your senior exemption is $50,000, you only pay taxes on $150,000.

- Circuit Breakers: These state income tax credits act like an electrical circuit breaker, kicking in when your property tax burden exceeds a certain percentage of your annual income. The state will refund you the excess amount when you file your state taxes.

Property tax relief is never automatic. You must go to your local county tax assessor’s office and physically file the exemption paperwork, providing your birth certificate and previous year’s tax return as proof of eligibility.

Area Agencies on Aging Housing Grants

Navigating the maze of local, state, and federal bureaucracy is exhausting. You have a powerful local ally designed specifically to handle this legwork. Your local Area Agency on Aging (AAA) receives federal funding through the Older Americans Act to help seniors age in place safely.

AAAs do not just provide information; they manage localized pools of grant money that you will not find advertised on the internet. These unadvertised funds can pay for emergency chore services, heavy house cleaning to prevent eviction, or minor home repairs like fixing broken steps or installing grab bars. The Eldercare Locator can connect you directly with your local Area Agency on Aging by simply entering your zip code.

When you call your local AAA, ask for an “options counselor.” This professional will conduct a free, comprehensive review of your financial situation and instantly match you with every municipal housing grant, food pantry, and utility assistance program active in your specific county.

Community Action Residential Repair Programs

Community Action Agencies (CAAs) are local non-profit organizations funded by the federal Community Services Block Grant. These agencies operate entirely on a local level, meaning the specific housing help they offer varies wildly from county to county. However, they are often the fastest source of emergency housing assistance available.

If you are facing immediate eviction, a CAA can often step in with emergency rental assistance to pay your arrears. If your water heater bursts in the middle of winter, a CAA may have an emergency repair fund to dispatch a plumber the same day.

When seeking home repairs through local non-profits or independent contractors, you must remain incredibly vigilant against fraud. Scammers routinely target older homeowners by pulling public tax records to see who has lived in their home the longest. Data from Consumer Financial Protection Bureau (CFPB) warns that you should never sign over your home’s deed, never pay a contractor entirely in cash upfront, and always verify that any individual offering free government repairs is legitimately connected to an approved agency.

Frequently Asked Questions

Do government housing grants count as taxable income?

In almost all cases, no. According to IRS.gov, payments made under a legislatively provided social benefit program for the promotion of general welfare are generally not considered gross income. This means grants for home repairs, utility assistance from LIHEAP, or subsidized rent through Section 8 will not increase your tax liability or push your Social Security benefits into a taxable bracket. Always keep the award letters for your records just in case your tax preparer needs to verify the source of the funds.

How long are the waiting lists for senior housing programs?

Waiting times vary drastically depending on your geographic location and the specific program. Section 8 housing vouchers often have waiting lists spanning two to five years, and some cities periodically close their lists to new applicants. Conversely, emergency programs like LIHEAP crisis grants or Community Action Agency emergency rental assistance can be approved and dispersed in a matter of days. Because of the long wait times for long-term housing, you should apply for multiple waiting lists across several neighboring counties immediately, rather than waiting until you are in a financial crisis.

Can I apply for multiple housing assistance programs at the same time?

Yes, and you absolutely should. The government encourages “stacking” these benefits to ensure a stable living environment. For example, you can legally live in an affordable Section 202 apartment, use LIHEAP to pay your winter heating bill, and have a Medicaid HCBS waiver pay for a home health aide to assist you with bathing. However, you must accurately report all your assistance during annual income recertification, as one benefit might slightly alter the calculation of another.

Will accepting a home repair grant put a lien on my house?

It depends entirely on the program’s specific rules. The USDA Section 504 grant does not place a lien on your home, but it does require you to repay the grant if you sell the house within three years of receiving the funds. Local municipal grants sometimes place a “forgivable lien” on the property, meaning the lien decreases by 20% every year you live in the home until it vanishes completely. You must read the fine print and ask the program administrator explicitly if a lien or repayment clause is attached to the funds.

For official financial guidance for seniors, visit

National Institute on Aging (NIA), Administration for Community Living (ACL) and Eldercare Locator.

Disclaimer: This article is for informational purposes and is not a substitute for professional financial or tax advice. Consult with a certified financial planner or tax professional for guidance on your specific situation.

Leave a Reply