Providing care for a loved one is a profound act of love, but it brings significant physical, emotional, and financial demands that can quickly deplete your energy and resources. You do not have to carry this heavy responsibility entirely on your own shoulders. Across the country, local, state, and federal programs are designed to offer family caregivers financial relief, respite care, counseling, and practical training. Understanding which options apply to your unique situation is the first step toward securing the assistance you deserve. By exploring these ten dedicated caregiving support programs, you can find the structured help necessary to protect your own health while continuing to deliver the best possible care to your family member.

Federal and State Financial Assistance

Many families mistakenly assume that providing care must mean absorbing all associated costs out of pocket. In reality, multiple government programs exist to help offset the financial burden of keeping a senior loved one at home rather than moving them to a nursing facility. Navigating these systems requires patience, but the financial relief they offer is substantial.

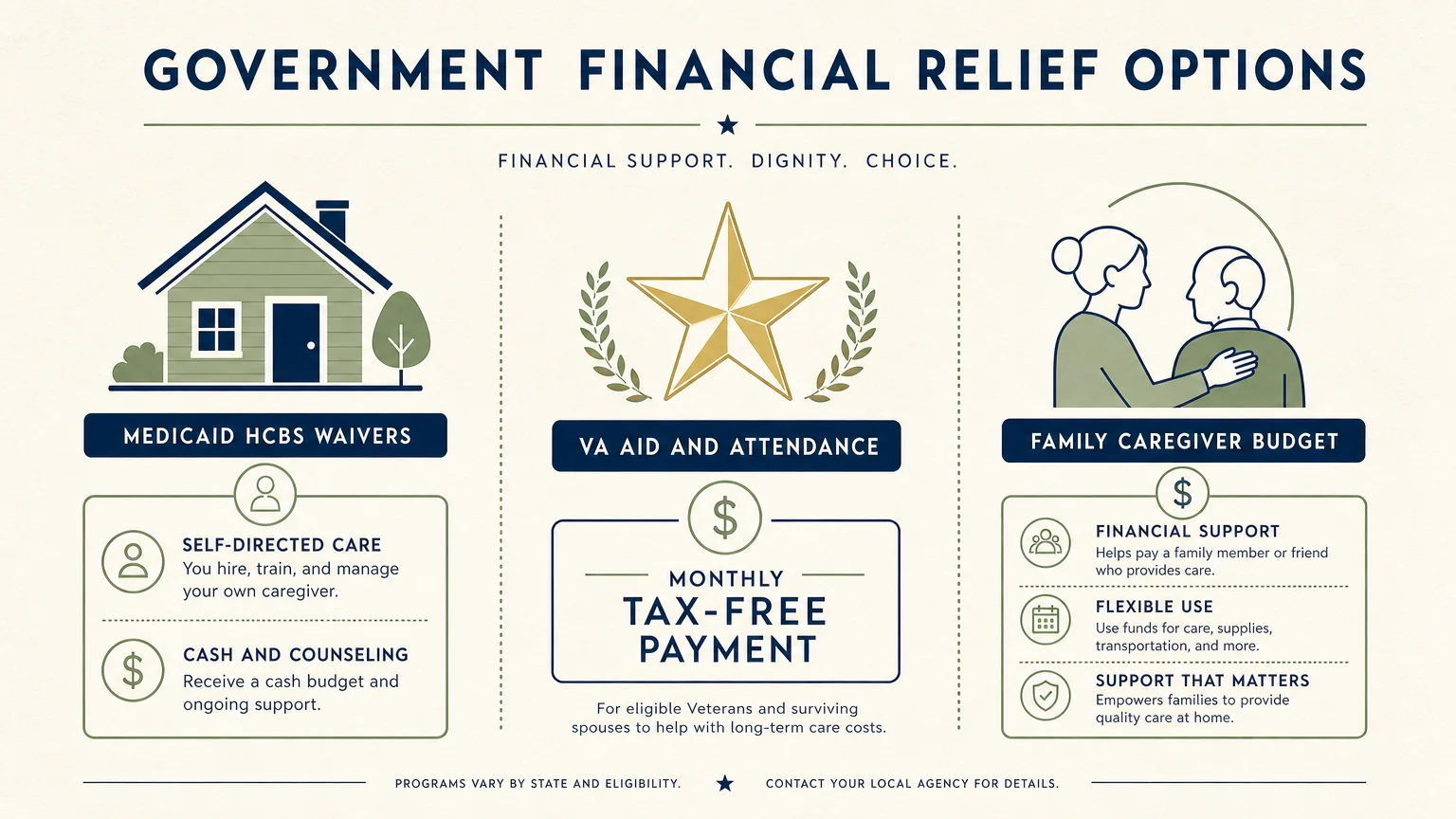

1. Medicaid Home and Community-Based Services (HCBS) Waivers

Medicaid is not just for nursing home care; it also provides robust support for seniors who wish to age in place. Through HCBS Waivers, states can waive certain Medicaid rules to pay for support services delivered in the home. One of the most powerful features of this program is “self-directed care” or “Cash and Counseling.” Under this model, the senior receives a budget to hire their own caregivers—which can frequently include adult children, relatives, and sometimes even spouses.

According to experts at the Centers for Medicare & Medicaid Services (CMS), HCBS programs vary drastically by state. You will need to check your specific state’s Medicaid website to understand the exact income limits, medical requirements, and specific family payment structures available to you. To qualify, your loved one must generally require a nursing home level of care but choose to live at home.

2. Veterans Affairs (VA) Aid and Attendance

If your loved one is a veteran or the surviving spouse of a veteran, the Aid and Attendance benefit provides a significant monthly tax-free payment in addition to their standard VA pension. This program is specifically designed for veterans who need help with daily activities, such as bathing, dressing, and eating, or who are bedridden or suffer from severe visual impairment.

The funds provided by Aid and Attendance can be used to pay for home care aides, adult day care, or even family members providing the care. Securing this benefit requires demonstrating wartime service, meeting financial thresholds, and providing medical documentation of the need for assistance. Working with a VA-accredited claims agent or a local Veterans Service Officer (VSO) simplifies the paperwork process and helps prevent application errors.

3. VA Program of Comprehensive Assistance for Family Caregivers (PCAFC)

Distinct from the Aid and Attendance pension, the PCAFC is a highly specialized program offering a monthly stipend directly to the family caregiver. It also provides access to health insurance through CHAMPVA, mental health counseling, and at least 30 days of respite care per year.

Originally restricted to post-9/11 veterans, this program has expanded to include veterans of all service eras who sustained or aggravated a serious illness or injury in the line of duty. The application process involves a rigorous clinical evaluation of the veteran’s needs, but the comprehensive support it provides makes it one of the most robust caregiver assistance programs in the country.

Respite and Daily Care Relief

Caregiver burnout is a documented health crisis. You cannot provide effective care if you are physically exhausted and emotionally drained. Programs designed to give you a temporary break—known as respite care—are essential to maintaining a healthy caregiving dynamic.

4. The National Family Caregiver Support Program (NFCSP)

Funded by the federal government and administered locally, the NFCSP is a cornerstone of family caregiver support. Research from the National Institute on Aging (NIA) shows that regular respite care is critical for preventing caregiver depression and chronic fatigue. The NFCSP directly addresses this by offering five essential services:

- Information to caregivers about available services.

- Assistance in gaining access to support programs.

- Individual counseling, organization of support groups, and caregiver training.

- Respite care to temporarily relieve caregivers from their responsibilities.

- Supplemental services, on a limited basis, to complement the care provided.

This program is available to adult family members caring for someone aged 60 or older, or someone with Alzheimer’s disease or a related dementia of any age. Because funding is distributed locally, waitlists can sometimes exist, so apply as early as possible.

5. Programs of All-Inclusive Care for the Elderly (PACE)

For seniors who require nursing home-level care but want to remain in the community, PACE is a life-changing Medicare and Medicaid program. According to Medicare.gov, PACE provides a comprehensive medical and social service delivery system. An interdisciplinary team of health professionals provides individuals with coordinated care, often centered around an adult day health center.

For you as a caregiver, PACE handles the exhausting logistics of medical care. The program coordinates doctor appointments, manages medications, provides transportation to medical facilities, and offers adult day care. By shifting the burden of medical management to a dedicated team of professionals, you are freed up to focus on spending quality time with your loved one rather than constantly playing the role of medical coordinator.

Disease-Specific and State Grants

Sometimes, broad federal programs do not fully address the unique challenges of specific conditions. Targeted grants and disease-specific networks step into this gap, offering specialized knowledge, funding, and community support.

6. State Lifespan Respite Care Programs

Recognizing that respite care is frequently too expensive for families to manage out of pocket, many states participate in the Lifespan Respite Care Program. These state-run initiatives provide mini-grants or vouchers that family caregivers can use to hire in-home care workers, pay for a short stay in a memory care facility, or cover the cost of adult day care for a few days.

You can use comprehensive government databases like Benefits.gov to filter and identify specific state-level grants that you might be eligible for. These programs aim to make respite care accessible and streamline the process of finding qualified temporary care workers in your local area.

7. Disease-Specific Support Networks

If your loved one suffers from a specific diagnosis—such as Alzheimer’s disease, Parkinson’s disease, ALS, or cancer—dedicated national organizations often provide exclusive grants and support services for caregivers. These organizations understand the precise trajectory of the illness and tailor their support accordingly.

Many of these organizations offer highly specific caregiver training. For example, learning how to safely transfer a loved one with mobility issues, or understanding how to de-escalate behavioral changes in a dementia patient. Additionally, they often host localized support groups where you can connect with other families facing the exact same daily challenges. These groups validate your experience and serve as incredible resources for local recommendations and coping strategies.

Tax Relief and Workplace Protections

Balancing a career with caregiving duties places immense strain on your finances and your professional life. Understanding your rights in the workplace and taking advantage of tax benefits can provide necessary breathing room.

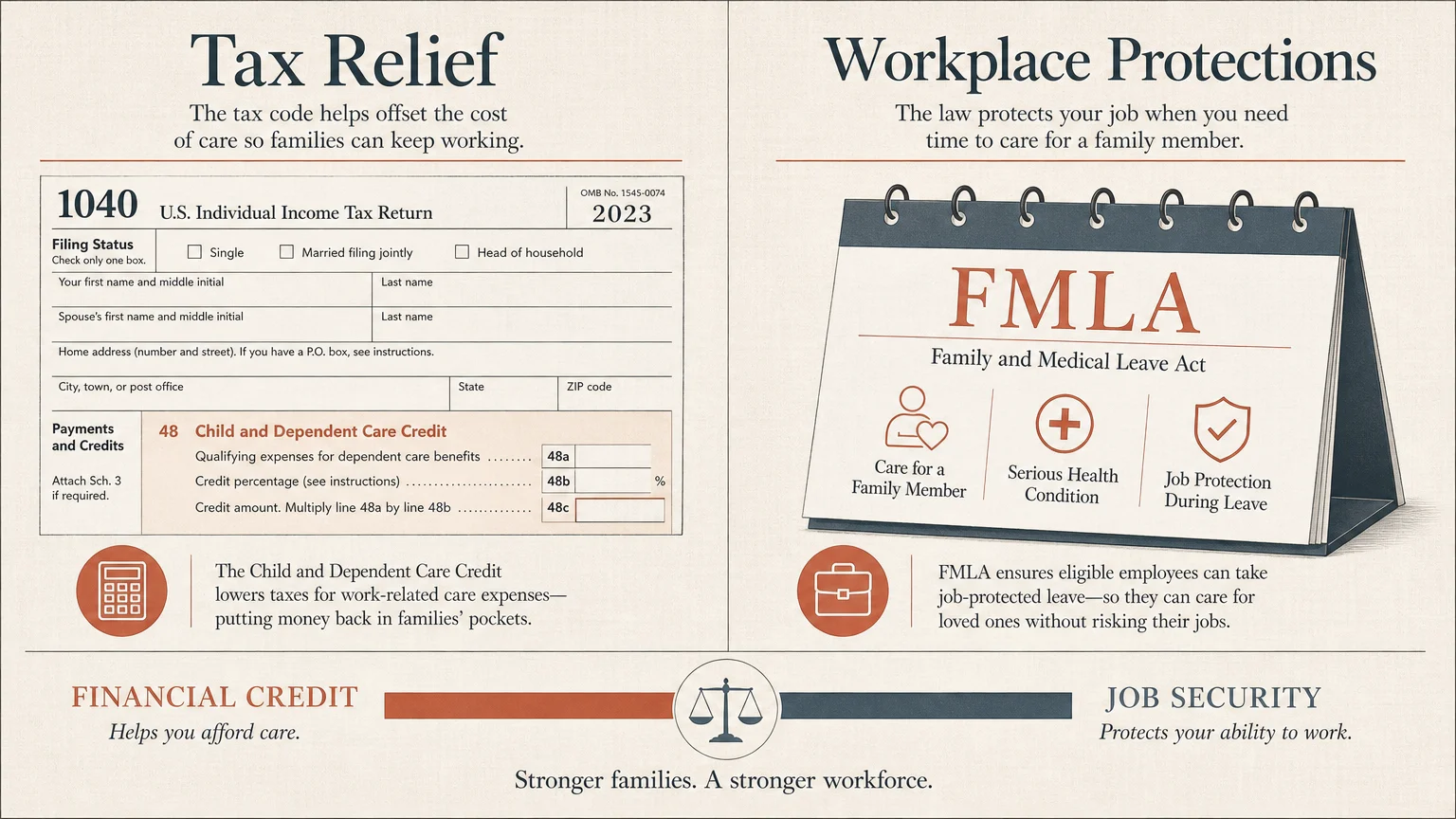

8. The Child and Dependent Care Tax Credit

Despite the name, this tax credit is not just for children. If you pay someone to care for a senior dependent so that you can go to work or actively look for work, you may qualify for this credit. The IRS allows you to claim a percentage of your caregiving expenses, which directly reduces your tax bill.

To qualify, the senior must be claimed as a dependent on your tax return, must be physically or mentally incapable of self-care, and must have lived with you for more than half the year. Eligible expenses include adult day care centers and in-home care aides. Keep meticulous records and receipts of all payments made to care providers to present to your tax professional during filing season.

9. Family and Medical Leave Act (FMLA)

While not a financial payout, FMLA is a critical protection program for working caregivers. FMLA entitles eligible employees of covered employers to take unpaid, job-protected leave for specified family and medical reasons. You can take up to 12 workweeks of leave in a 12-month period to care for a parent, spouse, or child with a serious health condition.

During this time, your employer must maintain your group health insurance coverage under the same terms and conditions as if you had not taken leave. While FMLA is federally mandated and unpaid, several states have implemented their own Paid Family Leave (PFL) programs. State-level PFL allows you to receive a portion of your salary while taking time off to care for a loved one. Check with your company’s human resources department and your state’s labor board to understand exactly what protections and benefits apply to you.

Community and Local Agency Support

Finding help often feels overwhelming simply because you do not know where to start. Local agencies exist specifically to act as navigators, connecting you to the various programs detailed above.

10. Area Agencies on Aging (AAAs)

There are over 600 Area Agencies on Aging across the United States. These local agencies are the primary boots-on-the-ground resource for seniors and their caregivers. They manage the distribution of federal and state funds to local programs and serve as the central hub for eldercare information in your zip code.

According to the Eldercare Locator, connecting with your local Area Agency on Aging can open the door to home-delivered meals (like Meals on Wheels), transportation services, local support groups, and home modification assistance. When you call your local AAA, ask to speak with a care manager or family caregiver specialist. They will conduct an intake interview, assess your loved one’s needs, and provide a customized list of local programs you qualify for.

How to Organize Your Caregiving Documents

Applying for any of these ten programs requires extensive documentation. Gathering these records ahead of time prevents delays in getting approved for financial assistance or respite care. Create a dedicated caregiving binder or a secure digital folder containing the documents outlined in the table below.

| Document Category | Specific Documents to Include | Why You Need It |

|---|---|---|

| Legal & Identification | Birth certificates, Social Security cards, Driver’s licenses, Military discharge papers (DD-214). | Required to prove identity and eligibility for federal and state programs, particularly VA benefits. |

| Financial Records | Recent bank statements, retirement account summaries, property deeds, tax returns for the last 3 years. | Necessary for Medicaid applications and needs-based grants to prove income and asset thresholds. |

| Medical Information | Current medication lists, primary care and specialist contact info, formal diagnoses from physicians. | Used to prove the medical necessity of care, required for HCBS waivers and disease-specific grants. |

| Advance Directives | Durable Power of Attorney (Financial and Medical), Living Will, HIPAA authorization forms. | Allows you to legally speak to government agencies, doctors, and financial institutions on the senior’s behalf. |

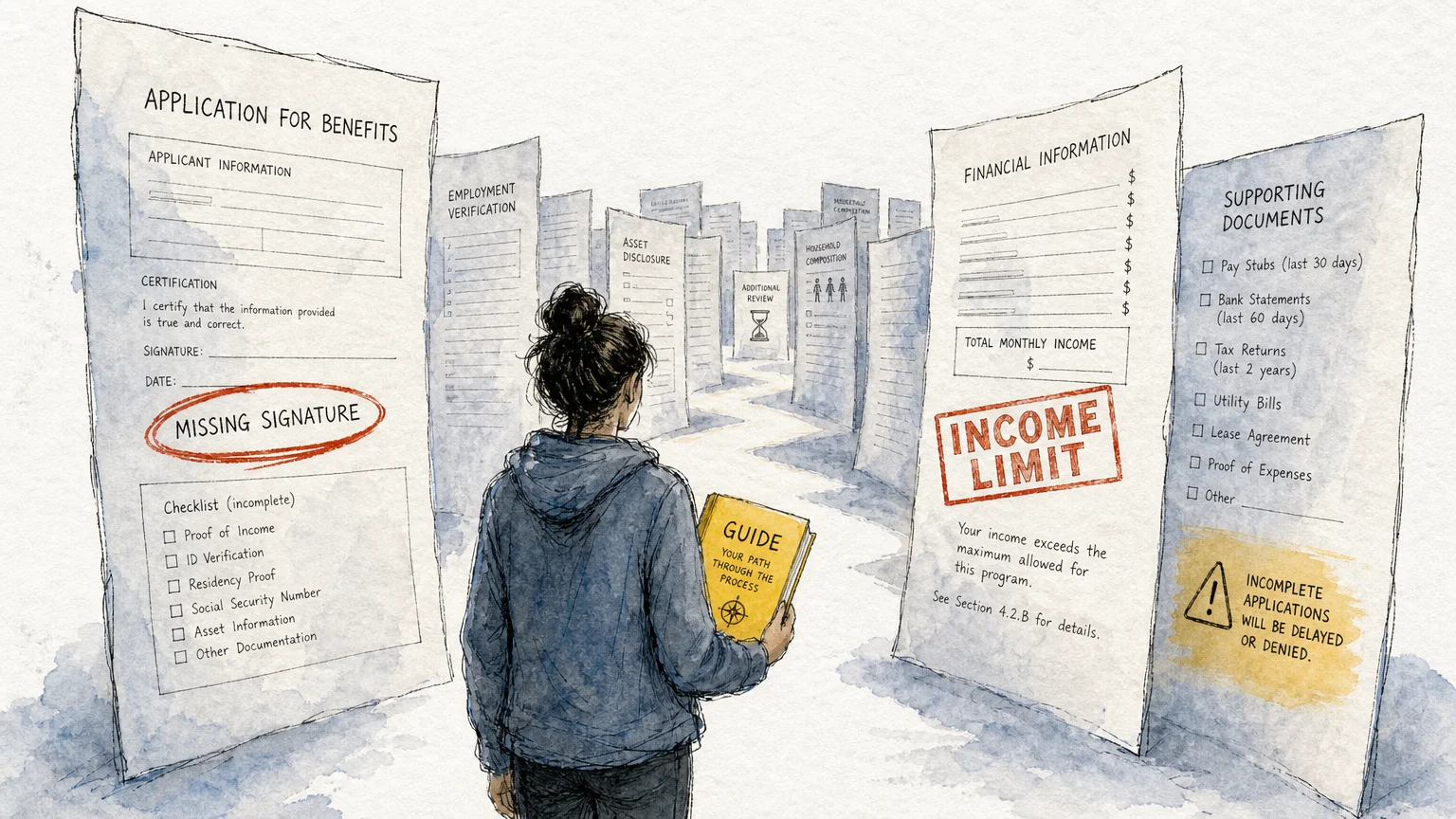

Common Pitfalls When Applying for Assistance

Navigating the bureaucracy of caregiving programs is rarely straightforward. Avoid these frequent mistakes to ensure your loved one receives their maximum benefits.

Applying Too Late

Many programs, particularly Medicaid waivers and state respite grants, have waitlists. Do not wait until you are completely burned out or your loved one’s health has drastically deteriorated to begin the application process. Apply for benefits the moment you anticipate needing them.

Falling for “Grant” Scams

Scammers aggressively target exhausted caregivers. If a company or website asks you to pay an upfront fee to access a “secret government grant” or guarantees approval for benefits, it is a scam. Genuine government programs and non-profit grants never require an application fee.

Violating the Medicaid Look-Back Period

If you anticipate needing Medicaid to pay for home care, be extremely careful about transferring assets. Medicaid reviews all financial transactions made within the past five years (the look-back period). Gifting money to grandchildren, transferring a house title, or selling assets below market value can result in a severe penalty period during which Medicaid will refuse to pay for care. Always consult an elder law attorney before shifting a senior’s assets.

Assuming Medicare Covers Custodial Care

A common and costly misconception is that standard Medicare will pay for a long-term home health aide or a stay in an assisted living facility. Medicare generally only pays for short-term, medically necessary skilled nursing care following a hospital stay. It does not pay for “custodial care”—help with bathing, dressing, and daily living. You must look to Medicaid, the VA, or private long-term care insurance for these expenses.

Frequently Asked Questions

Can I get paid for taking care of my elderly parent?

Yes, under specific circumstances. If your parent qualifies for Medicaid, many states offer self-directed care programs that allow them to hire you as their caregiver. Alternatively, if your parent is a qualifying veteran, the VA offers stipends to family caregivers. If they have a private long-term care insurance policy, some policies permit paying a family member for care.

Do I need legal guardianship to apply for these programs?

You do not necessarily need full legal guardianship, which requires a court process. However, you absolutely need a Durable Power of Attorney (POA) for both healthcare and finances. A POA allows you to sign applications, access medical records, and make financial decisions on your loved one’s behalf without having to go through the court system.

How do I find local caregiver support groups?

The fastest way to find a vetted, local support group is to contact your Area Agency on Aging. You can also check with local hospitals, senior centers, or specific disease foundations. Many organizations now offer virtual support groups via video call, which is highly convenient for caregivers who cannot leave their loved one home alone.

What if my parent refuses help from outside caregivers?

Resistance to outside care is incredibly common, usually stemming from a loss of independence or privacy. Start small by introducing a home care aide for just a few hours a week as a “companion” or “housekeeper” rather than a nurse. Keep the focus on how this assistance helps you, the family caregiver, rather than framing it as something the senior needs, which can help bypass their pride.

Are caregiver stipends considered taxable income?

It depends on the source of the funds. Payments received through the VA Comprehensive Assistance for Family Caregivers are tax-free. However, if you are paid through a Medicaid self-directed program or a private long-term care policy, those wages are generally considered taxable income and must be reported to the IRS. Always consult a tax professional regarding your specific situation.

For additional senior resources, visit AARP, Alzheimer’s Association and American Heart Association.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply