Rising property taxes easily threaten the financial security you worked decades to build, especially when you transition to a fixed income in retirement. Instead of cutting back on essentials like food and medication to keep your home, you can tap into local, state, and federal tax relief programs designed specifically to lower your housing costs. Municipalities across the country offer distinct property tax reductions, assessment freezes, and deferrals to keep older adults safely housed. Because these benefits are rarely applied automatically, you must proactively discover and claim them. Review these nine actionable property tax relief programs to uncover significant annual savings, protect your home equity, and stretch your retirement budget much further.

Why Property Tax Relief Matters for Older Adults

Living on a fixed income presents unique challenges when housing costs continue to rise. While you can pay off your mortgage, you can never truly pay off your property taxes. Local governments regularly reassess home values; as a result, your property taxes climb even if you make zero improvements to your property. This dynamic disproportionately harms seniors who bought their homes decades ago in neighborhoods that have since seen massive surges in real estate values.

According to research and advocacy updates from AARP, reducing housing costs remains one of the most effective ways for older adults to maintain independence and financial stability. Finding local tax relief directly reduces your monthly and annual expenses, freeing up cash flow for medical care, healthy groceries, and quality of life improvements. The programs outlined below exist entirely to prevent seniors from being taxed out of their own homes. By understanding how each mechanism works, you can identify which programs apply to your specific financial situation.

1. Senior Homestead Exemptions

Homestead exemptions serve as the first line of defense against steep property tax bills. While many states offer a standard homestead exemption for any owner-occupied primary residence, dozens of states provide an enhanced exemption specifically tailored for senior citizens. An exemption works by legally reducing the assessed value of your home before the tax rate is applied.

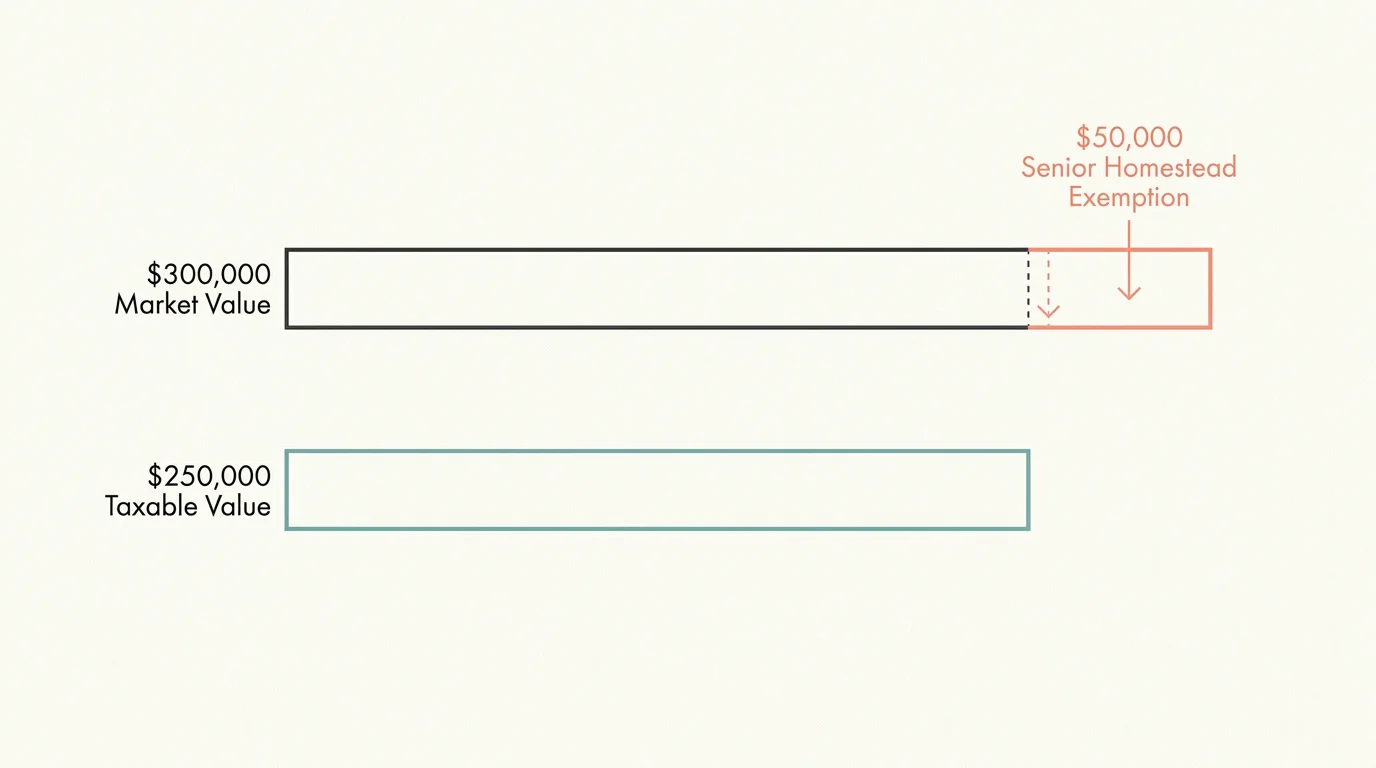

Consider a practical example. If your local tax assessor values your home at $300,000, and your local tax rate is 2%, your annual property tax bill equals $6,000. However, if your state offers a $50,000 senior homestead exemption, the county only taxes your home on a value of $250,000. This single adjustment lowers your tax bill to $5,000, immediately keeping $1,000 in your pocket.

To qualify for a senior homestead exemption, you typically must meet age requirements—usually 65 or older, though some states lower this to 61 or 62. Additionally, you must prove the home serves as your primary residence. Some jurisdictions also impose income limits to ensure the relief targets those who need it most. You must file the necessary paperwork directly with your county tax assessor or local appraisal district to activate this benefit.

2. Property Tax Freezes to Lock In Your Rate

If you live in a rapidly gentrifying area or a booming real estate market, your home’s assessed value might double over a short period. A property tax freeze acts as a financial anchor. Rather than reducing your current tax bill, a freeze locks in either your home’s assessed value or your actual tax payment amount at a specific baseline year.

Once you qualify for a freeze, you shield yourself from future municipal tax hikes. Even if the homes around you sell for record prices and cause neighborhood tax assessments to soar, your tax responsibility remains steady. This predictability makes budgeting on a fixed retirement income dramatically easier.

Eligibility for a freeze generally centers around age and income. You typically must renew your application annually, providing your latest tax returns or Social Security statements to prove your income remains below the mandated threshold. Keep in mind that a tax freeze usually breaks if you make significant additions to the home, such as building a new detached garage or adding a second story, as these actions trigger a baseline reassessment.

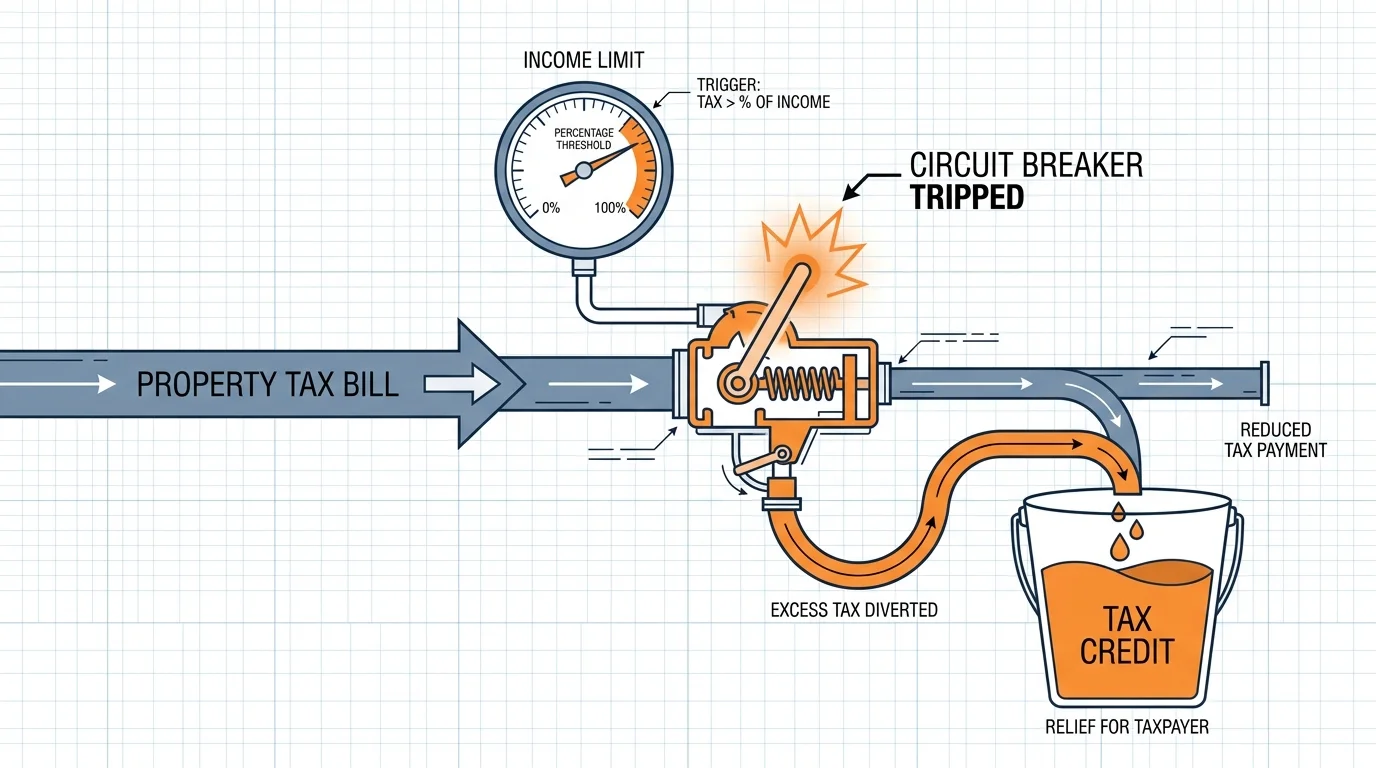

3. Circuit Breaker Programs for Income-Based Relief

Much like an electrical circuit breaker prevents a power surge from damaging your home, a property tax circuit breaker prevents a tax surge from damaging your finances. These programs trigger financial relief when your property taxes exceed a certain percentage of your annual income. They operate on the principle that no one should spend a disproportionate amount of their earnings solely to keep up with local taxes.

Here is how a typical circuit breaker functions: Your state might determine that property taxes should not exceed 5% of a senior’s income. If you earn $40,000 a year, your maximum acceptable tax burden is $2,000. If your actual property tax bill arrives at $3,500, the circuit breaker activates. The state then compensates you for the $1,500 difference.

States distribute this relief in different ways. Some apply a direct credit to your property tax bill before you pay it. Others require you to pay the tax upfront and claim the difference as a refundable credit on your state income tax return. Because circuit breakers rely entirely on income rather than home value, they provide a powerful lifeline for house-rich, cash-poor retirees.

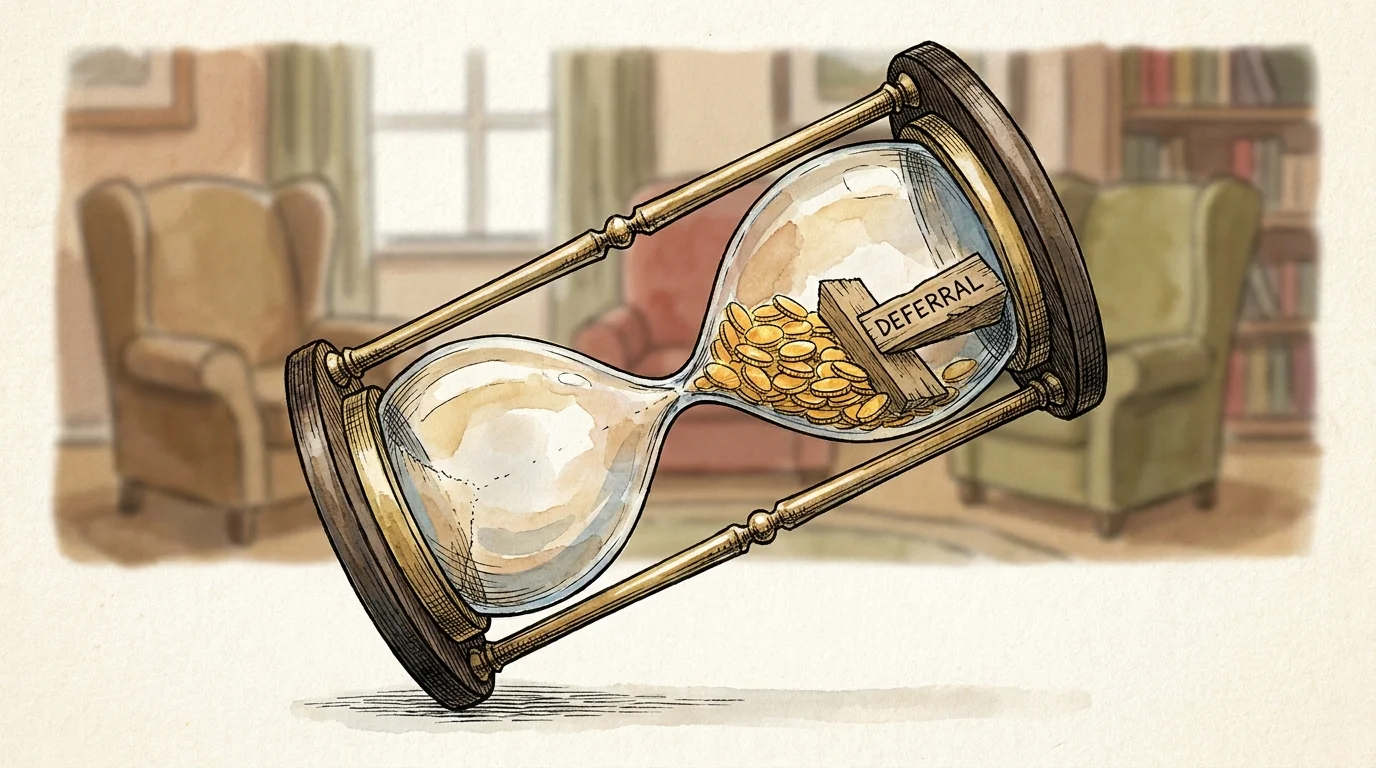

4. Property Tax Deferrals to Delay Payments

When you cannot afford your property taxes but do not qualify for exemptions or circuit breakers, deferral programs offer a crucial alternative. A deferral allows you to postpone paying your property taxes until a later date. The local government effectively pays the tax bill on your behalf and places a lien on your property for the deferred amount plus a moderate, state-regulated interest rate.

You do not have to repay the deferred taxes immediately. The debt only becomes due when you sell the property, transfer ownership, or pass away. At that point, the accumulated taxes and interest are paid out of the proceeds of the home sale. This mechanism allows you to leverage your home equity to cover your living expenses without taking out a commercial loan or a reverse mortgage.

While deferrals solve immediate cash-flow crises, they do erode the equity you plan to leave to your heirs. Weigh this option carefully and discuss it with your family to ensure everyone understands the long-term impact on the estate.

| Feature | Property Tax Exemption | Property Tax Deferral |

|---|---|---|

| How it Works | Permanently reduces the amount of tax you owe. | Postpones your tax payment to a later date. |

| Repayment | No repayment required. The money is yours to keep. | Must be repaid with interest when you sell the home or pass away. |

| Impact on Estate | Leaves your home equity fully intact for your heirs. | Reduces the final value of the estate left to your heirs. |

| Best For | Seniors meeting local age and income guidelines. | House-rich, cash-poor seniors who need immediate relief. |

5. Disabled Veteran Property Tax Exemptions

If you served in the military and sustained a service-connected disability, you likely qualify for substantial property tax relief. Nearly every state offers specialized exemptions to honor and support disabled veterans. The level of relief almost always corresponds directly to your disability rating assigned by the Department of Veterans Affairs (VA).

For example, a senior veteran with a 50% disability rating might receive a partial exemption that slices thousands of dollars off their home’s assessed value. However, if you hold a 100% service-connected permanent and total (P&T) disability rating, many states completely eliminate your property tax burden. Living 100% property tax-free represents one of the most powerful financial benefits available to older veterans.

To claim this benefit, you need to provide your local tax assessor with a current benefits letter from the VA detailing your exact disability rating. You only need to present this documentation once in many jurisdictions, though some require periodic verification.

6. Senior Tax Work-Off Programs

Dozens of towns and municipalities offer innovative senior tax work-off programs. These programs allow you to trade your time and skills for a direct reduction in your property tax bill. It serves as an excellent way to stay engaged with your community while saving money.

Participants take on part-time roles within local government operations. You might answer phones at the town hall, assist in the municipal library, serve as a crossing guard, or help maintain local parks. The city tracks your hours and credits your tax bill at the state minimum wage rate, up to a maximum allowed credit—often ranging between $1,000 and $2,000 per year.

Beyond the financial relief, these programs provide profound social benefits. They foster community connections, provide a sense of purpose, and keep you active. Contact your town manager’s office or local senior center to see if a work-off program operates in your area.

7. Surviving Spouse Tax Benefits

Losing a spouse brings overwhelming emotional pain, and the ensuing financial transition often compounds the stress. To soften this blow, many states allow surviving spouses to retain the property tax benefits their deceased partner initially earned. This continuation of benefits applies frequently to senior homestead exemptions, disability exemptions, and veteran tax relief.

Unfortunately, local governments do not automatically roll these benefits over to the surviving spouse. Because the tax assessor’s office relies on the name registered to the exemption, the death of the primary applicant can accidentally trigger a removal of the tax break. To protect your finances during this vulnerable time, you must contact your tax assessor and formally request to transfer the surviving spouse benefits into your name. Doing so prevents an unexpected, massive tax bill from arriving the following year.

8. Home Accessibility Abatement Programs

As you plan to age in place, you will likely need to modify your home. Installing exterior wheelchair ramps, widening doorways, lowering kitchen counters, and adding walk-in safety tubs all improve your daily safety. Under normal circumstances, improving a property increases its assessed value, which in turn raises your taxes.

However, many states recognize that taxing seniors for essential medical and accessibility upgrades is fundamentally unfair. Home accessibility abatement programs ensure that improvements made specifically to accommodate aging, illness, or disability do not trigger a reassessment of your home’s value.

Before you hire contractors to modify your home, contact your local appraisal district. Ask for the specific forms needed to register your upcoming renovations as accessibility modifications. By properly documenting the construction, you shield yourself from the penalty of higher taxes just for making your home safe to live in.

9. Federal Deductions for State and Local Taxes (SALT)

While local governments handle the direct assessment and billing of property taxes, the federal government offers a way to ease the pain on your annual income tax return. The State and Local Tax (SALT) deduction allows you to deduct the property taxes you pay from your federally taxable income.

To utilize the SALT deduction, you must itemize your deductions rather than taking the standard deduction. Current tax law caps the SALT deduction at $10,000 per year (or $5,000 if married and filing separately). If your total deductible expenses—including property taxes, state income taxes, mortgage interest, and large medical expenses—exceed the standard deduction for your age bracket, itemizing can result in a significant federal tax refund.

Because the standard deduction for seniors is relatively high, you should consult with a certified public accountant (CPA) or a volunteer tax preparer to determine if itemizing makes financial sense for your specific situation.

How to Apply for Senior Property Tax Relief

Discovering that you qualify for a tax break is only the first step; you must actively navigate the application process to secure the savings. Follow these actionable steps to ensure you do not leave money on the table:

- Locate the Right Office: Start by identifying the entity that issues your property tax bill. This is usually the county tax assessor, the local appraisal district, or the municipal tax collector.

- Gather Your Documentation: Prepare a folder with your government-issued ID (to prove your age), your most recent property tax bill, the deed to your home (to prove ownership), and your latest state and federal tax returns (to prove income limits).

- Check Application Deadlines: Property tax relief programs operate on strict, unforgiving deadlines. Many jurisdictions require applications to be submitted by March 1st or April 15th to apply to the current year’s tax bill. Missing the deadline usually means waiting an entire year for relief.

- Submit in Person or via Certified Mail: Whenever possible, drop off your application directly at the assessor’s office and request a stamped receipt. If you mail the documents, use certified mail so you have a tracking number proving you met the deadline.

You can also explore broad federal and state benefit structures by using the tools provided by Benefits.gov to uncover additional financial assistance. Their eligibility questionnaires can point you toward state-specific portals that manage circuit breaker and deferral applications.

Common Mistakes and Scams Targeting Senior Homeowners

While pursuing property tax relief, you must remain vigilant against costly errors and predatory schemes designed to separate you from your savings. The most common mistake seniors make involves assuming that relief automatically kicks in at age 65. Municipal software systems rarely track your birth date; the burden of claiming the benefit rests entirely on you.

Furthermore, aggressive scammers heavily target senior homeowners. You might receive official-looking letters in the mail offering to file your property tax exemption paperwork or appeal your home’s assessed value for an upfront fee of $100 to $200. These solicitations often feature alarming language threatening massive tax hikes if you fail to act.

Experts at the Consumer Financial Protection Bureau (CFPB) routinely warn homeowners to avoid companies that charge fees to file standard, free exemption paperwork. Your local tax assessor’s office provides the application forms at no cost, and their staff will gladly help you fill them out for free. Never pay a third-party company to file an exemption you can submit yourself.

Another dangerous pitfall occurs when seniors casually transfer the deed of their home to their adult children, perhaps attempting to simplify estate planning. Transferring the deed changes the legal ownership of the property. The moment your name comes off the deed, you immediately lose your senior homestead exemptions and property tax freezes, which can trigger a catastrophic spike in the property tax bill.

Frequently Asked Questions

Does paying off my mortgage stop my property taxes?

No. Your mortgage and your property taxes are entirely separate obligations. When you pay off your mortgage, you stop paying your lender, but you still owe annual property taxes to your local government for as long as you own the home. You must arrange to pay these taxes directly to the county, rather than through a mortgage escrow account.

Can I claim a senior property tax exemption on a vacation home?

No. Almost all property tax relief programs mandate that the property must serve as your primary, principal residence. You cannot claim senior homestead exemptions or circuit breakers on summer cabins, investment properties, or secondary homes.

Do I have to reapply for my senior exemption every year?

Requirements vary by municipality. Some counties automatically renew your senior homestead exemption once you apply the first time. However, income-based programs—such as circuit breakers and property tax freezes—almost always require annual renewal. You must submit your latest financial documents each year to prove you still fall below the income thresholds.

What if I missed the deadline to file for my property tax relief?

If you miss the deadline, contact your assessor’s office immediately. A handful of states offer grace periods or allow for retroactive filing if you can prove medical hardship or extenuating circumstances. Otherwise, you will have to pay the full tax amount for the current year and submit your application for the following year.

Where can I get free help applying for these programs?

If you need local assistance navigating these applications, reach out to your Area Agency on Aging through the Eldercare Locator. Additionally, local senior centers and volunteer tax assistance programs (like those run by AARP) routinely provide free help gathering documents and completing municipal paperwork.

For additional senior resources, visit

National Institute on Aging (NIA), Centers for Disease Control and Prevention (CDC) and Medicare.gov.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply