Navigating retirement involves a constant stream of mail, from health coverage updates to tax documents. Sorting through this pile can feel overwhelming, but tossing the wrong piece of paper might cost you thousands of dollars or delay critical benefits. Certain government forms serve as your golden tickets to secure housing, prove your medical coverage, minimize your tax burden, and access earned military benefits. By knowing exactly which official documents demand a permanent place in your filing cabinet, you protect your fixed income and spare your family unnecessary administrative headaches during emergencies. Here are the nine crucial government forms you must never throw away and exactly why they belong in your permanent records.

1. Form SSA-1099: Social Security Benefit Statement

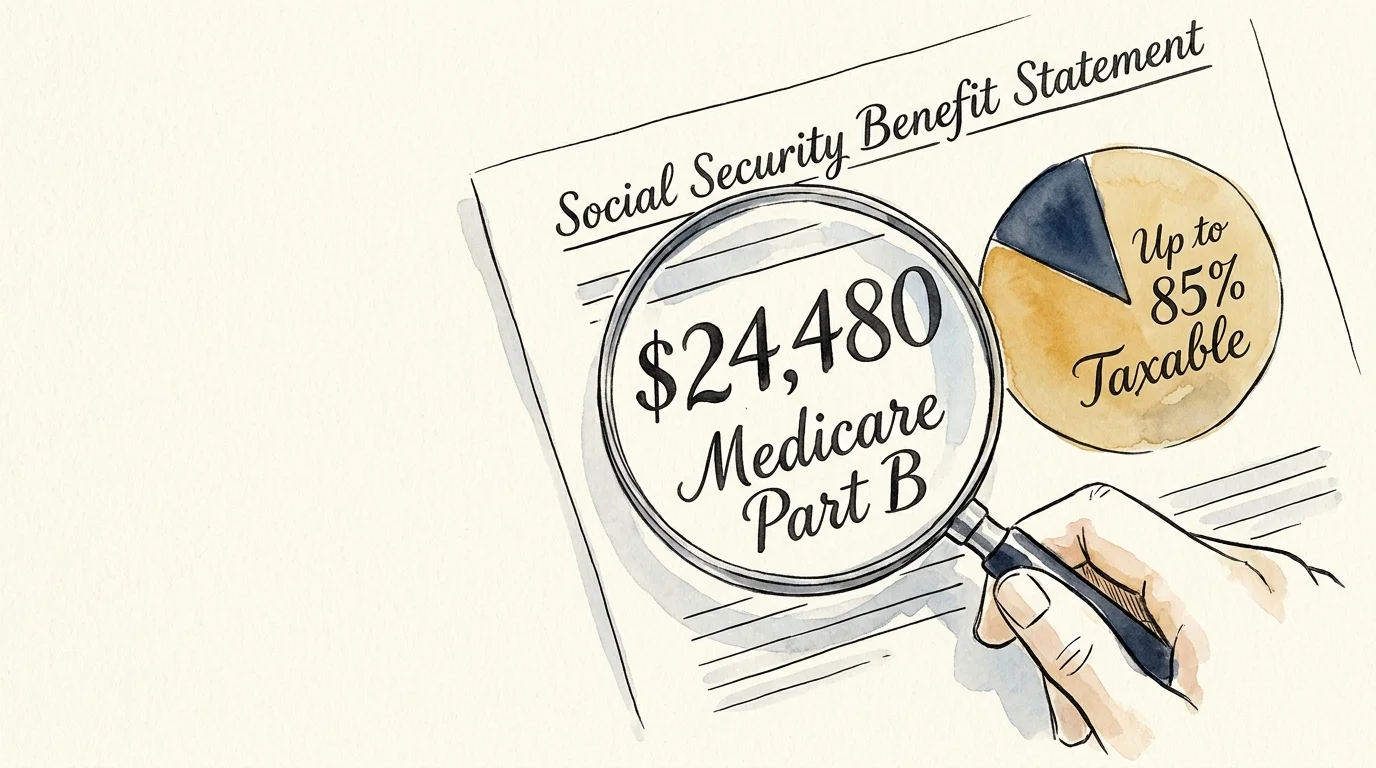

Every January, you receive Form SSA-1099 in the mail. This document details exactly how much money you received in Social Security benefits during the previous calendar year. It also shows how much money was deducted for Medicare Part B premiums before your monthly deposit hit your bank account. You must retain this document for several critical reasons.

First and foremost, you need Form SSA-1099 to file your federal income taxes. Depending on your total combined income, up to 85% of your Social Security benefits may be taxable. Without this form, calculating your tax liability becomes a guessing game that could trigger an audit or result in overpayment. According to the Social Security Administration (SSA), you can easily request a replacement form online through your personal account, but having the physical copy on hand saves you the hassle during the busy tax season.

Beyond taxes, this form acts as an official proof of income. If you apply for subsidized senior housing, energy assistance programs, or supplemental nutrition programs, administrators will demand verified proof of your annual earnings. Your SSA-1099 provides undeniable evidence of your fixed income status.

2. Medicare Summary Notice (MSN)

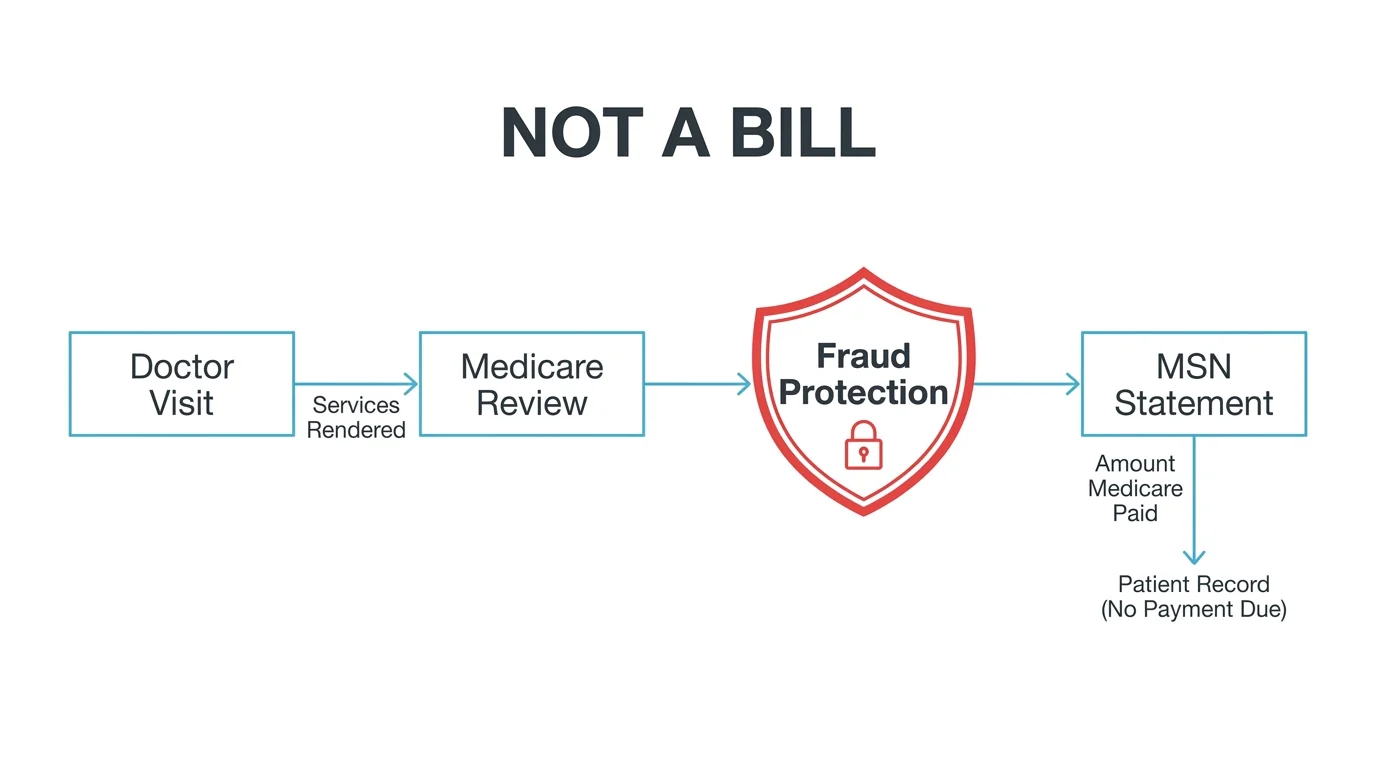

The Medicare Summary Notice frequently confuses people because it closely resembles a medical bill. It is not a bill. Rather, it is a comprehensive statement mailed to you every three months—provided you used Medicare services during that period. It lists all the healthcare services, medical supplies, and equipment billed to Medicare on your behalf.

Retaining your MSNs serves as your primary defense against medical billing errors and healthcare fraud. Fraudsters sometimes steal Medicare numbers to bill the government for wheelchairs, braces, or tests you never received. By reviewing your MSN, you can spot these fake charges immediately and report them.

| Feature | Medicare Summary Notice (MSN) | Standard Medical Bill |

|---|---|---|

| Sender | Federal Government (Medicare) | Your Doctor or Hospital |

| Frequency | Every 3 months (if services were used) | Shortly after your appointment |

| Action Required | Review for accuracy and fraud | Pay the remaining balance owed |

| What it Shows | What Medicare paid, what was denied, and maximum you can be billed | The specific amount you owe the provider |

According to Medicare.gov, you should compare your MSNs against the bills you receive from your doctors to ensure you are not overpaying. If a provider charges you more than the “Maximum You May Be Billed” amount listed on your MSN, you have physical proof to dispute the charge.

3. Social Security Award Letter

Your Social Security Award Letter—sometimes called a Notice of Award—is the original document you received when your application for retirement, disability, or survivor benefits was approved. This letter outlines your initial benefit amount, your date of entitlement, and the specific rules regarding your ongoing payments.

Unlike the annual SSA-1099 or the yearly Cost-of-Living Adjustment (COLA) notices, the original Award Letter establishes the foundation of your benefits. It remains the ultimate verification document for mortgage lenders, auto loan providers, and landlords. While a bank statement shows a direct deposit, the Award Letter proves to financial institutions that this income is permanent and guaranteed.

Store this document in your permanent files. If you ever need to transition into an assisted living facility or apply for Medicaid to cover long-term care, caseworkers will trace your income history back to this original determination.

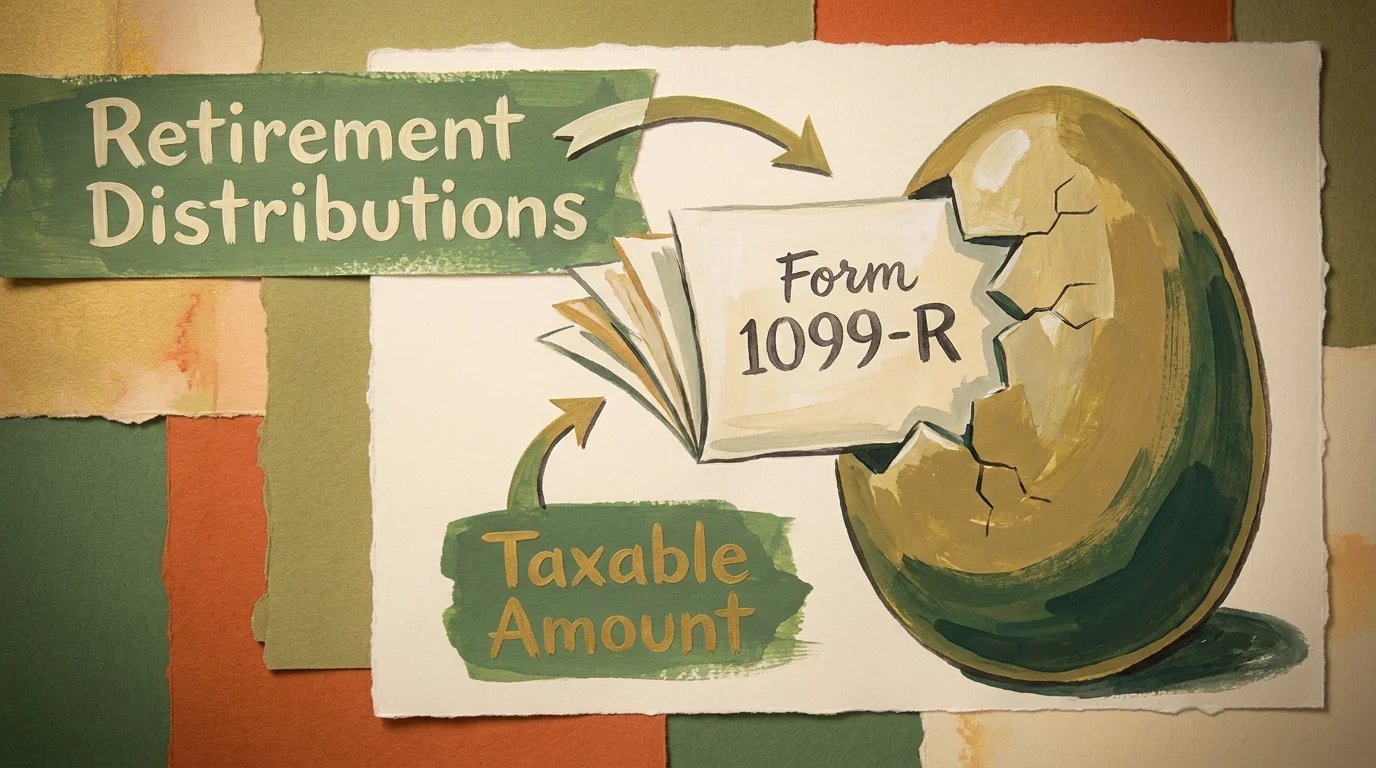

4. IRS Form 1099-R: Retirement Distributions

Whenever you take money out of a pension, 401(k), IRA, or an annuity, the financial institution managing that account generates an IRS Form 1099-R. This form dictates how the IRS views your retirement income. Not all withdrawals are taxed equally; some are fully taxable, some are partially taxable, and others are tax-free.

You must keep every Form 1099-R you receive. These forms contain specific distribution codes that tell the IRS exactly what kind of withdrawal you made. For example, if you roll money directly from a 401(k) into an IRA, the transaction is not taxable. However, the IRS still requires a 1099-R to prove that a legal rollover occurred rather than an early, taxable cash withdrawal.

Furthermore, as you age, managing Required Minimum Distributions (RMDs) becomes a legal necessity. Your 1099-R forms prove that you have met your annual RMD obligations, shielding you from severe IRS penalty taxes that apply when you fail to withdraw the correct amount.

5. DD Form 214: Military Discharge Papers

For veterans, the DD Form 214 (Certificate of Release or Discharge from Active Duty) is arguably the most valuable single piece of paper you own. It verifies your military service dates, your final rank, your specialized training, and most importantly, the character of your discharge (e.g., Honorable).

You should never discard this form because nearly all federal and state veteran benefits require it as proof of service. Without a DD Form 214, you cannot access VA healthcare, apply for a VA-backed mortgage, or claim veteran-specific property tax exemptions in your home state.

This document is also crucial for your surviving spouse and family. A DD Form 214 is required to arrange burial in a VA national cemetery, request a military headstone, or secure burial allowances. Replacing a lost DD Form 214 through the National Archives can take weeks or months; having the original safely stored ensures your family can access benefits immediately during a stressful time.

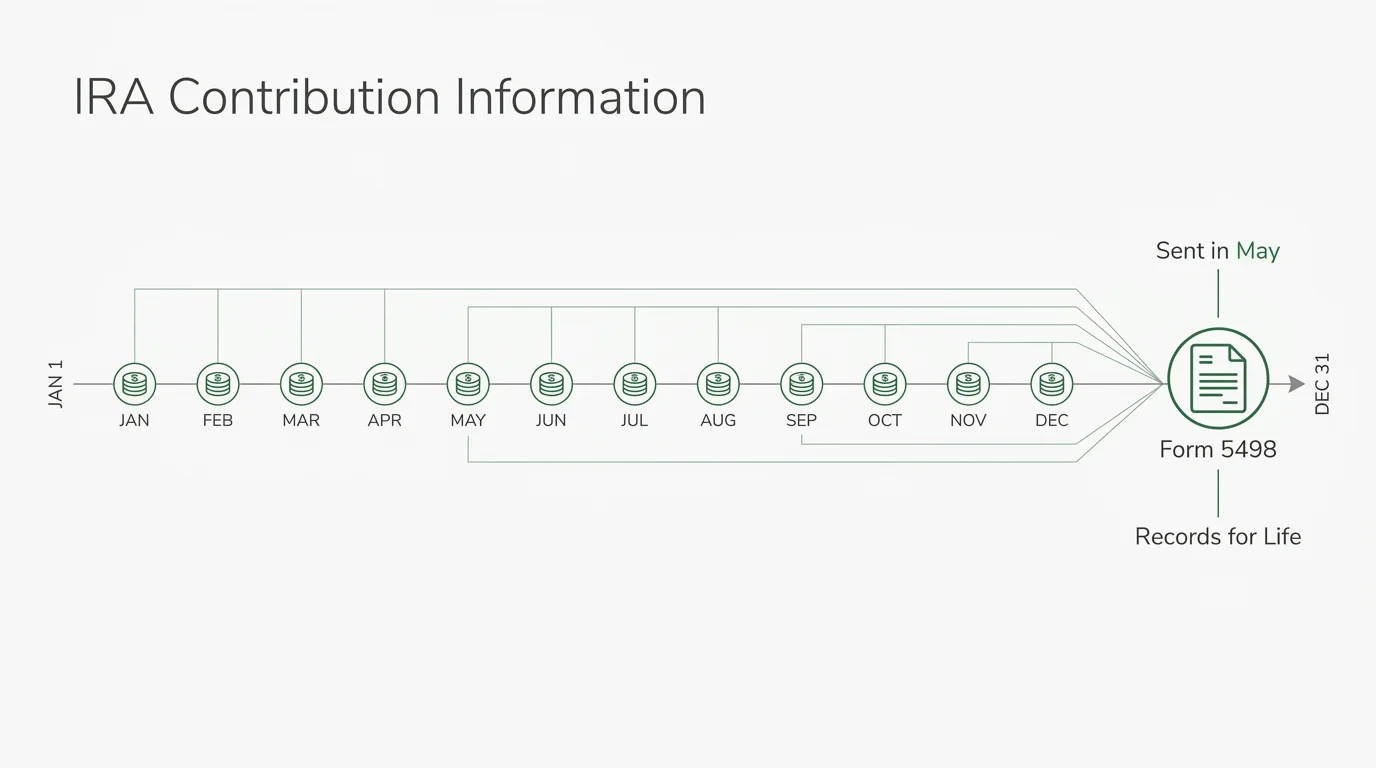

6. IRS Form 5498: IRA Contribution Information

Many seniors mistakenly throw away Form 5498 because it usually arrives in May, well after the April tax filing deadline. Financial institutions issue this form to report your IRA contributions, rollovers, and the Fair Market Value of your account at the end of the previous year.

Retaining Form 5498 is vital for tracking your Required Minimum Distributions. The IRS uses the Fair Market Value reported on this form to calculate exactly how much money you must withdraw from your tax-deferred accounts each year. Keeping a historical record of these forms helps you and your financial advisor accurately plan your annual withdrawals.

Additionally, if you made non-deductible contributions to a traditional IRA over your working years, your Form 5498 serves as a paper trail. It proves to the IRS that you already paid taxes on a portion of that money, ensuring you do not pay taxes twice when you eventually withdraw those funds.

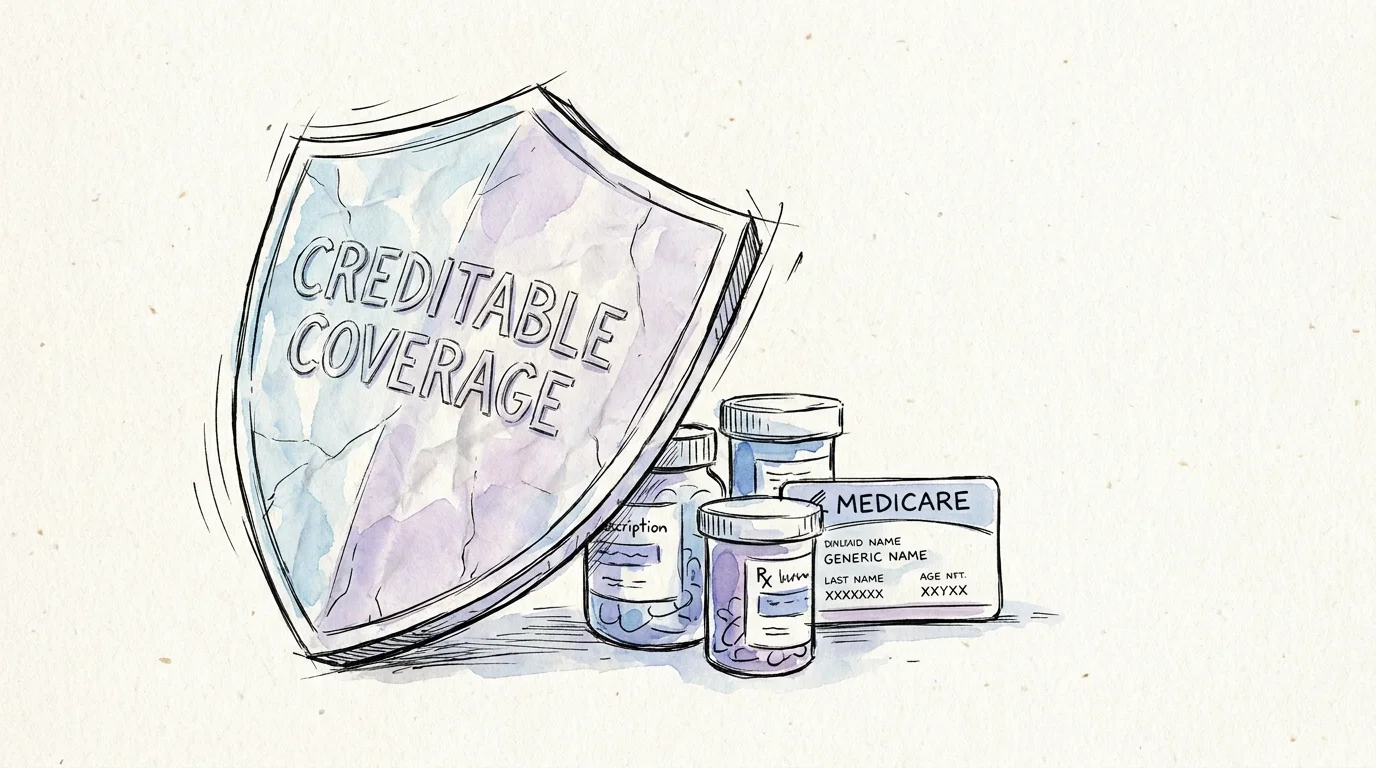

7. Medicare Creditable Coverage Notices

When you turn 65 and become eligible for Medicare, you must sign up for Medicare Part D (prescription drug coverage) unless you already have coverage that is considered “creditable”—meaning it pays out at least as much as standard Medicare coverage. If you continue working past 65 and stay on an employer or union health plan, they will send you a Creditable Coverage Notice every September.

You must keep these notices. If you eventually retire and decide to enroll in Medicare Part D at age 68, Medicare will want to know why you waited three years. Without proof of continuous creditable coverage, you will face a permanent late enrollment penalty. This penalty adds 1% of the “national base beneficiary premium” for every single month you were eligible for Part D but did not enroll.

According to the Centers for Medicare & Medicaid Services (CMS), these late enrollment penalties last for as long as you have Medicare prescription drug coverage. Storing your Creditable Coverage Notices in a safe place prevents this lifelong surcharge from draining your monthly budget.

8. IRS Form 1040: Annual Tax Returns

Your Form 1040 is the master document summarizing your annual federal income taxes. While you do not need to keep every tax return you have ever filed, you should absolutely retain your Form 1040 and all supporting schedules for at least the past seven years.

The IRS generally has three years to audit your return for good-faith errors, but they have up to six years to initiate an audit if they suspect you underreported your income by 25% or more. Holding onto seven years of tax returns provides an adequate buffer against any unexpected IRS inquiries.

Moreover, keeping your recent Form 1040s makes it significantly easier to fill out current-year tax forms. Having a physical record allows you to quickly reference your previous Social Security income, pension distributions, and standard deductions without relying on an accountant or a digital portal you might struggle to access.

9. State and Local Property Tax Exemption Forms

Many states and counties offer substantial property tax relief specifically designed to help seniors stay in their homes. These programs—often called senior freezes, homestead exemptions, or elderly property tax credits—require you to submit official applications and income verification forms to your local assessor’s office.

Once approved, you will receive official confirmation documents verifying your reduced tax rate or frozen property assessment. Never throw these away. Local governments occasionally update their computer systems or conduct municipal audits. If your senior exemption accidentally drops off your property record, your tax bill could double overnight.

Having the physical approval form allows you to immediately contest the error with your local tax assessor. When living on a fixed income, a sudden and unexpected property tax spike can threaten your financial stability; keeping your exemption paperwork ensures you can defend your rights.

Common Document Management Mistakes to Avoid

Managing years of paperwork can lead to simple mistakes with severe financial consequences. The most dangerous mistake seniors make is tossing official documents into the regular trash without shredding them. Scammers actively dig through household recycling bins looking for Social Security benefit statements, old tax returns, and Medicare forms. With just a few pieces of discarded mail, thieves can piece together your identity.

According to the Consumer Financial Protection Bureau (CFPB), older adults are prime targets for identity theft and financial exploitation. Fraudsters use stolen forms to open credit cards in your name, redirect your Social Security deposits to different bank accounts, or file fraudulent tax returns to steal your refund. Always invest in a cross-cut shredder and completely destroy any expired or redundant government forms.

Another common mistake is storing original, critical documents in bank safe deposit boxes without keeping accessible copies at home. If you pass away or become suddenly incapacitated, the bank will seal your safe deposit box until the probate court resolves the estate. This leaves your family completely unable to access your DD Form 214 for military burial benefits or your Social Security documents to report your passing.

How to Safely Store Your Government Forms

Protecting your documents requires a system that balances security with accessibility. Start by purchasing a fireproof and waterproof safe for your home. Use this safe to house your permanent, irreplaceable documents: your original Social Security Award Letter, your DD Form 214, and your most recent tax returns.

Create a “Grab and Go” binder for daily reference and emergencies. Use clear plastic sleeves to hold copies—never the originals—of your current Medicare Summary Notices, current property tax exemptions, and your latest SSA-1099. Keep this binder in a secure but easy-to-reach location. Tell your adult children, trusted caregiver, or power of attorney exactly where this binder lives.

If you are comfortable with technology, consider digitizing your records. Scan your essential government forms and save them onto an encrypted USB flash drive. Keep one flash drive in your home safe and give a duplicate drive to a trusted family member. Digital backups ensure that even if a natural disaster destroys your physical paperwork, you can print exact replicas of your most critical life documents immediately.

Frequently Asked Questions

How long should I keep old Medicare Summary Notices?

You should keep your Medicare Summary Notices (MSNs) for at least one full year. This gives you enough time to compare them against any lagging medical bills from your providers and dispute any fraudulent charges. Once a year has passed and all associated medical bills are paid and settled, you can safely shred the old MSNs.

What should I do if I lost my original Social Security Award Letter?

If you cannot find your original Social Security Award Letter, you can request a Benefit Verification Letter (also known as a proof of income letter). You can obtain this instantly by logging into your online account at the official SSA website, or you can call their national toll-free number to have a physical copy mailed to your home.

Do I need to keep tax returns forever?

No, you do not need to keep tax returns indefinitely. The general rule for seniors is to keep your IRS Form 1040 and all associated tax documents (like 1099s and W-2s) for seven years. This comfortably covers the IRS window for audits. Once a return is more than seven years old, use a cross-cut shredder to destroy it completely.

Is it safe to store my government forms digitally?

Yes, storing documents digitally is safe if done correctly. Never save sensitive government forms on public computers or email them to yourself unencrypted. Instead, scan the documents and save them to a password-protected external hard drive or a secure, encrypted cloud storage service. Always keep the physical originals of vital documents like the DD Form 214.

What happens if I lose my military discharge papers?

If you lose your DD Form 214, you can request a replacement copy from the National Archives. You can start the request online or mail in a specific request form (SF-180). Because processing times can vary widely and take several weeks, you should request a replacement immediately rather than waiting until you actually need the document for a benefit application.

For additional senior resources, visit

National Institute of Mental Health (NIMH), National Institutes of Health (NIH) and Centers for Medicare & Medicaid Services (CMS).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply