Maximizing your retirement income requires more than just checking your pension or 401(k) balance; it involves claiming targeted benefits designed specifically for older adults. You can unlock thousands of dollars in hidden savings each year by leveraging tax credits, healthcare subsidies, and housing exemptions tailored to your age bracket. Many seniors unknowingly leave money on the table simply because they are unaware of the local and federal programs available to them. From utility assistance to property tax freezes, these financial tools protect your nest egg against inflation and rising living costs. By reviewing these ten essential income perks, you can secure your financial foundation, reduce everyday expenses, and enjoy the comfortable retirement you worked decades to achieve.

Social Security Strategies and Spousal Benefits

Your Social Security benefit forms the foundation of your retirement income. However, the system contains multiple nuances that can either enhance or diminish your monthly checks. Understanding how to pull the right levers guarantees you receive every dollar you deserve.

1. Delayed Retirement Credits

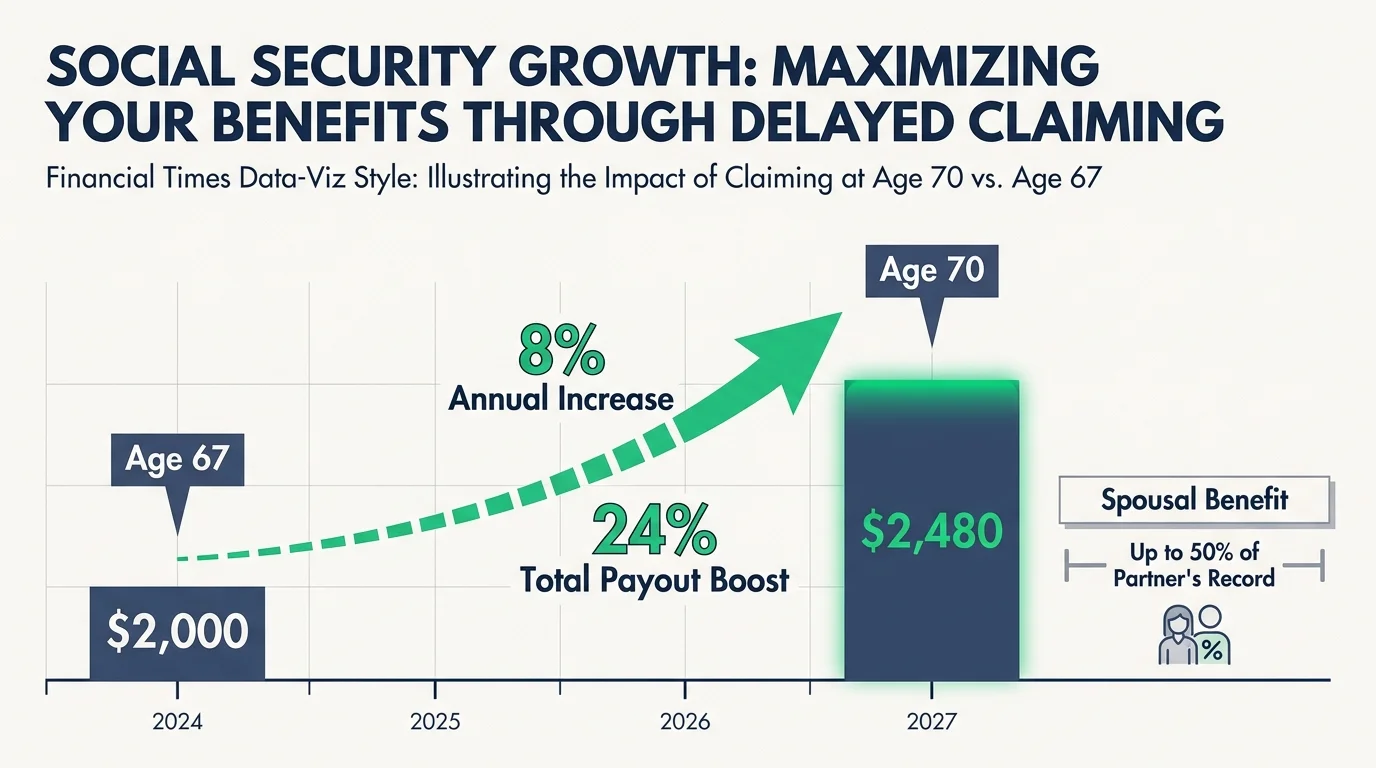

One of the most powerful income perks available to retirees is the delayed retirement credit. You qualify for your standard, unreduced benefit at your Full Retirement Age (FRA), which falls between 66 and 67 depending on your birth year. However, if you wait to claim your benefits after reaching your FRA, your monthly payout increases significantly. According to the Social Security Administration (SSA), delaying your claim increases your monthly benefit by 8% for each full year you wait until you turn 70. For example, if your standard benefit is $2,000 at age 67, waiting until age 70 permanently boosts your monthly check to $2,480. This guaranteed 24% increase serves as an excellent hedge against inflation and ensures higher guaranteed income for the rest of your life.

2. Spousal and Survivor Benefits

Many retirees overlook the hidden value in spousal and survivor benefits. If you are married, divorced, or widowed, you might qualify for benefits based on your partner’s earnings record. A spousal benefit can provide you with up to 50% of your partner’s primary insurance amount, which is incredibly helpful if you spent years out of the workforce raising children or caring for family members. Divorced individuals can also claim this perk if the marriage lasted at least ten years and they remain unmarried. Survivor benefits offer an even greater advantage—widows and widowers can often step up to 100% of their deceased spouse’s benefit amount. Coordinating when and how you and your spouse claim these benefits requires careful timing, but the financial payoff is substantial.

Tax Deductions and Credit Advantages

Taxes do not disappear when you stop working. Fortunately, the tax code recognizes the financial constraints of aging and offers specialized deductions that keep more money in your checking account.

3. The Extra Standard Deduction for Seniors

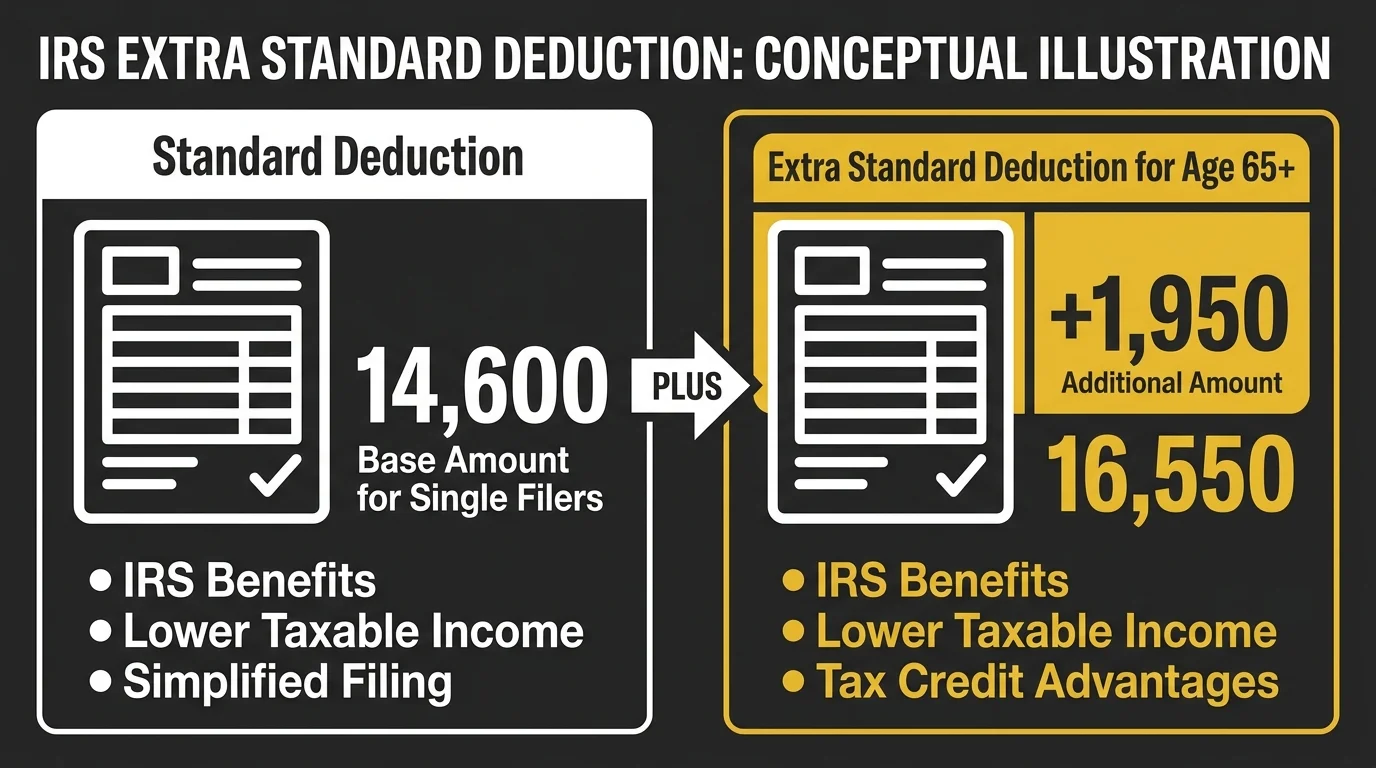

The IRS offers an immediate income perk the moment you turn 65: a larger standard deduction. When you file your annual tax return, you can claim an additional monetary amount on top of the regular standard deduction. If you and your spouse are both over 65 and file jointly, you both get this extra amount, which effectively lowers your taxable income by thousands of dollars before you even begin calculating what you owe. Furthermore, if you are legally blind, the IRS grants you yet another boost to your standard deduction. You must actively ensure your tax software or preparer checks the box for your age, as missing this simple step results in overpaying taxes.

4. State-Level Retirement Income Exemptions

Your geographic location plays a massive role in your retirement tax burden. Many states offer generous exemptions designed specifically to attract and retain retirees. While the federal government taxes up to 85% of your Social Security benefits depending on your combined income, a large majority of states do not tax Social Security at all. Additionally, several states exempt a portion—or even the entirety—of pension income and withdrawals from retirement accounts like IRAs and 401(k)s. When planning your budget, research your specific state’s Department of Revenue rules to see if you qualify for age-based tax exclusions. Structuring your withdrawals to stay within your state’s tax-exempt limits represents a brilliant way to stretch your savings.

Healthcare Subsidies and Medicare Savings Programs

Medical expenses represent one of the largest threats to a fixed income. Fortunately, specific safety nets exist to shield you from exorbitant healthcare costs. Securing these perks drastically lowers your monthly out-of-pocket spending.

5. Medicare Savings Programs (MSPs)

Even with Medicare, premiums, deductibles, and copayments add up quickly. If your income falls below certain thresholds, your state can help pay your Medicare costs through Medicare Savings Programs. These programs function as an incredible financial perk because they put money directly back into your Social Security check by covering your Part B premium. Research and guidelines provided by Medicare.gov indicate that these programs can save beneficiaries thousands of dollars annually. Depending on your income and asset levels, you might qualify for one of the main programs outlined below.

| Program Name | What It Covers | Who It Helps |

|---|---|---|

| Qualified Medicare Beneficiary (QMB) | Part A/B premiums, deductibles, coinsurance, and copayments. | Seniors with very low income and limited resources. |

| Specified Low-Income Medicare Beneficiary (SLMB) | Part B premiums only. | Seniors with low to moderate income. |

| Qualifying Individual (QI) | Part B premiums only (funds are limited and granted on a first-come basis). | Seniors with slightly higher income than SLMB limits. |

6. Extra Help for Prescription Drugs (Part D)

Affording daily medication is a struggle for millions of seniors, but the “Extra Help” program—also known as the Low-Income Subsidy (LIS)—slashes the costs of prescription drugs. If you qualify, this perk covers your Part D monthly premiums, annual deductibles, and prescription copayments. Furthermore, it eliminates the dreaded Medicare coverage gap, commonly known as the “donut hole.” Even if your income is slightly above the strict poverty line, you should still apply, as the program features sliding scale benefits. Securing this subsidy transforms unmanageable pharmacy bills into predictable, affordable copays of just a few dollars per prescription.

Real Estate and Property Tax Exemptions

For many retirees, a home is their most valuable asset. However, rising property values mean rising property taxes. Local governments offer specific income perks to ensure older adults are not priced out of their long-time family homes.

7. Property Tax Freezes and Deferrals

Local municipalities often provide “homestead exemptions” or “senior property tax freezes” to older homeowners. A property tax freeze locks the assessed value of your home at the amount it was worth when you reached a certain age (often 65). Even if your local real estate market skyrockets, your property tax bill remains based on the frozen, lower value. Other jurisdictions offer deferral programs, allowing you to delay paying your property taxes until you sell the home or pass away. To access this perk, you must proactively apply through your county assessor’s office. You must usually provide proof of age, homeownership, and sometimes income verification.

8. Home Modification and Repair Grants

As you age, your physical needs change, and your home must adapt. Modifying a home for accessibility—such as installing a walk-in tub, a wheelchair ramp, or widening doorways—costs thousands of dollars. The federal government, along with many state housing authorities, provides grants and low-interest loans specifically for seniors to handle these repairs. The Section 504 Home Repair program, for example, offers grants to seniors aged 62 and older to remove health and safety hazards from their homes. Because these are grants rather than loans, you do not have to repay the money as long as you remain in the home for a specified period, keeping your emergency savings intact.

Everyday Utility Assistance and Senior Discounts

Small daily expenses chip away at a fixed income just as easily as large bills do. Trimming your regular overhead leaves you with more discretionary money to enjoy life.

9. Utility and Energy Assistance Programs

Heating and cooling costs consume a massive portion of retirement budgets. The Low Income Home Energy Assistance Program (LIHEAP) helps older adults cover the costs of their energy bills. LIHEAP can provide a one-time payment directly to your utility company, preventing service disconnections during extreme summer heat or freezing winter months. Additionally, seniors can leverage the federal Lifeline program, which offers a monthly discount on broadband internet and phone services. The Benefits.gov platform serves as a central hub where you can take an eligibility questionnaire to easily locate these utility assistance programs in your specific ZIP code.

10. Age-Based Memberships and Retail Perks

Never underestimate the power of simply asking, “Do you offer a senior discount?” While it sounds simple, corporate and retail discounts generate significant annual savings. As highlighted by AARP, taking advantage of age-based retail, dining, and travel discounts allows you to maintain an active lifestyle for less. From discounted auto insurance premiums for completing mature driver courses to the America the Beautiful Senior Pass—which grants lifelong access to national parks for a small, one-time fee—these perks encourage you to travel and shop while protecting your wallet.

Common Pitfalls That Drain Retirement Income

Earning and saving money is only half the battle; protecting it from unnecessary losses is equally important. Many retirees inadvertently sabotage their financial stability by falling into predictable traps.

First, failing to plan for Required Minimum Distributions (RMDs) triggers massive tax penalties. Once you reach a certain age (currently 73, though subject to change based on birth year), the IRS mandates that you withdraw a specific percentage from your traditional IRAs and 401(k)s. If you forget to take this withdrawal, the IRS imposes a heavy excise tax on the amount not withdrawn. You must set up automatic calculations and distributions with your brokerage firm to avoid this costly mistake.

Second, overpaying for Medicare supplemental plans drains your monthly budget. Insurance companies frequently change their pricing, and the plan that offered the best value five years ago might now be the most expensive option on the market. Failing to comparison-shop during the annual Medicare Open Enrollment period results in hundreds of dollars lost to premium creep.

Finally, seniors represent the primary target for sophisticated financial scams. Fraudsters use high-pressure tactics, fake tech-support pop-ups, and artificial intelligence voice cloning to steal life savings. The Consumer Financial Protection Bureau (CFPB) advises seniors to carefully evaluate any unsolicited requests for money, never share bank details over the phone, and freeze their credit files to block identity theft. Protecting your information is just as critical as pursuing new income perks.

Frequently Asked Questions

Do I automatically receive the extra standard tax deduction when I turn 65?

No, the IRS does not apply the extra standard deduction automatically. You or your tax preparer must actively select the box on your Form 1040 indicating that you are 65 or older. If you use tax preparation software, you will usually be prompted to answer questions about your age, which will then trigger the software to apply the higher deduction amount.

Can I collect Social Security spousal benefits if I am divorced?

Yes, you can collect benefits based on your ex-spouse’s work record under specific conditions. Your marriage must have lasted for at least ten consecutive years, you must be 62 or older, and you must currently be unmarried. Furthermore, claiming a benefit on your ex-spouse’s record does not reduce the amount they or their current spouse receive.

Will applying for utility assistance affect my Social Security payments?

No, receiving help from programs like the Low Income Home Energy Assistance Program (LIHEAP) or the Lifeline broadband discount does not impact your Social Security benefits. These are entirely separate assistance programs. Government agencies do not count these utility grants as taxable income, meaning they will not cause a reduction in your monthly Social Security checks.

How do I find out what local property tax exemptions I qualify for?

Because property taxes are managed at the local level, you must contact your county or city tax assessor’s office. You can call them directly or visit their official website to search for “senior property tax exemptions” or “homestead exemptions.” They will provide the necessary application forms and inform you of the exact income and age requirements for your specific municipality.

Does Medicare cover the cost of everyday living assistance?

Original Medicare generally does not cover the cost of non-medical everyday living assistance, such as long-term care in a nursing home, help with bathing, or meal delivery. Medicare primarily pays for medically necessary services, hospital stays, and short-term skilled nursing facility care. If you need financial assistance for long-term custodial care, you will need to explore Medicaid, long-term care insurance, or specialized state-funded aging programs.

For additional senior resources, visit

National Institutes of Health (NIH),

Centers for Medicare & Medicaid Services (CMS),

Social Security Administration (SSA) and

Consumer Financial Protection Bureau (CFPB).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply