Facing end-of-life planning often brings emotional and financial stress, especially when average burial costs can quickly exceed $8,000. Taking control of your final arrangements now protects your loved ones from unexpected financial burdens during a time of grief. You have multiple practical strategies at your disposal to significantly reduce these expenses without sacrificing the dignity of a meaningful farewell. By understanding your options—from direct cremation and veteran benefits to targeted government assistance programs—you can make informed decisions that align with your budget and values. This guide explores eight proven methods to ease burial costs, providing you with the clear steps needed to secure peace of mind for both yourself and your family.

Way 1: Shop Around and Compare Funeral Home Prices

Most families simply choose the funeral home closest to their house or the one their family has used for generations. While loyalty and convenience matter, avoiding price comparisons is a fast way to overpay for funeral expenses. Funeral costs can vary by thousands of dollars within the same city for the exact same services.

According to the Consumer Financial Protection Bureau (CFPB), funeral homes are required by federal law to provide you with a written, itemized price list before discussing any arrangements. This mandate, known as the Federal Trade Commission (FTC) Funeral Rule, is a powerful tool for your end of life planning.

When you call or visit a funeral provider, ask for their General Price List (GPL). You have the right to purchase only the specific goods and services you want, rather than accepting a bundled package that includes items you do not need. For example, if you prefer a simple memorial service at your church or local community center, you can decline the funeral home’s facility rental fees.

To implement this strategy effectively, call three local funeral homes and request quotes for the specific services you desire. Compare their prices on major expenses like the basic services fee, transportation of the body, and merchandise like caskets or urns. Keep a written record of these quotes so your family knows exactly who to call and what to expect financially.

Way 2: Claim Your Social Security Lump-Sum Death Benefit

If you have worked and paid into the Social Security system, your family may be entitled to modest funeral financial help directly from the government. While it will not cover the entirety of a modern funeral, every bit of burial cost assistance matters when managing fixed incomes and estate transitions.

As noted by the Social Security Administration (SSA), a surviving spouse or dependent child may be eligible for a special lump-sum death payment of $255. This payment is typically made to the spouse who was living with the deceased at the time of death.

If the spouse was living apart, they may still be eligible if they were receiving certain Social Security benefits on the deceased’s record. If there is no surviving spouse, the payment can be made to a child who is eligible for benefits on the deceased’s record in the month of death.

To ensure your family receives this benefit, they must apply within two years of the date of death. They cannot complete this specific application online. Instead, your loved ones will need to call their local Social Security office or the national toll-free number to report the death and schedule an appointment to apply for the lump-sum payment. Keeping your Social Security number and vital records organized in a dedicated folder will make this process much smoother for your grieving family.

Way 3: Utilize Veterans Burial Benefits

If you served in the United States military and received a discharge other than dishonorable, you have earned significant burial benefits that can drastically reduce funeral expenses. Many veterans and their spouses are unaware of the full scope of these benefits, leaving valuable financial support unused.

The Department of Veterans Affairs (VA) provides several forms of burial support programs. Eligible veterans can receive a gravesite in any of the national cemeteries with available space, opening and closing of the grave, perpetual care, a government headstone or marker, a burial flag, and a Presidential Memorial Certificate. All of these services are provided at no cost to your family.

If you prefer to be buried in a private cemetery rather than a national one, the VA still provides a free headstone or marker, a burial flag, and a memorial certificate. Additionally, the VA pays a burial allowance to help cover funeral and burial costs. The amount of this allowance depends on whether the death was service-connected or non-service-connected.

To prepare your family to claim these benefits, you must locate your DD-214 form (Certificate of Release or Discharge from Active Duty). Store this document with your will and other essential end of life planning materials. Without the DD-214, the funeral director will face significant delays in securing your military burial honors and financial allowances.

Way 4: Choose Direct Cremation or Immediate Burial

One of the most effective ways to lower your final expenses is to alter the type of service you choose. Traditional funerals involve embalming, a viewing or wake, a formal funeral service, and a graveside burial. These events require the heavy involvement of funeral home staff, expensive facilities, and high-priced merchandise.

Direct cremation and immediate burial bypass these costly steps. In a direct cremation, the body is cremated shortly after death, without embalming, viewing, or a formal funeral service beforehand. The ashes are then returned to your family, who can host a meaningful, low-cost memorial service at a later date in a park, home, or place of worship.

Immediate burial follows a similar streamlined process. The body is buried shortly after death in a simple container, bypassing embalming and public viewings.

Review the table below to see a general comparison of national average costs for different end-of-life options:

| Type of Arrangement | Typical Services Included | Estimated Average Cost |

|---|---|---|

| Traditional Burial | Basic services fee, embalming, viewing, ceremony, hearse, premium casket, grave plot, headstone | $8,000 – $12,000+ |

| Immediate Burial | Basic services fee, transportation, simple casket, grave plot, headstone (no viewing/embalming) | $3,500 – $5,500 |

| Direct Cremation | Basic services fee, transportation, alternative container, crematory fee (no viewing/embalming) | $1,000 – $2,500 |

Choosing direct cremation or immediate burial represents an excellent way to secure funeral financial help by simply avoiding the most expensive line items on a funeral home’s price list.

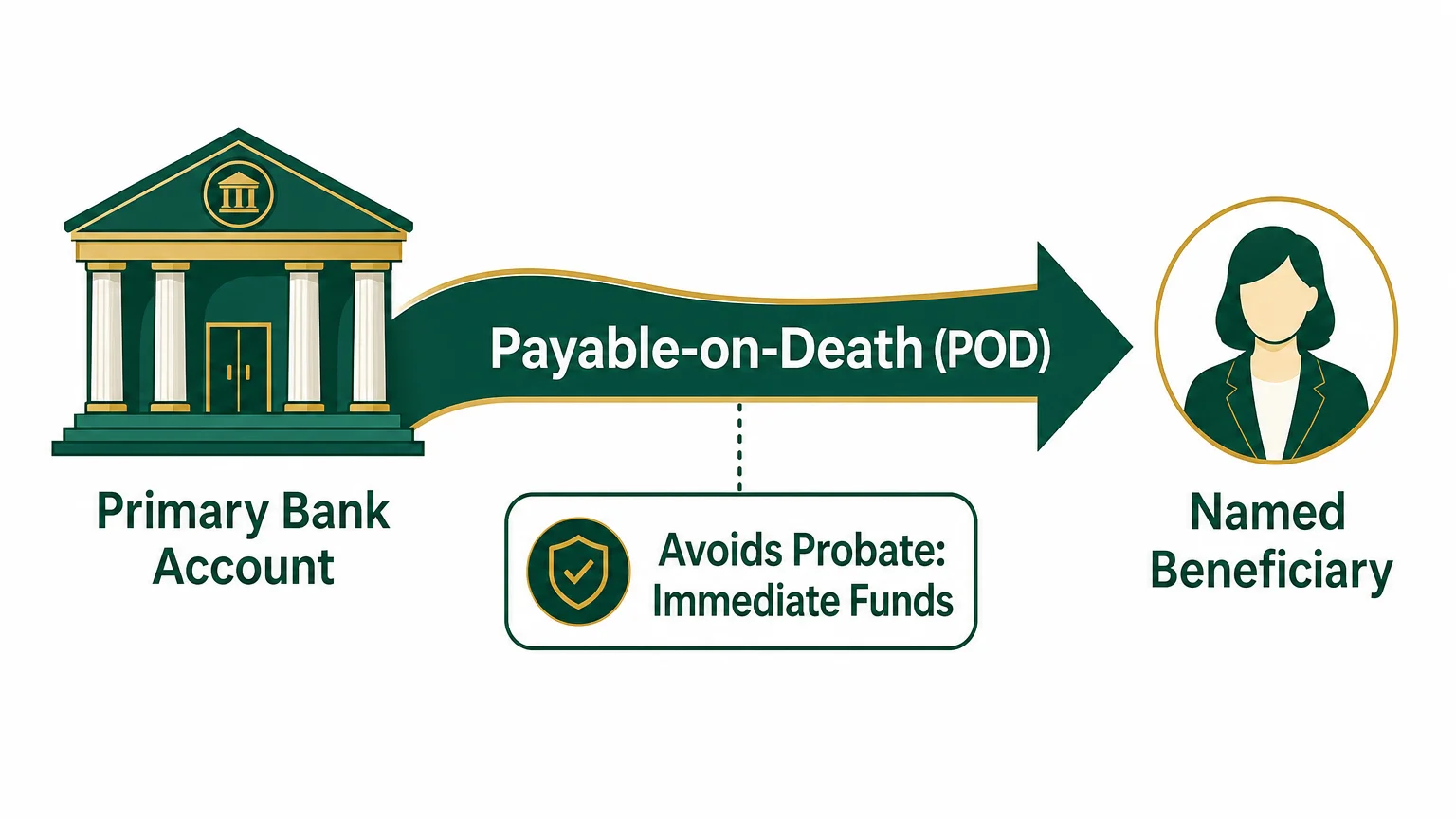

Way 5: Set Up a Payable-on-Death Bank Account

Even if you have enough money saved to cover your funeral, your family might struggle to access those funds immediately after you pass away. When a person dies, their standard bank accounts are often frozen until the estate goes through the probate process—a legal procedure that can take months or even years. Meanwhile, funeral homes typically require payment upfront.

To solve this problem, you can convert your standard savings or checking account into a Payable-on-Death (POD) account. This is sometimes called a Totten Trust. By establishing a POD account, you designate a specific beneficiary—such as your spouse or an adult child—who will receive the funds immediately upon your death.

The money in a POD account bypasses the lengthy probate process. To access the cash, your designated beneficiary simply needs to present a valid death certificate and their own personal identification to the bank. They can then withdraw the funds and pay the funeral director without resorting to high-interest credit cards or personal loans.

Setting up a POD account is entirely free. Visit your local bank branch, request a beneficiary designation form for your existing account, and fill in the details of your chosen representative. You retain full control of the money while you are alive, meaning you can spend it, withdraw it, or change the beneficiary at any time.

Way 6: Explore State and Local Assistance Programs

If you have very limited income and assets, you might qualify for state or county burial cost assistance. Many local municipalities operate “indigent burial” programs designed to ensure that community members receive a respectful disposition, regardless of their financial status.

You can search for local support and specialized grants through Benefits.gov, which connects citizens with government assistance programs based on specific needs. Most states handle burial assistance at the county level through the Department of Human Services, the Department of Social Services, or the local coroner’s office.

Funding and eligibility requirements vary drastically by zip code. In some counties, the government will provide a small cash grant (often between $300 and $1,000) directly to the funeral home to offset expenses. In other jurisdictions, the county maintains contracts with specific funeral homes to provide direct cremation or a basic burial at no cost to the family.

Be aware that utilizing these burial support programs often comes with strict limitations. The county usually dictates the type of service provided, which is almost always a direct cremation or an immediate burial in a specific cemetery. Families are rarely allowed to upgrade caskets or add expensive memorial services when utilizing indigent burial funds.

Way 7: Consider Whole-Body Donation to Science

If you are passionate about advancing medical research and education, donating your body to science is a noble choice that also acts as a profound form of funeral financial help. Medical schools, research hospitals, and private anatomical donation organizations rely on these generous gifts to train the next generation of doctors and discover new medical treatments.

When you register for whole-body donation, the receiving institution generally covers the cost of transporting your body from the place of death to their facility. Once their research or educational program is complete—which can take several weeks to a few years—the institution will typically cremate the remains at their own expense. They will then return the cremated ashes to your family or scatter them in a dignified manner, depending on your prior instructions.

If you choose this route, you must register with a specific program well in advance. Keep your registration card in your wallet and inform your next of kin about your decision, as they will need to contact the institution immediately upon your death.

It is critical to have a backup plan. Medical programs can reject a donation at the time of death for various reasons, including specific infectious diseases, extreme obesity, or if the facility currently has no space. Ensure your family knows what to do and how to handle expenses if the anatomical donation falls through.

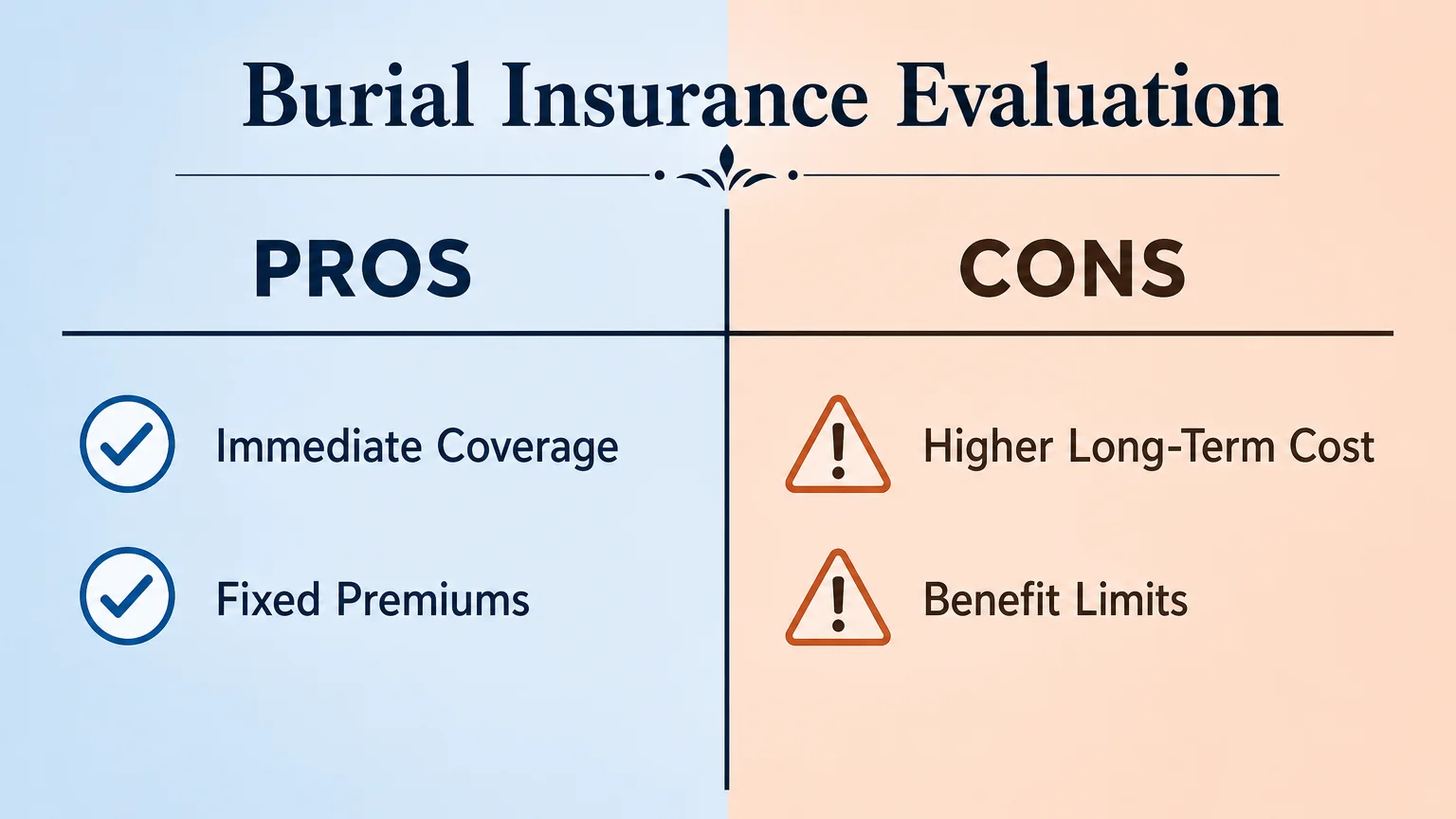

Way 8: Weigh the Pros and Cons of Burial Insurance

Burial insurance, also known as final expense insurance, is a small whole-life insurance policy designed specifically to cover funeral expenses. The death benefit usually ranges from $5,000 to $25,000. These policies are heavily marketed to seniors because they rarely require a medical exam; acceptance is often guaranteed based on a short health questionnaire.

While burial insurance provides cash to your beneficiaries to handle your final arrangements, it requires careful consideration. The premiums for these policies are typically high relative to the small payout you receive.

Research from AARP suggests carefully reviewing any pre-need or burial insurance contract, as some policies may cost you more in premiums than they eventually pay out in benefits. If you live for many years after purchasing a guaranteed-issue policy, you could end up paying $10,000 in premiums for a policy that only pays out $7,000.

Before purchasing burial insurance, evaluate your existing assets. If you have substantial savings, a traditional life insurance policy, or a POD bank account, you likely do not need specialized final expense insurance. However, if you have no savings and want to ensure your family is not burdened with out-of-pocket costs, a carefully vetted burial insurance policy from a reputable provider can offer valuable peace of mind.

Watch Out for Common Funeral Planning Scams

The funeral industry is largely filled with compassionate professionals dedicated to helping grieving families. However, the emotional vulnerability of end of life planning makes seniors and their loved ones prime targets for upselling and predatory practices.

Protect your estate by familiarizing yourself with these common pitfalls:

- The Embalming Myth: Some unscrupulous providers may imply that embalming is a legal requirement. In truth, no state legally requires routine embalming for every death. Refrigeration is a legally acceptable and much cheaper alternative if a viewing or burial is delayed.

- Casket Requirements for Cremation: You never have to buy a traditional wooden or metal casket for a cremation. The FTC Funeral Rule explicitly states that funeral homes must offer you an “alternative container” (usually made of heavy cardboard or unfinished wood) which costs a fraction of the price.

- Protective Caskets and Vaults: Salespeople may try to sell you a casket with a “rubber gasket” or “sealer,” claiming it will preserve the body forever by keeping out water and dirt. No casket or vault can permanently prevent natural decomposition. Paying extra for these protective seals is an unnecessary expense.

- Guilt-Tripping: Beware of subtle language designed to make you feel guilty for choosing affordable options. Statements like, “Given your mother’s standing in the community, I’m sure you want the premium package,” are manipulative sales tactics. Focus on what honors your loved one’s actual wishes and your budget.

Frequently Asked Questions

Does Medicare or Medicaid pay for funeral expenses?

Medicare does not cover any funeral or burial costs. However, if you are a low-income senior enrolled in Medicaid, you might be eligible for state-specific burial cost assistance. Some states allow families to use a small portion of a deceased person’s Medicaid funds for burial, but rules are extremely strict and vary widely by location. Always check with your local Medicaid office for exact guidelines.

Can I prepay for my funeral directly with a funeral home?

Yes, you can purchase a “pre-need” contract directly from a funeral home to lock in today’s prices for tomorrow’s services. While this guarantees your wishes are recorded, it carries risks. If the funeral home goes out of business, changes ownership, or if you move to a different state, you may lose the money you invested. Always ask where the prepaid funds are held (they should be in a third-party trust) and whether the contract is transferable.

What happens if my family absolutely cannot afford a burial?

If your estate has no assets and your family cannot afford any funeral expenses, the county or municipality will step in. The local coroner or health department will arrange for a direct cremation or a basic burial in a county cemetery. The family will not have control over the details of the service, but the disposition will be handled respectfully according to local health laws.

Can I build my own casket or buy one online?

Yes. Federal law guarantees your right to purchase a casket from a third-party retailer, such as a warehouse club or an online merchant, and the funeral home must accept it without charging you a handling fee. Furthermore, it is perfectly legal in all 50 states to build your own casket or have a family member build one for you, which can save thousands of dollars.

For additional senior resources, visit

American Heart Association,

Benefits.gov and

National Institute on Aging (NIA).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply