Retirement offers a profound opportunity to redesign your daily life on your own terms, but navigating this transition requires careful strategy. Without the safety net of a regular paycheck, seemingly minor oversights can rapidly compound into significant financial and emotional burdens. To protect your hard-earned savings and preserve your peace of mind, you need to recognize the common traps that derail many retirees. By understanding exactly what behaviors and decisions to avoid, you can build a resilient foundation for your golden years. Read on to discover the top missteps in finance, healthcare, lifestyle, and security that you must sidestep to ensure a comfortable, secure, and deeply fulfilling retirement.

Financial Missteps to Avoid

1. Claiming Social Security Too Early

One of the most consequential choices you will make involves your Social Security benefits. Many seniors rush to claim benefits at age 62, the earliest possible opportunity. While this provides an immediate income stream, it permanently locks in a reduced monthly payout—sometimes by as much as 30 percent compared to what you would receive at your full retirement age. According to the Social Security Administration (SSA), delaying your claim past your full retirement age actually earns you delayed retirement credits. These credits increase your benefit by roughly 8 percent per year until you reach age 70. Unless you have pressing health concerns or immediate financial hardship, practicing patience with your claiming strategy provides a guaranteed way to boost your lifelong, inflation-adjusted income.

2. Ignoring Required Minimum Distributions (RMDs)

If you have money saved in tax-advantaged retirement accounts like a traditional IRA or a 401(k), the IRS mandates that you begin taking withdrawals at a specific age. Missing your Required Minimum Distribution (RMD) triggers one of the steepest penalties in the tax code. If you fail to withdraw the required amount, you face an excise tax of up to 25 percent on the amount you were supposed to take out. To prevent this severe financial penalty, you should calculate your RMDs early in the year and set up automated transfers with your brokerage firm. Staying ahead of this requirement ensures you remain compliant with tax laws and keeps your money working for you rather than being forfeited to penalties.

3. Failing to Adjust Your Investment Risk

The investment strategy that built your wealth during your working years is rarely the best strategy for preserving it in retirement. Continuing to hold an overly aggressive portfolio exposes you to the sequence of returns risk; if the stock market crashes early in your retirement, selling investments at a loss to fund your living expenses can permanently deplete your nest egg. Conversely, moving entirely to cash exposes your savings to inflation risk, slowly eroding your purchasing power. You should adopt a balanced approach, often called the bucket strategy. Keep one to two years of living expenses in liquid, safe cash accounts, allocate medium-term needs to bonds, and leave long-term funds in equities to outpace inflation.

Healthcare and Medicare Oversights

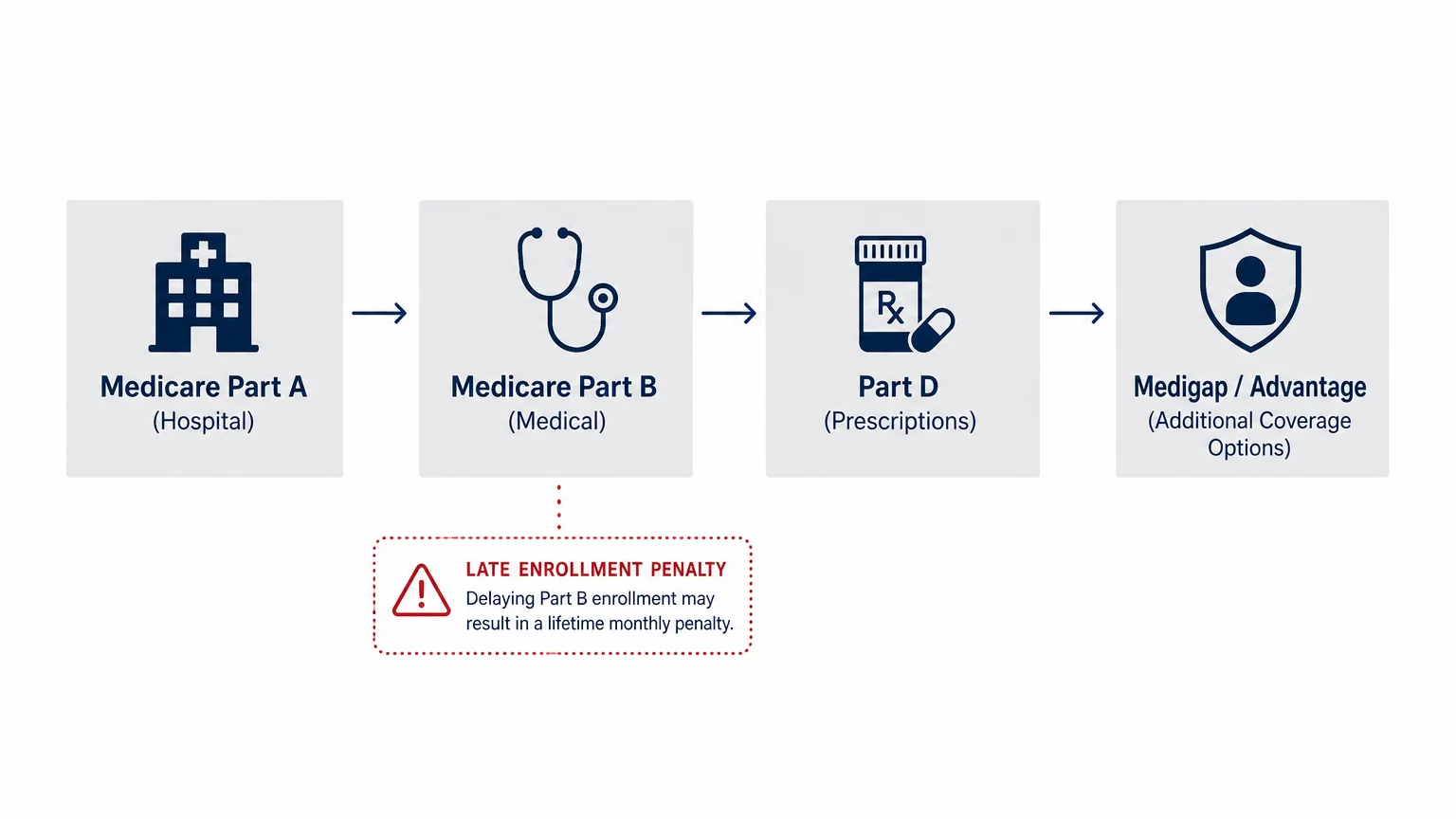

4. Missing Medicare Enrollment Deadlines

Navigating the transition to Medicare requires strict adherence to timelines. Your Initial Enrollment Period (IEP) spans seven months: the three months before your 65th birthday, your birthday month, and the three months following it. Missing this window carries lifelong consequences. Data provided by Medicare.gov outlines that failing to sign up for Medicare Part B when you are first eligible can result in a permanent late enrollment penalty, which adds 10 percent to your monthly premium for every 12-month period you delayed. Set calendar alerts well before your 65th birthday to review your options and complete your enrollment on time.

5. Assuming Traditional Medicare Covers Long-Term Care

A prevalent and dangerous myth among retirees is that traditional Medicare will fund a stay in an assisted living facility or nursing home. In reality, Medicare only covers short-term skilled nursing care following a qualifying hospital stay, typically maxing out at 100 days. It does not cover custodial care—assistance with daily living activities like bathing, dressing, and eating—which makes up the vast majority of long-term care needs. Without a proper strategy, out-of-pocket costs for long-term care can quickly drain a lifetime of savings. You should proactively research long-term care insurance, explore hybrid life insurance policies, or consult an elder law attorney regarding Medicaid planning long before you actually need care.

6. Skipping Regular Health Screenings

Retirement provides the perfect opportunity to prioritize preventative healthcare, yet many seniors neglect routine screenings once they step away from employer-mandated health programs. Catching conditions like hypertension, diabetes, or early-stage cancers drastically improves your treatment options and overall quality of life. Make full use of the preventive services covered by your health plan. Medicare fully covers an initial “Welcome to Medicare” visit as well as Annual Wellness Visits. These appointments give you and your doctor dedicated time to develop a personalized prevention plan, review your current medications, and schedule necessary screenings such as bone density tests, colonoscopies, and vital vaccinations.

Lifestyle and Social Isolation Pitfalls

7. Losing Your Sense of Purpose

Leaving the workforce can trigger an unexpected psychological challenge known as retirement shock. For decades, your career likely dictated your schedule, provided your social circle, and anchored your identity. Waking up on a Monday morning with absolutely nothing required of you sounds idyllic, but a complete lack of structure often leads to depression and listlessness. To combat this, treat retirement as a time of reinvention. Structure your days with intention. Volunteer for a local charity, mentor young professionals in your former industry, or dedicate serious time to a passion project. Having a reason to get out of bed every morning is essential for your mental well-being.

8. Letting Social Connections Fade

Isolation is a silent threat to seniors. The casual conversations at the office water cooler and the daily interactions with colleagues vanish once you retire. Without deliberate effort, your social circle can shrink rapidly. Research from the National Institute on Aging (NIA) shows that social isolation and loneliness are linked to higher risks for a variety of physical and mental conditions, including high blood pressure, heart disease, obesity, a weakened immune system, and cognitive decline. You must treat socializing as a vital part of your health regimen. Join local clubs, participate in community center activities, schedule weekly lunches with friends, and actively nurture relationships with your family members.

9. Adopting a Sedentary Routine

The temptation to spend hours relaxing in your favorite armchair is strong, but a sedentary lifestyle accelerates muscle loss, decreases bone density, and drastically increases your risk of falling. Preserving your mobility dictates your independence in later years. You do not need to become a marathon runner; simply incorporating regular, low-impact movement into your daily routine yields massive benefits. Engage in brisk walking, swimming, gardening, or tai chi to maintain your cardiovascular health and preserve your balance. Aim for at least 30 minutes of intentional movement most days of the week.

Housing Decisions and Family Boundaries

10. Upsizing or Relocating Without a Trial Run

The dream of moving to a coastal town or purchasing a massive home to host grandchildren frequently collides with the reality of high taxes, unexpected isolation, and exhausting upkeep. Before you sell your current home and sever ties with your established community, test the waters. A trial run gives you an honest perspective on the day-to-day lifestyle, the local healthcare facilities, and the actual cost of living in a new area.

| Approach | Financial Impact | Emotional Impact | Flexibility |

|---|---|---|---|

| Impulse Move | High risk. Closing costs, moving fees, and real estate commissions can drain tens of thousands of dollars if you change your mind. | Potentially high stress. You might feel trapped in an unfamiliar area away from friends and established doctors. | Low. Once you buy a home, you are anchored to that location until you can sell it. |

| Trial Run (Renting for 6 Months) | Low risk. Renting allows you to retain your primary savings and assess true living costs. | Low stress. You experience the lifestyle with the safety net of knowing you can return home. | High. You can easily pivot to a different neighborhood or state at the end of the lease. |

11. Becoming the Family Bank

Your desire to help your adult children or grandchildren is completely natural, but sacrificing your own financial security to do so is a critical mistake. Whether it is co-signing a mortgage, funding a lavish wedding, or repeatedly paying off a relative’s credit card debt, these actions compromise the capital you need to survive. There are loans available for college and mortgages available for homes; there are no loans available to fund your retirement. Establish firm financial boundaries with your family. Explain that preserving your own financial independence is ultimately the greatest gift you can give them, as it ensures you will not become a financial burden on them later in life.

12. Holding Onto a High-Maintenance Property

Staying in the family home out of pure sentimentality can trap you in a cycle of endless maintenance and rising property taxes. A two-story home with steep stairs, a large yard, and aging plumbing demands both physical stamina and continuous cash injections. Routine maintenance typically costs between one and four percent of a home’s value every single year. You should assess your home through the lens of aging in place. Are the hallways wide enough for mobility aids? Is there a full bathroom and bedroom on the first floor? If outfitting the home for your senior years is cost-prohibitive, downsizing to a smaller, single-story home or a low-maintenance condo is a practical move.

Scams and Security Vulnerabilities

13. Ignoring Fraud and Phishing Threats

Seniors are disproportionately targeted by sophisticated financial scams, ranging from romance fraud and tech support schemes to urgent calls impersonating a grandchild in distress. The tactics used by fraudsters continually evolve, particularly with the advent of artificial intelligence capable of cloning voices. The Consumer Financial Protection Bureau (CFPB) warns that scammers rely on creating a false sense of urgency to bypass your rational decision-making. Protect yourself by establishing a family safe word, never providing remote access to your computer to an unsolicited caller, and freezing your credit files at the three major bureaus. If an offer sounds too good to be true or a demand for payment requires gift cards or cryptocurrency, it is a scam.

14. Skipping Estate Planning Updates

Creating a will or a trust two decades ago and never looking at it again is a recipe for family conflict. Major life events—such as divorces, the birth of grandchildren, or the passing of a designated executor—render old documents obsolete. Furthermore, many people forget that beneficiary designations on retirement accounts and life insurance policies completely override instructions in a will. Review your estate plan every three to five years. Verify that your powers of attorney for both healthcare and finances are up to date, ensuring a trusted individual can make decisions on your behalf if you become incapacitated.

15. Leaving Digital Legacies Unmanaged

In our modern era, your legacy exists online just as much as it does in physical filing cabinets. You likely possess dozens of online accounts, ranging from banking portals and investment platforms to social media profiles and digital photo storage. If you pass away or experience severe cognitive decline without leaving a clear digital roadmap, your family will face an administrative nightmare attempting to locate and access these assets. Utilize a secure password manager to store your login credentials. Draft a digital estate plan that names a digital executor, providing them with the necessary master passwords and explicit instructions on how to handle or close your online presence.

Frequently Asked Questions

Can I work part-time without losing my Social Security benefits?

Yes, you can work while receiving Social Security, but if you have not yet reached your full retirement age, your earnings are subject to an annual limit. If you earn more than this specific limit, the government will temporarily withhold a portion of your benefits. However, once you reach your full retirement age, you can earn as much as you want without any reduction to your monthly Social Security payments.

How much of my portfolio should I withdraw each year?

A common guideline is the 4 percent rule, which suggests withdrawing 4 percent of your total portfolio value in your first year of retirement and adjusting that amount for inflation annually. However, this is just a baseline. Your actual withdrawal rate should adapt to market conditions, your life expectancy, and your other sources of guaranteed income. Working with a fiduciary advisor helps tailor a withdrawal strategy specifically for your portfolio.

What happens if I miss my Medicare Initial Enrollment Period?

If you miss your Initial Enrollment Period, you will generally have to wait for the General Enrollment Period, which runs from January 1 to March 31 each year, with coverage beginning the month after you sign up. Most importantly, missing your initial window usually means you will incur permanent late enrollment penalties for Part B, significantly increasing your monthly healthcare costs for the rest of your life.

Should I pay off my mortgage before retiring?

Entering retirement without a mortgage drastically reduces your required monthly cash flow, providing immense peace of mind and shielding you from sequence of returns risk. However, you should not drain your liquid savings or trigger massive tax hits from IRA withdrawals just to pay off a low-interest mortgage. Evaluate your overall liquidity and the interest rate of your loan before making a large lump-sum payoff.

For additional senior resources, visit

Social Security Administration (SSA), Consumer Financial Protection Bureau (CFPB) and Administration for Community Living (ACL).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply