Navigating retirement on a fixed income means stretching every dollar, but you do not have to manage rising costs alone. Billions of dollars in federal and state funds are set aside each year to help older adults cover essential living expenses. These government assistance programs provide crucial relief for housing, healthcare, groceries, and utility bills, ensuring you maintain a comfortable lifestyle. Many seniors unknowingly miss out on these retirement support benefits simply because they assume they earn too much or find the application process overwhelming. By understanding the specific financial aid programs available, you can confidently claim the senior financial assistance you deserve and protect your hard-earned savings from unexpected financial strain.

Supplemental Security Income (SSI): Boosting Your Monthly Budget

Supplemental Security Income, commonly known as SSI, acts as a vital financial safety net for older adults with limited income and resources. Unlike standard Social Security retirement benefits—which depend on your lifetime earnings and work history—SSI is entirely needs-based. This means you can receive SSI even if you have never worked, provided you meet the financial requirements.

According to the Social Security Administration (SSA), SSI provides monthly cash payments to adults aged 65 and older, as well as to individuals with disabilities. You can use these funds for your most basic needs, including rent, groceries, clothing, and utility bills.

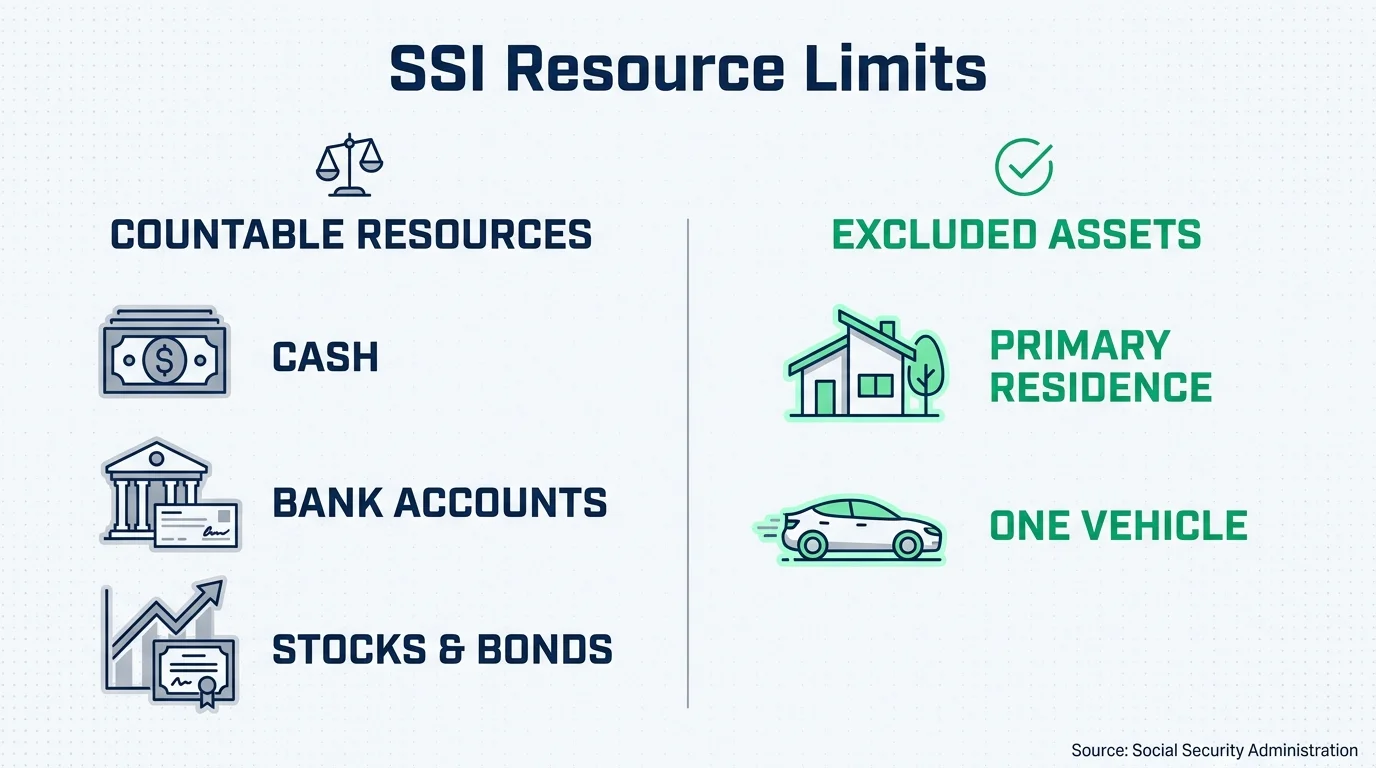

To qualify for this senior financial assistance, you must meet specific resource limits. The government looks at your “countable resources,” which generally include cash, bank accounts, stocks, and bonds. However, the SSA excludes certain major assets from this calculation. Your primary residence, the land it sits on, and one vehicle used for transportation typically do not count against your resource limits.

Applying for SSI requires providing documentation of your current income and assets. You will need to gather your bank statements, lease agreements, and proof of any other income you receive, such as pensions or standard Social Security benefits. Applying online or calling your local Social Security office is the fastest way to initiate your claim.

Medicare Savings Programs (MSPs): Cutting Healthcare Costs

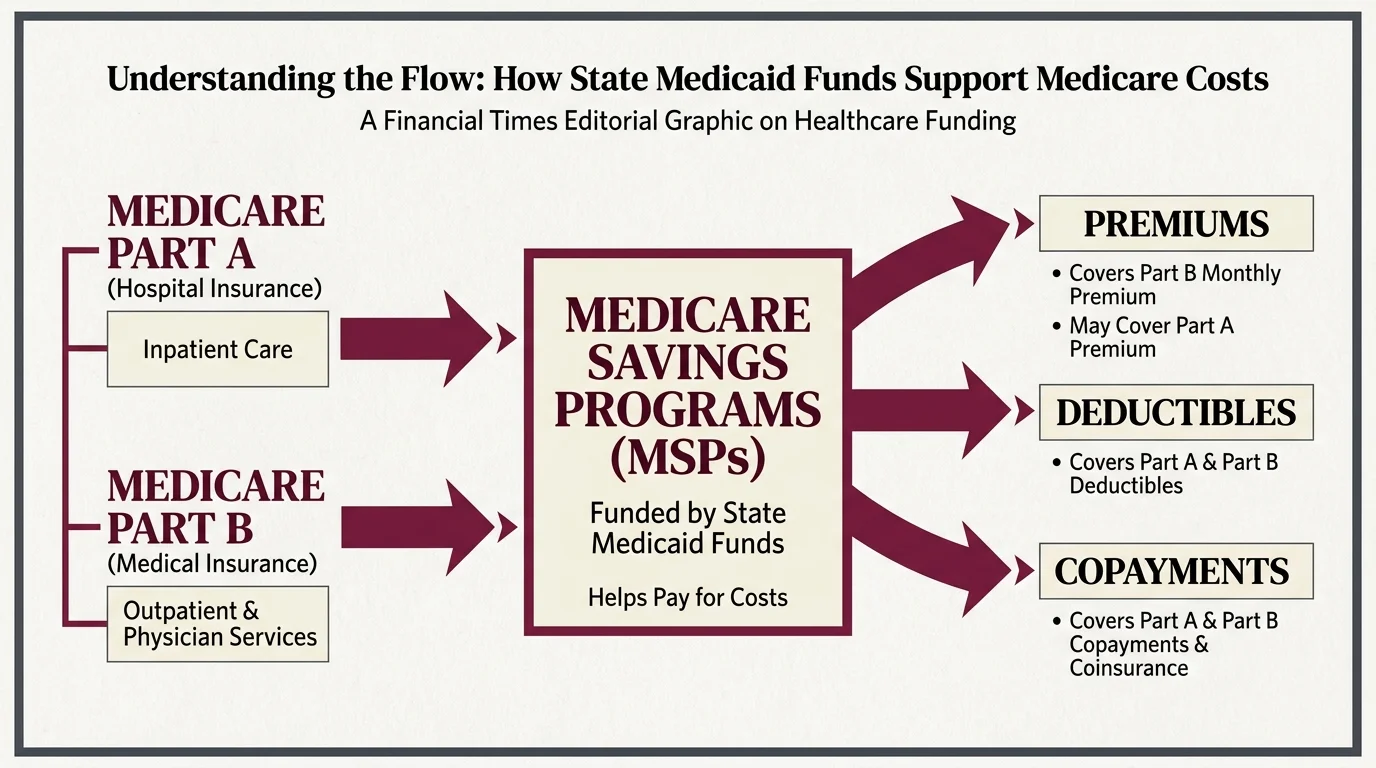

Healthcare costs consistently rank among the highest expenses for retirees. Even with Medicare coverage, out-of-pocket costs like premiums, deductibles, and copayments quickly drain a fixed budget. Medicare Savings Programs (MSPs) exist specifically to lift this burden by using state Medicaid funds to pay for your Medicare Part A and Part B costs.

There are four distinct types of MSPs, each with its own income limits and benefits. Depending on your financial situation, your state may cover your premiums, and in some cases, your deductibles and coinsurance as well.

| Program Name | What It Covers | Best For |

|---|---|---|

| Qualified Medicare Beneficiary (QMB) | Part A premiums, Part B premiums, deductibles, coinsurance, and copayments. | Seniors with the lowest income and limited resources who need comprehensive cost coverage. |

| Specified Low-Income Medicare Beneficiary (SLMB) | Part B premiums only. | Seniors whose income is slightly too high for QMB but still require help with monthly Part B costs. |

| Qualifying Individual (QI) | Part B premiums only. | Seniors needing Part B premium help. Funds are limited and granted on a first-come, first-served basis. |

| Qualified Disabled and Working Individuals (QDWI) | Part A premiums only. | Working seniors with a disability who lost premium-free Part A when they returned to work. |

Because states manage these programs, income thresholds vary based on where you live. Some states have even eliminated the asset test entirely, making it much easier to qualify. If you struggle to pay your medical bills, applying for an MSP is a crucial step toward stabilizing your finances.

The Extra Help Program: Lowering Prescription Drug Prices

Managing chronic conditions often requires multiple prescription medications. If you have Medicare Part D, you know that the costs of these drugs fluctuate and sometimes spike to unmanageable levels. The Extra Help program—also known as the Part D Low-Income Subsidy—is a federal initiative designed to reduce these costs dramatically.

When you qualify for Extra Help, the program pays for your Part D monthly premiums, annual deductibles, and coinsurance. It also eliminates the dreaded Part D late enrollment penalty if you delayed signing up for coverage. Most importantly, it caps your out-of-pocket costs for each prescription at a low, fixed amount. For many seniors, a medication that once cost hundreds of dollars a month drops to just a few dollars per refill.

An important benefit of the system is the automatic enrollment feature. If you already receive Medicaid, Supplemental Security Income (SSI), or participate in a Medicare Savings Program, you automatically qualify for Extra Help. You do not need to fill out a separate application. If you do not automatically qualify, you can still apply through the Social Security Administration.

Low-Income Home Energy Assistance Program (LIHEAP): Managing Utility Bills

Extreme temperatures pose serious health risks for older adults. Staying warm in the winter and cool in the summer is not a luxury; it is a medical necessity. The Low-Income Home Energy Assistance Program (LIHEAP) offers financial help for seniors struggling to manage their home energy bills.

LIHEAP operates through a network of local community action agencies and social service departments. The program provides several types of vital support:

- Direct Bill Payment: LIHEAP sends funds directly to your utility company to lower your outstanding balance or cover upcoming heating and cooling costs.

- Crisis Assistance: If you face an immediate utility shut-off or have run out of heating oil during a harsh winter, LIHEAP offers emergency funds to restore or maintain your services.

- Weatherization Repairs: The program often covers minor, energy-related home repairs. This includes adding insulation, sealing drafty windows, or repairing a broken furnace, which lowers your bills permanently.

Because funding is distributed locally, you must apply through your state or tribal government. To locate the specific agency handling applications in your county, the official Benefits.gov portal provides a reliable directory of state resources. Applying early in the season is critical, as states distribute LIHEAP funds on a first-come, first-served basis until the money runs out.

Supplemental Nutrition Assistance Program (SNAP): Affording Healthy Groceries

Proper nutrition is the foundation of healthy aging. Unfortunately, rising grocery store prices force many seniors to choose between buying fresh, nutritious food and paying for medication. The Supplemental Nutrition Assistance Program (SNAP) addresses this problem directly by providing funds specifically for groceries.

Research from the National Institute on Aging (NIA) highlights the importance of a nutrient-rich diet in managing chronic illnesses like diabetes and heart disease. SNAP allows you to purchase fresh produce, lean proteins, dairy, and breads at authorized grocery stores, supermarkets, and even many local farmers’ markets.

Many seniors mistakenly believe they will not qualify for SNAP or assume the benefit amount is too small to justify the paperwork. However, the program features special rules designed exclusively for adults aged 60 and older. For example, if you have high out-of-pocket medical expenses, you can deduct a portion of those costs from your income when applying. This “excess medical expense deduction” effectively lowers your countable income, making it easier to qualify and potentially increasing your monthly benefit amount.

You receive your SNAP benefits on an Electronic Benefits Transfer (EBT) card, which looks and works exactly like a standard debit card. This ensures your transactions at the checkout counter remain private and seamless.

Housing Choice Voucher Program: Securing Affordable Rent

Securing safe, affordable housing is one of the most challenging aspects of living on a fixed income. Property taxes, maintenance, and rent prices continue to climb, pushing many seniors out of their lifelong communities. The Housing Choice Voucher Program, commonly referred to as Section 8, is the federal government’s primary program for assisting low-income individuals, the elderly, and people with disabilities to afford decent, safe housing in the private market.

Under this program, you are not restricted to subsidized housing projects. You can choose any privately owned apartment, townhome, or single-family home, provided the landlord agrees to rent under the program guidelines and the property meets basic health and safety standards.

The financial mechanics of the voucher program are straightforward. You are generally required to pay about 30% of your adjusted gross monthly income toward rent and utilities. Your local Public Housing Agency (PHA) pays the remaining balance directly to your landlord. This structure ensures that your housing costs always remain proportional to your income.

Waitlists for housing vouchers can be long, sometimes stretching for years. It is highly recommended to apply at multiple PHAs in your surrounding area. Gather your birth certificate, Social Security card, and proof of income beforehand to ensure your application processes smoothly once you reach the top of the list.

How to Safely Apply and Avoid Common Financial Scams

While exploring government assistance programs, you must remain vigilant. Scammers frequently target older adults by posing as government officials or helpful agents offering guaranteed financial aid programs.

The Consumer Financial Protection Bureau (CFPB) warns that fraudulent actors often use high-pressure tactics to steal personal information or money. They may call, email, or send text messages claiming you have been approved for a special senior grant—but insist you must pay a “processing fee” first.

To protect yourself and your assets, keep these safety rules in mind when applying for retirement support benefits:

- Never pay to apply: Legitimate government assistance programs are entirely free to apply for. If a website or caller demands a fee, wire transfer, or gift card to process your application, it is a scam.

- Verify the source: Always use official government websites ending in “.gov” when reading about benefits or submitting personal information. Avoid clicking on links in unsolicited emails.

- Guard your numbers: Never give out your Social Security number, Medicare number, or bank account details to someone who contacts you unexpectedly. The government will never call you out of the blue demanding this information.

- Seek local help: If you find applications confusing, utilize free local resources. Your local Area Agency on Aging or State Health Insurance Assistance Program (SHIP) employs trained counselors who provide free, unbiased help with benefit applications.

Frequently Asked Questions

Can I receive benefits from multiple financial aid programs at the same time?

Yes, absolutely. Many of these programs are designed to work together to provide comprehensive support. For example, it is very common for a senior to receive SNAP for groceries, LIHEAP for utilities, and the Extra Help program for prescriptions simultaneously. Qualifying for one program often makes it easier to prove your eligibility for others.

Does owning my home disqualify me from getting help?

In most cases, no. Programs like Supplemental Security Income (SSI) and Medicaid generally exclude the home you live in from their asset calculations. Similarly, programs like SNAP and LIHEAP base their eligibility primarily on your monthly income rather than the value of your primary residence. You can own your home and still receive significant assistance to maintain it.

How do I apply for these programs if I do not have a computer or internet access?

Every government program offers alternative ways to apply. You can call the specific agency (such as the Social Security Administration or your local social services office) to request a paper application by mail, or you can apply over the phone. Additionally, visiting your local senior center or public library can connect you with social workers who can print applications or fill them out with you in person.

Are the benefits I receive from these programs considered taxable income?

Generally, assistance based on financial need is not taxable. Benefits such as SNAP, LIHEAP, housing vouchers, and SSI are not considered gross income by the IRS and do not need to be reported on your taxes. Standard Social Security retirement benefits, however, may be partially taxable depending on your total overall income.

What happens if my application for a program is denied?

If you receive a denial letter, do not panic. The letter will explain the exact reason for the decision and provide instructions on how to appeal. Often, denials occur simply due to a missing document or a clerical error. You have the right to request an appeal, provide the missing information, and have your case reviewed again by a different representative.

For additional senior resources, visit

Medicare.gov, National Institute of Mental Health (NIMH) and National Institutes of Health (NIH).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Such valuable information is included here. I am going to make sure I share with other seniors I communicate with that could & should know of these items.