Paying for necessary medications should never mean sacrificing your grocery budget or skipping utility bills. Yet, millions of older adults face overwhelming pharmacy costs every month, entirely unaware that substantial savings programs already exist. You can dramatically reduce your out-of-pocket healthcare expenses by tapping into hidden prescription discounts designed specifically for seniors on fixed incomes. From manufacturer assistance programs to federal subsidies and specialized pharmacy networks, these resources remain severely underutilized simply because people do not know where to look. By learning how to access these ten proven discount strategies, you can take control of your healthcare finances, keep more money in your wallet, and ensure you never have to ration another vital prescription.

Understanding the Cost Burden on Fixed Incomes

Retirement often brings an unexpected financial shock at the pharmacy counter. As you age, you naturally require more maintenance medications to manage chronic conditions like high blood pressure, diabetes, or arthritis. Relying on a fixed income makes it incredibly difficult to absorb sudden price hikes or changes in your insurance formulary—the list of drugs your plan covers.

Many older adults quietly struggle with “polypharmacy,” the medical term for taking multiple prescription medications daily. The compounding copays, deductibles, and out-of-pocket gaps can quickly drain your retirement savings. Worse, financial strain pushes some seniors to skip doses or cut pills in half, directly jeopardizing their health and independence. You do not have to settle for this stressful reality. The healthcare system is complicated, but learning to navigate its discount structures will protect both your physical health and your bank account.

1. Manufacturer Patient Assistance Programs (PAPs)

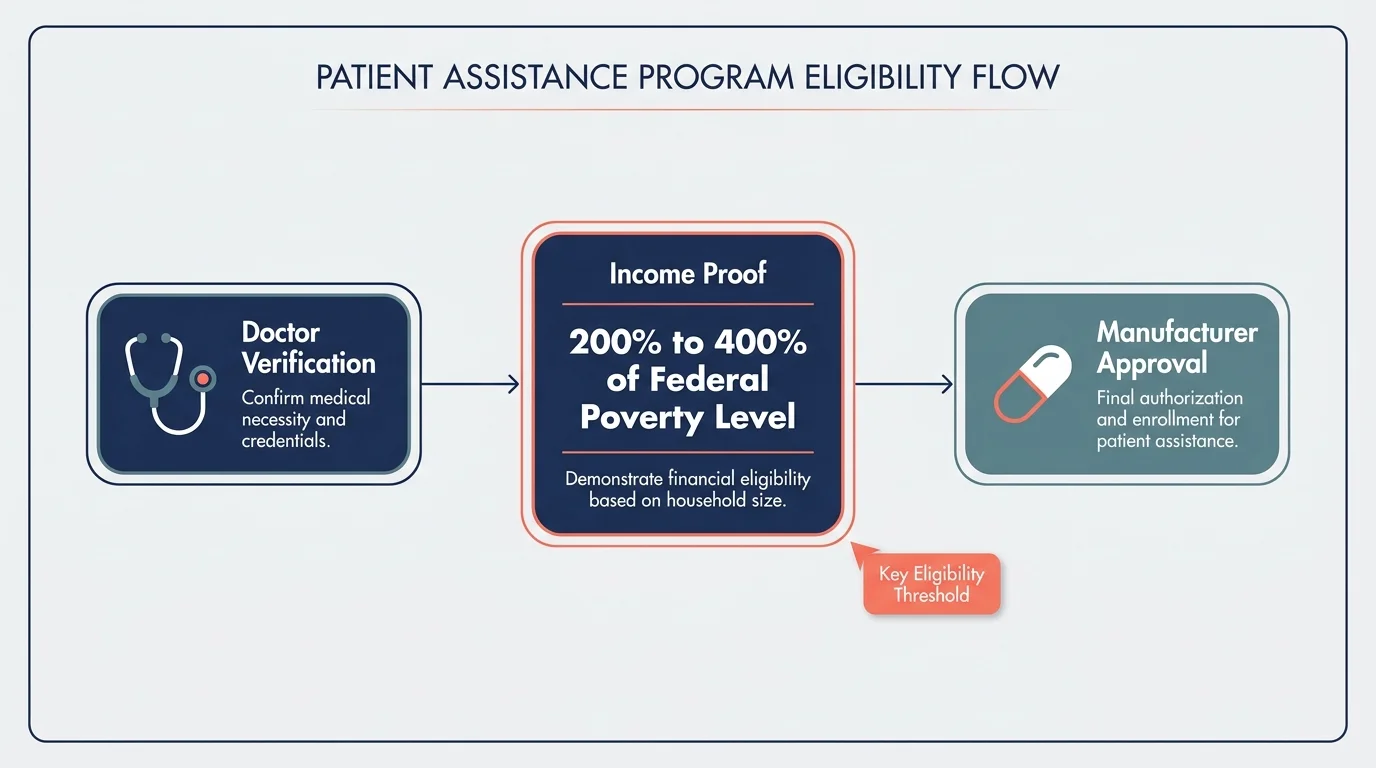

Pharmaceutical companies routinely offer Patient Assistance Programs (PAPs) to help individuals who cannot afford their brand-name medications. These programs provide medications for free or at a drastically reduced cost directly from the manufacturer. PAPs are especially valuable for expensive specialty drugs that lack generic alternatives.

To qualify, you typically need to prove your income falls below a certain threshold—often between 200% and 400% of the Federal Poverty Level. Your doctor will also need to sign a portion of the application verifying your prescription. Search for the specific brand name of your medication online alongside the phrase “patient assistance program” to find the official manufacturer’s application. Many seniors assume they make too much money to qualify, but the income limits are surprisingly generous, making this a highly underused resource.

2. Pharmacy Discount Cards and Apps

Independent discount networks negotiate bulk pricing directly with pharmacies, passing the savings on to consumers through free discount cards and mobile apps. You present these digital or physical cards to your pharmacist instead of your traditional insurance card. In many cases, the cash price negotiated by the discount card is significantly lower than your Medicare Part D copay.

You cannot combine a discount card with your Medicare insurance on a single transaction. You must choose one or the other. Ask your pharmacist to run the price through your insurance, and then ask them to check the price using the discount card. Choose whichever option leaves more money in your pocket. Keep in mind that purchases made with a discount card generally do not count toward your Medicare deductible or out-of-pocket maximum limits.

3. The Medicare Extra Help Program

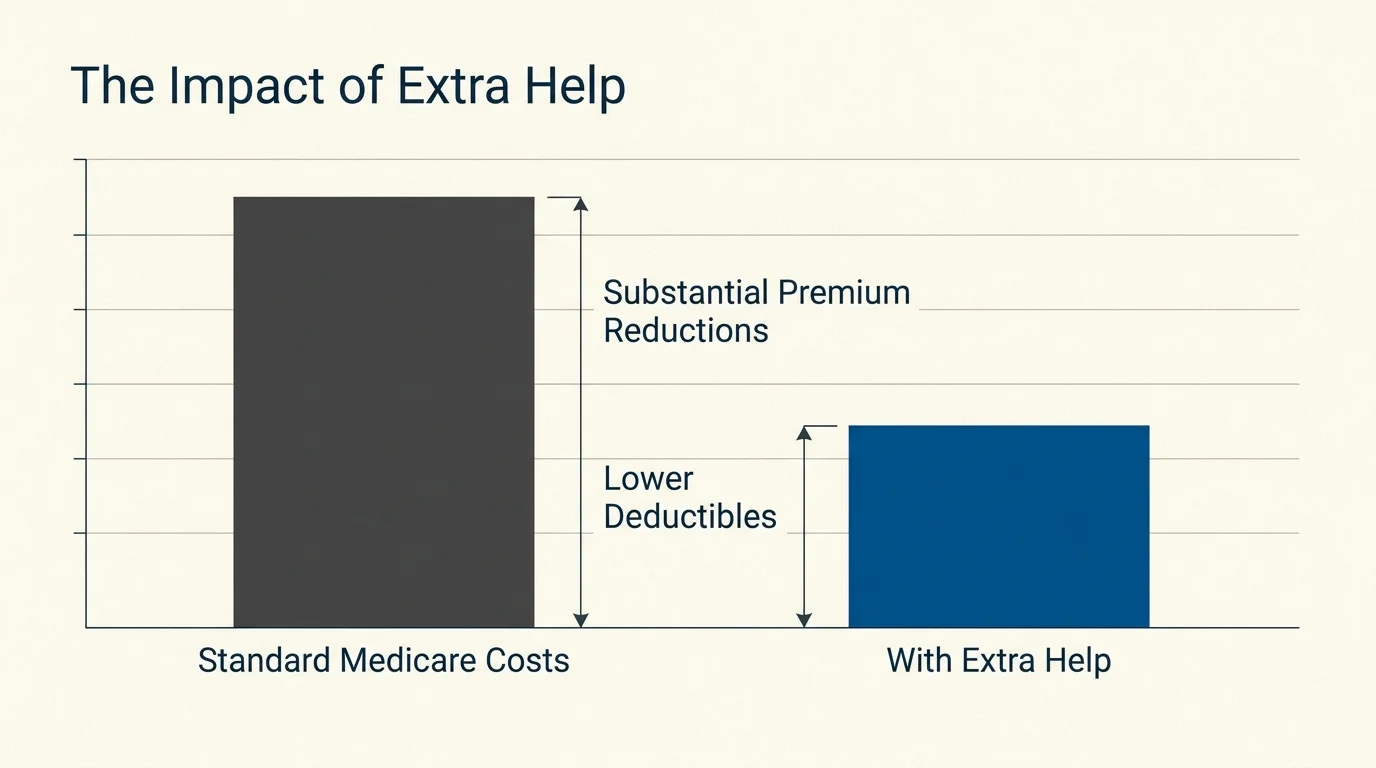

The federal government offers a Low-Income Subsidy, universally known as Extra Help, to assist Medicare beneficiaries with paying their Part D premiums, deductibles, and coinsurance. If you qualify, this program severely caps the amount you pay for both generic and brand-name medications. According to the Social Security Administration (SSA), the Extra Help program is estimated to be worth about $5,300 per year to the average senior who qualifies.

Recent changes to the law expanded eligibility, meaning more seniors qualify now than ever before. Even if you were denied in the past, your current income and asset levels might now meet the threshold. Applying is straightforward, entirely free, and can be completed online or over the phone. Securing Extra Help also eliminates the Medicare Part D late enrollment penalty if you delayed signing up for coverage.

4. State Pharmaceutical Assistance Programs (SPAPs)

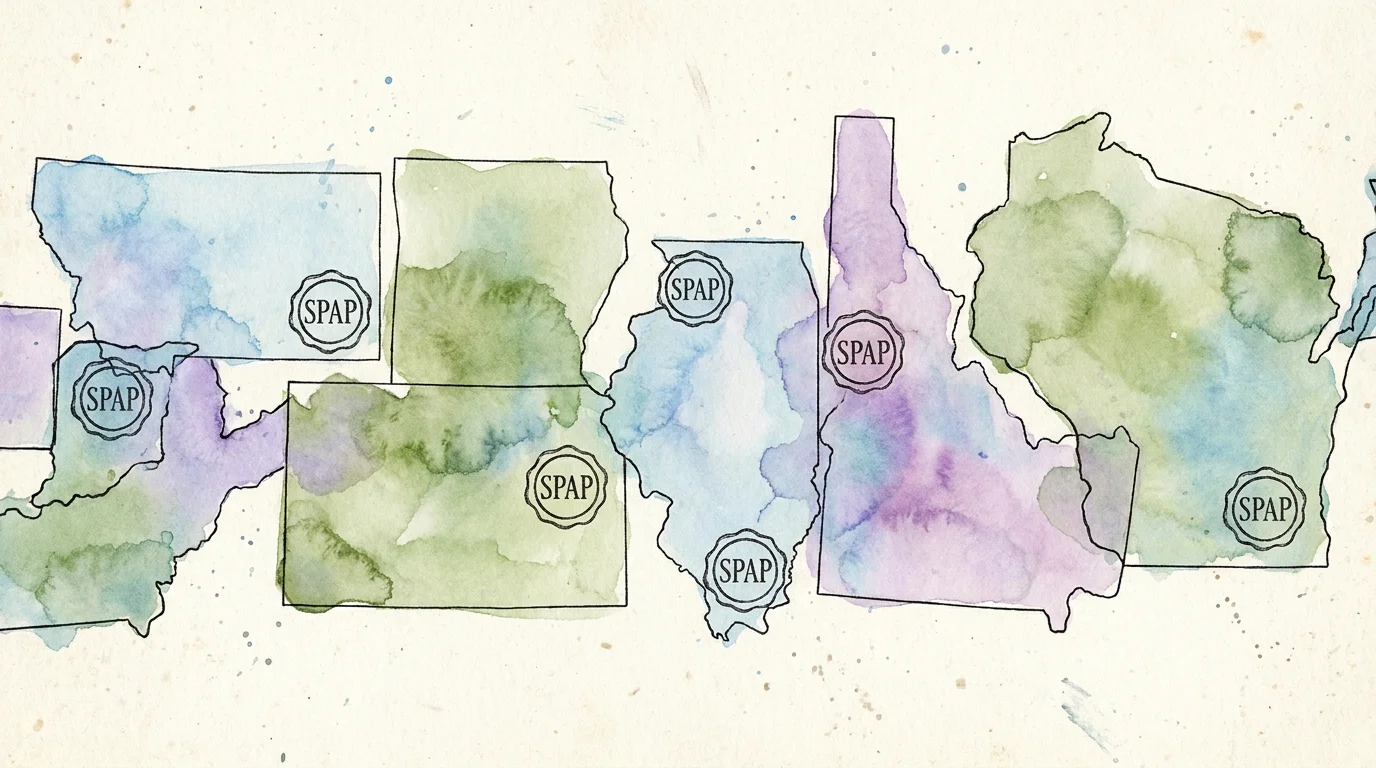

Many state governments fund their own assistance programs to help older adults and adults with disabilities pay for prescription drugs. These State Pharmaceutical Assistance Programs (SPAPs) act as secondary coverage, wrapping around your primary Medicare Part D plan to pay the remaining out-of-pocket costs at the pharmacy counter.

Each state establishes its own rules, income limits, and application procedures. Some states cover a broad range of medications, while others focus on treatments for specific chronic illnesses like HIV/AIDS or end-stage renal disease. Resources at Medicare.gov offer tools and directories to help you find out if your state currently funds an active SPAP and how to submit your application.

5. Preferred Pharmacy Networks

Medicare Part D and Medicare Advantage plans divide pharmacies into different pricing tiers: preferred, standard, and out-of-network. Seniors frequently overpay simply because they fill their prescriptions at a convenient standard pharmacy rather than a preferred one located just a mile down the road.

Insurance companies negotiate much deeper discounts with their preferred network. A generic medication that costs $15 at a standard in-network pharmacy might cost exactly $0 at a preferred pharmacy. Review your plan’s annual documentation to identify which major chains or local independent drugstores hold preferred status. Transferring your active prescriptions to a preferred location requires just one phone call to the new pharmacy, and they will handle the transition for you.

6. Mail-Order Pharmacy Savings

If you take daily maintenance medications for conditions like cholesterol, thyroid imbalances, or high blood pressure, transitioning to a mail-order pharmacy can yield massive savings. Insurance companies highly incentivize mail-order services because they reduce administrative costs.

Instead of driving to the store every 30 days, your insurance plan’s mail-order service will ship a 90-day supply directly to your front door. Plans often charge you for only two months’ worth of copays while delivering a three-month supply, effectively giving you one month free. Beyond the financial discount, mail delivery eliminates transportation barriers, prevents missed refills, and guarantees you always have an adequate supply of necessary treatments on hand.

7. The $35 Insulin Cap and Free Vaccines

Recent federal legislation fundamentally changed how Medicare handles vital preventive care and diabetes management. If you use insulin, you no longer have to fear astronomical price spikes. Data from the Centers for Medicare & Medicaid Services (CMS) confirms that all Medicare Part D plans must now cap out-of-pocket costs for a one-month supply of covered insulin at exactly $35.

This cap applies regardless of whether you have met your annual deductible. Additionally, Medicare Part D now covers recommended adult vaccines—including the shingles, RSV, and standard tetanus-diphtheria-whooping cough vaccines—at absolutely no cost to you. If your pharmacist tries to charge you a copay for these specific preventive vaccines, ask them to re-run your Medicare coverage, as the zero-dollar mandate is federal law.

8. Disease-Specific Nonprofits and Grants

Charitable foundations exist specifically to help patients afford the life-saving treatments required for severe or rare chronic illnesses. Organizations operating in this space provide direct financial grants to cover insurance copays, deductibles, and sometimes even travel expenses related to receiving specialized medical care.

Funding depends on private donations, meaning grants open and close throughout the year based on available resources. If you face a diagnosis of cancer, macular degeneration, rheumatoid arthritis, or Parkinson’s disease, search for national foundations dedicated to that exact condition. Medical social workers and clinical navigators at your doctor’s office can often help you submit the required medical documentation to secure these charitable grants.

9. Supermarket and Retail Generic Lists

Several massive grocery chains and big-box retailers maintain independent generic drug discount lists. These programs completely bypass the traditional insurance model. Retailers offer a specific list of common generic medications for a flat rate—often $4 for a 30-day supply or $10 for a 90-day supply.

You do not need an insurance card to access these prices. You simply need a valid prescription from your doctor for a drug included on their promotional list. Because these lists frequently change, you should periodically review the retailer’s website or ask the pharmacy counter for a printed copy of their current low-cost generic offerings. This strategy works flawlessly for common antibiotics, generic heart medications, and standard antidepressants.

10. Veterans Affairs (VA) Prescription Benefits

Veterans often possess access to some of the most comprehensive and affordable prescription coverage available in the United States, yet many hesitate to enroll because they already have Medicare. You can and should utilize both systems to maximize your benefits.

When you enroll in VA healthcare, you are assigned to a priority group based on your military service history, disability rating, and income. This group determines your copay structure. Many veterans receive their medications entirely free, while others face strict, low-cost caps. To use this benefit, your prescriptions must be written or approved by a VA healthcare provider and filled through a VA pharmacy or the VA’s automated mail-order system.

Common Pitfalls to Avoid When Seeking Discounts

While the search for affordable medication provides massive relief, it also exposes seniors to targeted scams and restrictive fine print. Bad actors constantly attempt to exploit older adults who feel desperate to lower their healthcare costs.

- Paying for Discount Cards: Legitimate pharmacy discount cards are entirely free. You should never pay a membership fee, a monthly subscription, or an upfront activation cost to access a prescription discount network. The Consumer Financial Protection Bureau (CFPB) warns against healthcare scams where bad actors demand upfront fees for fake medical discount cards or attempt to steal your banking information under the guise of lowering your premiums.

- Ignoring the Annual Enrollment Period: Medicare Part D plans change their formularies and pricing tiers every single year. A drug that costs $10 this year might jump to $45 next year. Failing to review your coverage during the Annual Enrollment Period (October 15 to December 7) is the fastest way to lose money.

- Buying from Unverified International Pharmacies: Purchasing medications from random overseas websites poses severe health risks. These unregulated sites often sell counterfeit, expired, or chemically altered drugs. Always consult your doctor before sourcing medications outside your standard pharmacy network.

How to Talk to Your Doctor About Lowering Costs

Doctors write prescriptions based on clinical guidelines and efficacy, often entirely unaware of what the drug will cost you at the pharmacy. You must become your own financial advocate inside the examination room. If you feel anxious about bringing up money with your physician, remember that your doctor wants you to take your medication. If you cannot afford it, the treatment fails. Be direct about your financial constraints.

| Question to Ask Your Doctor | Why It Matters for Your Budget |

|---|---|

| “Is there a generic alternative for this medication?” | Generics contain the exact same active ingredients as brand-name drugs but cost up to 85% less. |

| “Can we try ‘step therapy’ first?” | Step therapy involves trying an older, less expensive drug first to see if it works before moving on to newer, costly options. |

| “Do you have any manufacturer samples?” | Pharmaceutical reps leave free samples with clinics. A month of free samples gives you time to sort out assistance applications or secure better coverage. |

| “Can you prescribe a 90-day supply instead of 30?” | Filling a 90-day supply often results in a lower total copay and qualifies you for cheaper mail-order delivery options. |

Frequently Asked Questions

Can I use a pharmacy discount card at the exact same time as my Medicare Part D coverage?

No, you cannot combine them on a single transaction to double your savings. You must ask the pharmacist to process the prescription through your Medicare plan, and then calculate the cost using the discount card. You simply choose to pay whichever generated price is lower. If you use the discount card, the money spent usually will not count toward your Medicare deductible.

Do I have to reapply for the Medicare Extra Help program every single year?

In many cases, your Extra Help status automatically renews. However, if your income or assets fluctuate, you may receive a “Notice of Award” or a “Redetermination” letter in the mail during late summer. If you receive a redetermination form, you must fill it out and return it promptly to prove you still meet the financial requirements, otherwise, you will lose your subsidy on January 1st.

What happens if my necessary medication is suddenly removed from my plan’s formulary?

If your plan drops your drug, you do not immediately have to pay full price. You have the right to request a “formulary exception.” This requires your prescribing doctor to submit a statement to your insurance company explaining that the specific drug is medically necessary and that alternative drugs on the formulary would be ineffective or cause adverse side effects.

Are generic medications truly as safe and effective as expensive brand-name drugs?

Yes. The federal government heavily regulates generic drug production. Research supported by the National Institutes of Health (NIH) confirms that generic drugs work in the exact same way and provide the same clinical benefits as their brand-name counterparts. They must prove bioequivalence, meaning they deliver the same amount of active ingredient into your bloodstream in the same amount of time.

Is it safe to use mail-order pharmacies if I live in a region with extreme hot or cold weather?

Yes. Accredited mail-order pharmacies utilize highly advanced shipping protocols. For medications sensitive to temperature, such as insulin or certain biological injections, pharmacies use specialized insulated packaging, cooling packs, and expedited overnight shipping to ensure the integrity of the medication is maintained from the facility directly to your doorstep.

For additional senior resources, visit AARP, Alzheimer’s Association and American Heart Association.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply