Navigating retirement expenses becomes much easier when you claim the specific financial and health benefits designed for your generation. If you were born between 1941 and 1969, you qualify for federal, state, and private assistance programs that significantly lower your monthly costs. Many older adults unknowingly leave thousands of dollars on the table because they never apply for their rightful perks. From utility subsidies and property tax exemptions to enhanced medical coverage and everyday discounts, discovering these resources protects your fixed income. Securing these benefits requires a proactive approach, but the financial relief is well worth your time. Review these ten essential programs to ensure you receive exactly what you deserve.

Understanding Your Eligibility Based on Birth Year

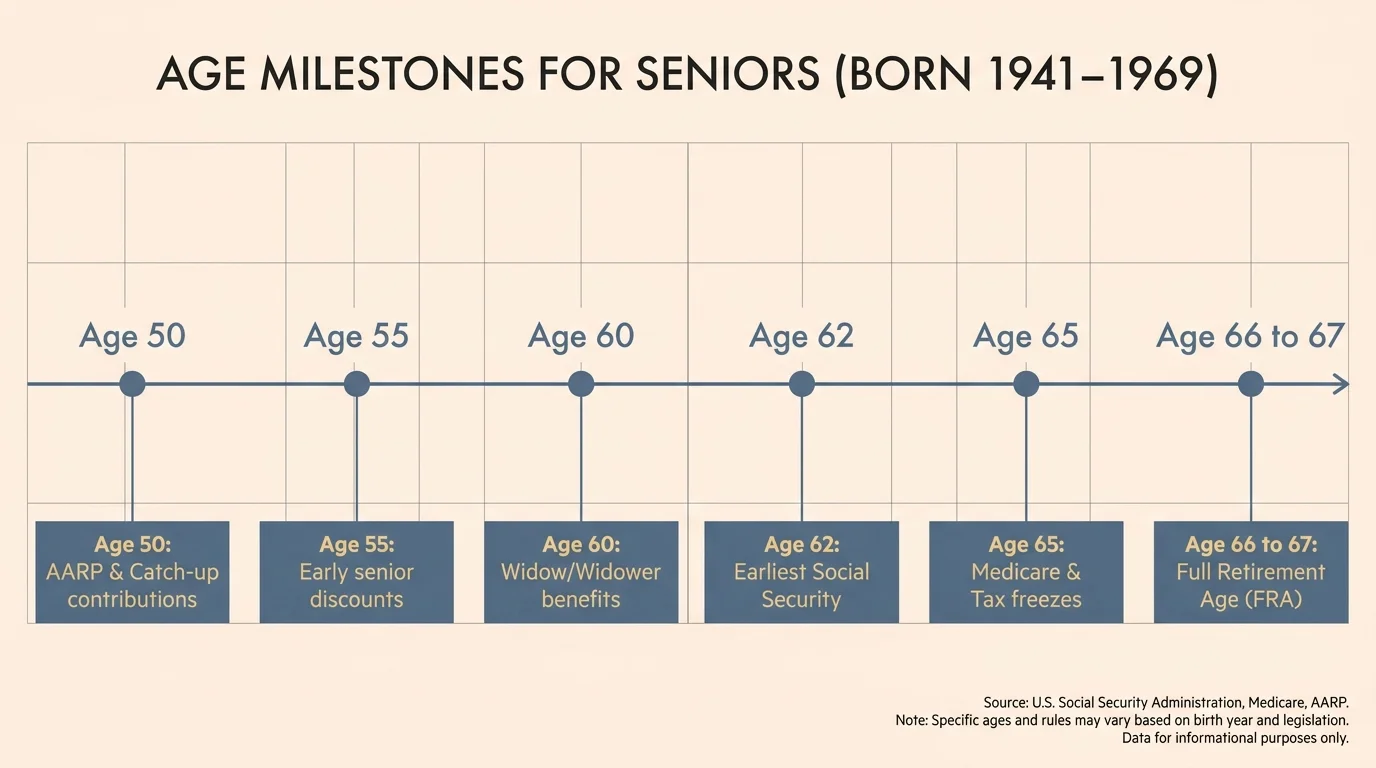

Because the timeframe between 1941 and 1969 spans almost three decades, your birth year dictates exactly which programs you can access today. Some benefits unlock at age 50, while others require you to reach your full retirement age. Knowing your specific timeline prevents you from missing crucial enrollment windows that could cost you money in penalties or lost coverage.

Tracking benefits by birth year simplifies your retirement planning. Rather than guessing when to apply for various programs, you can map out a timeline that aligns with your exact age. Below is a breakdown of major age milestones and the benefits that become available to you at each stage.

| Age Milestone | Benefit Eligibility Trigger |

|---|---|

| Age 50 | AARP membership eligibility; catch-up contributions for retirement accounts begin. |

| Age 55 | Access to early senior discounts; eligibility for specific senior living communities. |

| Age 60 | Widow or widower Social Security benefits unlock. |

| Age 62 | Earliest eligibility to claim personal Social Security retirement benefits. |

| Age 65 | Medicare eligibility begins; standard age for property tax freezes in many states. |

| Age 66 to 67 | Full Retirement Age (FRA) for Social Security, depending on your exact birth year. |

1. Maximize Your Social Security Returns

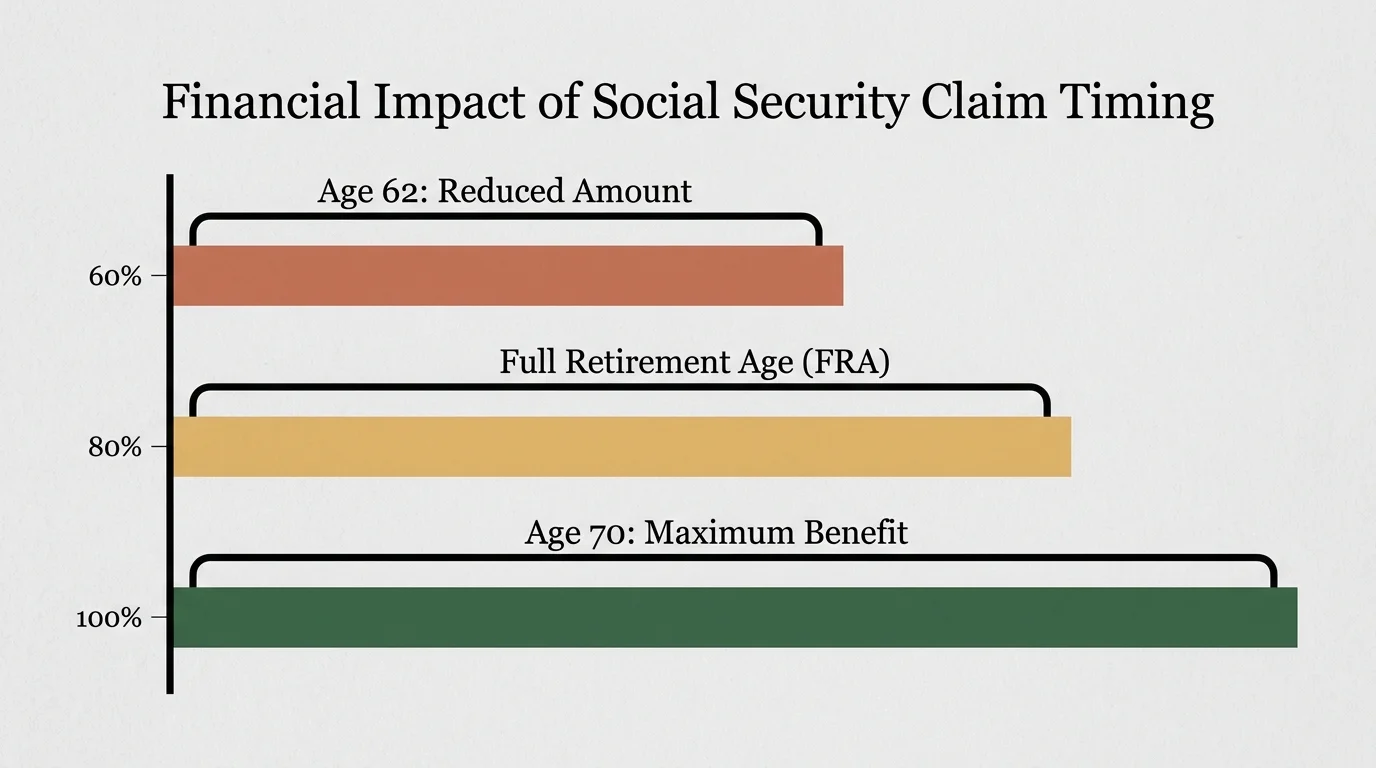

Your Social Security benefit serves as the foundation of your retirement income. However, the age at which you choose to start collecting dramatically impacts your monthly check for the rest of your life. If you were born between 1941 and 1969, you face a critical decision: claim early at 62 for a reduced amount, wait until your Full Retirement Age (FRA), or delay claiming to maximize your payout.

According to the Social Security Administration (SSA), delaying your claim beyond your Full Retirement Age increases your benefit by 8% for every year you wait, up until age 70. This guaranteed return easily outperforms most conventional investments. If you claim at age 62, you could face a permanent reduction of up to 30% on your monthly payments.

Consider your health status, life expectancy, and current financial needs before claiming. If you plan to continue working, claiming early might trigger the earnings test, which temporarily withholds some of your benefits. You should create an online account on the SSA website to review your personalized statements and calculate the exact difference between claiming early and waiting.

2. Unlock Essential Health Savings With Medicare Allowances

Healthcare costs consistently rank as the highest expense for older adults. Once you turn 65, Medicare provides substantial coverage, but standard premiums and out-of-pocket costs still strain fixed budgets. Fortunately, numerous supplemental programs exist to absorb these financial blows.

Medicare Savings Programs (MSPs) help pay your Part A and Part B premiums, deductibles, coinsurance, and copayments if you meet certain income and resource limits. Furthermore, the Extra Help program specifically lowers the cost of prescription drugs under Medicare Part D. Qualifying for Extra Help can save you thousands of dollars annually on vital medications.

Many seniors fail to apply for these programs because they assume their income is too high. However, income limits adjust annually, and certain deductions apply. As noted by experts at Medicare.gov, you should actively review your eligibility for Extra Help and MSPs every year during the Open Enrollment period, as subtle shifts in your financial situation might suddenly qualify you for massive savings.

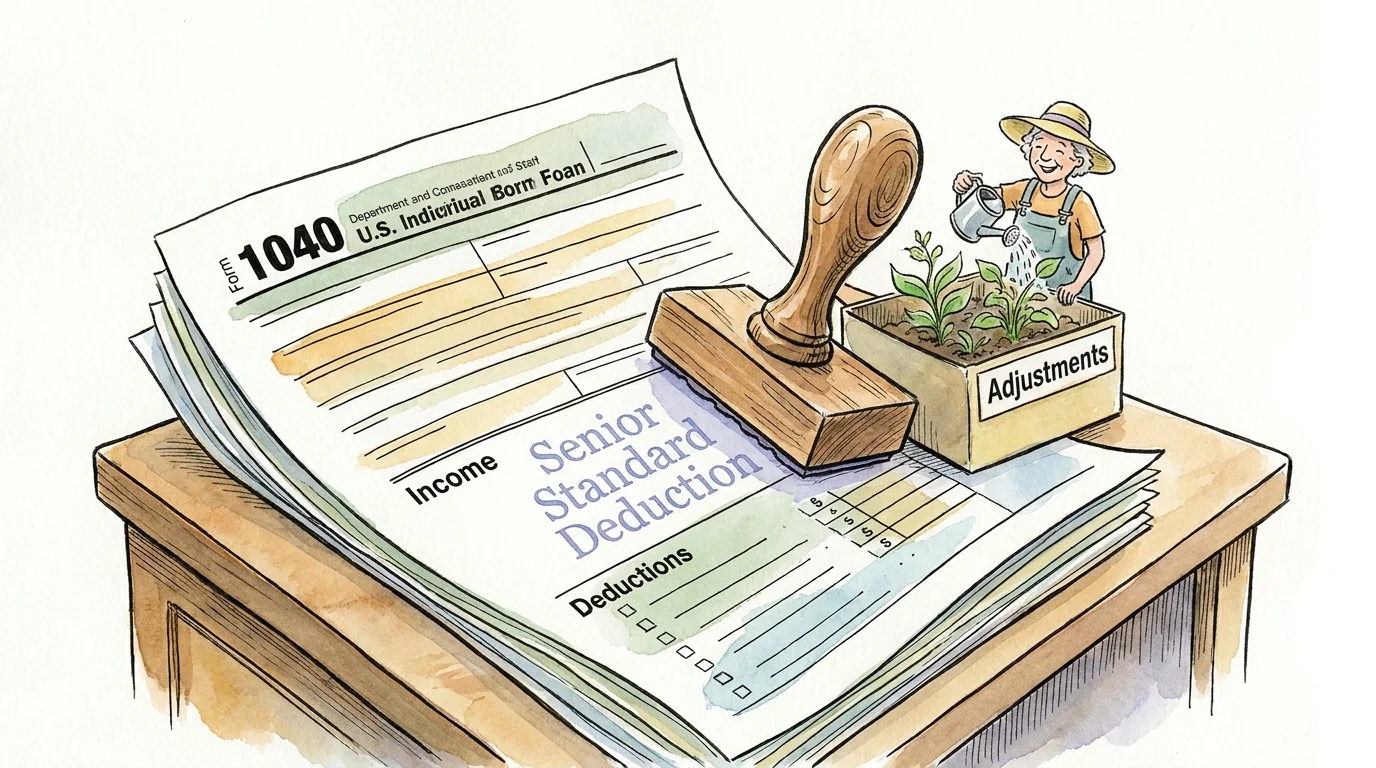

3. Reduce Tax Burdens With the Senior Standard Deduction

Filing taxes changes significantly as you age. The IRS offers a higher standard deduction for individuals who are 65 or older by the end of the tax year. This simple benefit directly reduces your taxable income, leaving more money in your bank account.

If you use commercial tax preparation software, ensure you check the specific box confirming your age. Many people rush through their filings and rely on the software’s defaults, inadvertently claiming the standard deduction for younger adults. If you are legally blind, the IRS provides an additional deduction amount, which you can stack on top of the age-based increase.

Beyond the federal level, investigate your state tax codes. Many states do not tax Social Security income, and several offer specific retirement income exclusions for pensions and 401(k) distributions. Taking advantage of these provisions minimizes the amount of your retirement savings going back to the government.

4. Slash Property Taxes Through Local Exemption Programs

Rising property values often lead to surging property taxes, which create severe hardships for seniors living on a fixed income. To prevent older adults from being priced out of their long-time homes, most local governments offer significant property tax relief programs. These benefits for seniors usually fall into two categories: homestead exemptions and senior freezes.

- Senior Exemptions: This program reduces the assessed value of your home, which directly lowers your tax bill.

- Tax Freezes: This locks in your property’s assessed value at a specific baseline once you reach a certain age (often 65), preventing future tax hikes even if the neighborhood’s market value skyrockits.

- Circuit Breakers: These state-funded programs provide a refund or tax credit if your property taxes exceed a certain percentage of your annual income.

Because property taxes are handled at the county or municipal level, you must apply directly through your local tax assessor’s office. Pay close attention to deadlines, as most jurisdictions require you to submit your application by early spring to receive the exemption for the current tax year.

5. Cut Utility Bills With Energy Assistance Programs

Heating your home in the winter and cooling it during the summer requires substantial energy. If you find your utility bills overwhelming, the Low Income Home Energy Assistance Program (LIHEAP) offers crucial financial support. This federally funded program issues grants directly to your utility providers, immediately lowering your outstanding balances.

LIHEAP also funds the Weatherization Assistance Program (WAP). Instead of just paying your bills, weatherization tackles the root cause of high energy costs by improving your home’s energy efficiency. Eligible seniors receive free home upgrades, including enhanced insulation, weatherstripping, and even repairs or replacements for failing HVAC systems.

You apply for both LIHEAP and weatherization through your state or local community action agency. Priority is often given to households with individuals over the age of 60. Gather your recent utility bills, proof of income, and identification documents before calling your local office to initiate the application process.

6. Access Nutritious Meals Through Senior Food Assistance

Good nutrition forms the bedrock of healthy aging, yet the rising cost of groceries forces many older adults to make difficult choices between food and medication. Senior assistance programs bridge this gap, ensuring you have access to fresh, healthy meals without draining your budget.

The Supplemental Nutrition Assistance Program (SNAP) features special rules for seniors. If you are 60 or older, you can deduct out-of-pocket medical expenses exceeding $35 a month from your gross income. This medical deduction often qualifies seniors for a significantly higher monthly SNAP allotment. Do not ignore this calculation, as it makes a tremendous difference in your grocery budget.

Additionally, community-based meal programs offer both nutrition and socialization. Research from the Administration for Community Living (ACL) emphasizes the importance of these initiatives, which fund local Congregate Meal programs at senior centers and home-delivered meals (like Meals on Wheels) for homebound individuals. These services operate on a sliding scale or request voluntary donations, meaning you never have to skip a meal due to financial constraints.

7. Secure Discounts on Travel and Public Transit

Retirement provides the perfect opportunity to travel, visit family, and explore your community. Fortunately, your birth year unlocks a massive array of discounts designed to make transportation highly affordable.

If you enjoy the outdoors, purchasing the America the Beautiful Senior Pass is one of the best retirement perks available. For a small one-time fee, citizens aged 62 and older receive lifetime access to thousands of federal recreation sites and national parks. The pass also provides a 50% discount on select amenity fees, such as camping and boat launching.

Closer to home, explore your local public transit authority. Almost all bus, subway, and commuter rail systems offer a reduced fare program for individuals over 65, often cutting ticket prices in half. Furthermore, if you still drive, ask your auto insurance provider about mature driver discounts. Many insurers lower your premiums significantly if you complete an approved defensive driving course.

8. Explore Free Preventive Care and Wellness Programs

Catching health issues early prevents costly medical emergencies later. Medicare covers a robust suite of preventive services at absolutely no cost to you, provided you visit doctors who accept Medicare assignment. Taking advantage of these free screenings protects both your physical health and your wallet.

During your first 12 months on Part B, you qualify for a “Welcome to Medicare” preventive visit. After that first year, you earn a free Annual Wellness Visit to develop or update a personalized prevention plan. These visits are not standard physicals; they focus heavily on assessing cognitive function, establishing baseline health metrics, and reviewing your current medications.

Medicare also fully covers numerous preventive screenings, including bone mass measurements, cardiovascular disease screenings, and various cancer screenings. You also receive full coverage for annual flu shots, pneumococcal vaccines, and COVID-19 vaccines. Always ask your provider to confirm that a recommended test falls under Medicare’s preventive care umbrella to ensure you owe nothing out of pocket.

9. Protect Your Wealth From Common Senior Scams

Securing your benefits only matters if you can protect them from those trying to steal them. Seniors born between 1941 and 1969 frequently find themselves targeted by sophisticated financial scams. Criminals use fear, urgency, and confusion to drain retirement accounts and steal identities.

Be highly suspicious of unsolicited phone calls claiming to be from the IRS, Medicare, or the Social Security Administration. These agencies communicate primarily through physical mail. A government official will never call you demanding immediate payment over the phone via wire transfer, cryptocurrency, or prepaid gift cards.

According to guidelines from the Consumer Financial Protection Bureau (CFPB), you should routinely monitor your bank statements and credit reports for unauthorized activity. If someone calls offering to help you “unlock” extra Medicare benefits for a fee, hang up immediately. Protect your personal information ruthlessly; treat your Medicare and Social Security numbers with the same security as your bank account passwords.

10. Find Local Support Through the Eldercare Locator

Navigating the sheer volume of available senior benefits often feels overwhelming. You do not have to figure everything out on your own. Every region in the United States operates an Area Agency on Aging (AAA), a public or private non-profit organization designated to address the needs of older adults at the local level.

Your local AAA acts as a central clearinghouse for senior assistance programs. Their trained counselors provide free, unbiased advice on Medicare enrollment, legal assistance, transportation services, and caregiver support. They understand the specific state and county grants available in your exact zip code.

To connect with your local agency, you simply need to use the official Eldercare Locator. By entering your zip code, you instantly receive the contact information for the nearest support center. Scheduling a quick consultation with a local counselor represents the smartest first step in claiming your rightful benefits.

Frequently Asked Questions

Do I automatically receive these benefits when I turn 65?

No. While you become eligible for many programs at age 65, almost none of them enroll you automatically. You must actively apply for Medicare, Social Security, property tax exemptions, and utility assistance. The only exception occurs if you are already receiving Social Security benefits before turning 65, in which case you are automatically enrolled in Medicare Parts A and B.

Can I collect Social Security and still work full-time?

Yes, you can work while receiving Social Security. However, if you claim benefits before your Full Retirement Age (FRA) and earn more than the annual limit, the SSA will temporarily withhold a portion of your monthly check. Once you reach your exact FRA, you can earn any amount of money without any reduction to your benefits.

Are there benefits available if my income is too high for Medicaid?

Absolutely. While Medicaid serves low-income individuals, many other programs target middle-income seniors. Property tax freezes, the Senior Standard Deduction, free Medicare preventive care, and lifetime national park passes do not have strict low-income thresholds. Additionally, Medicare Savings Programs often feature higher income limits than standard Medicaid.

How do I find out which specific programs I qualify for in my state?

The easiest method is to contact your local Area Agency on Aging. You can also use the National Council on Aging’s free online tool, BenefitsCheckUp. By answering a few anonymous questions about your age, location, and income, you will receive a customized report listing every federal, state, and local program you qualify for.

Will claiming benefits early permanently reduce my monthly payments?

When it comes to Social Security, yes. Claiming your retirement benefits at age 62 locks in a permanent reduction compared to waiting for your Full Retirement Age. However, claiming other benefits early—such as senior travel discounts or utility assistance—has no negative impact on your future finances.

For additional senior resources, visit

Medicare.gov, National Institute of Mental Health (NIMH), National Institutes of Health (NIH) and Centers for Medicare & Medicaid Services (CMS).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply