Navigating retirement income can feel overwhelming when you are ready to claim Social Security but your spouse decides to keep working. Your personal benefits based on your own work history remain entirely yours and are not reduced simply because your partner earns a paycheck. However, your spouse’s ongoing income can significantly impact your household tax bracket and potentially trigger taxes on your Social Security payments. Understanding how the earnings test, spousal benefit rules, and joint income thresholds interact will help you maximize your lifetime benefits. By making strategic decisions now, you protect your hard-earned retirement income while supporting your partner’s continued career.

Understanding the Basics of Spousal Benefits

When you prepare to claim Social Security, you must first understand the difference between your own retirement benefit and a spousal benefit. Your own benefit calculates your payout based on the highest 35 years of your earnings. A spousal benefit, on the other hand, allows you to claim up to 50 percent of your partner’s primary insurance amount, which is the benefit they are entitled to at their full retirement age.

A crucial rule dictates how and when you can access these spousal funds. If your spouse is still working and has decided to delay claiming their own Social Security benefits, you are strictly prohibited from collecting a spousal benefit based on their work record. According to the Social Security Administration (SSA), you cannot receive spousal benefits until your working partner actually files for their own retirement benefits.

If you have your own work history, you can certainly file for your own benefits immediately. You do not have to wait for your spouse to retire or file to access the money you earned yourself. Later on, when your working spouse finally retires and claims their Social Security, you can switch over to a spousal benefit if that amount happens to be higher than your own primary benefit. The government will automatically pay you your own benefit first, and then add a secondary amount to bring your total up to the higher spousal level.

How Your Working Spouse Impacts Your Own Record

Many seniors worry that a spouse bringing home a large salary will directly reduce the monthly Social Security check they receive. Rest assured, your personal retirement benefit is an individual entitlement. Your spouse’s ongoing W-2 wages or self-employment income will never trigger a reduction in your own primary benefit.

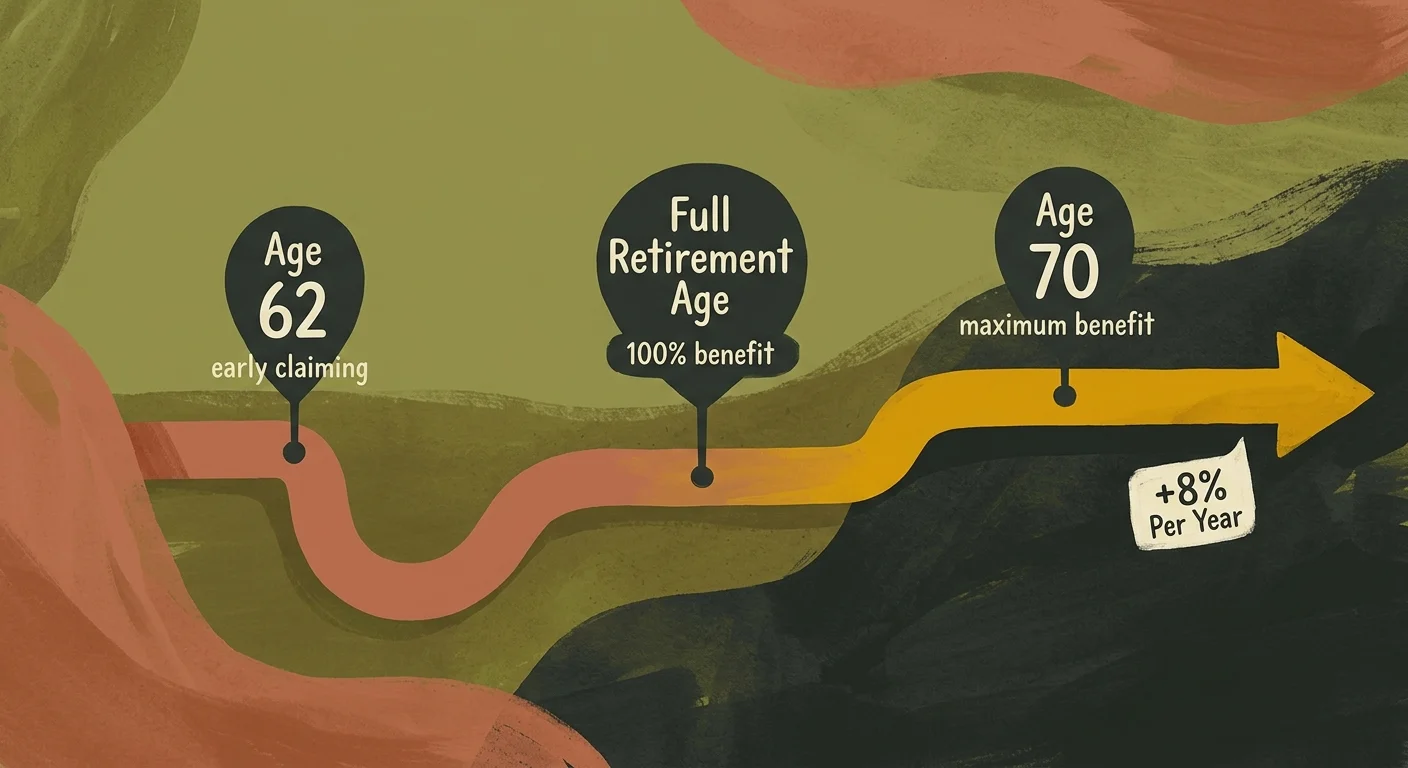

Your benefit relies exclusively on two factors: your lifetime earnings record and the exact age at which you choose to start receiving your payments. If you wait until your full retirement age—which falls between 66 and 67 for most people retiring today—you secure 100 percent of your earned benefit. If you file earlier, your monthly amount permanently decreases. If you delay past your full retirement age, you earn delayed retirement credits that increase your payout by 8 percent per year until you reach age 70.

Your spouse’s employment status plays absolutely no role in this baseline calculation. You earned those credits over decades of hard work. Therefore, you can confidently claim your own benefit and use it to cover household expenses, travel, or savings, completely independent of whether your spouse clocks in for a shift tomorrow morning. The complications only arise when we look at taxation and specific earnings limits, which we will break down next.

The Earnings Test and Spousal Income

The Retirement Earnings Test limits how much money you can earn from a job while claiming Social Security before your full retirement age. If you exceed the annual earnings limit, the government withholds a portion of your benefits. A common point of confusion is whether a working spouse’s income counts toward this limit.

The short answer is no, provided you are claiming on your own record. The Retirement Earnings Test evaluates individual earned income. If you are fully retired and claiming your own benefit, it does not matter if your spouse earns $50,000 or $500,000 this year. Your benefits will not face withholding because you are not the one performing the work.

However, the scenario changes drastically if your working spouse decides to claim Social Security while continuing to work before their full retirement age. In this situation, the earnings test applies to their income. The government will withhold $1 in benefits for every $2 they earn above the standard annual limit. If this happens, it affects their payout directly.

Furthermore, if you eventually receive a spousal benefit based on their record, the earnings test penalty cascades down to you. If your working spouse earns too much and has their benefits withheld, your spousal benefit will also be withheld for those same months. This interconnected rule makes it incredibly important to coordinate claiming strategies. If your partner plans to keep working and earning a substantial income, it is generally wiser for them to delay claiming until they reach full retirement age, at which point the earnings test completely disappears.

Navigating Taxes on Your Social Security Benefits

While your spouse’s income does not reduce your baseline benefit amount, it plays a massive role in how much of your Social Security becomes taxable. The Internal Revenue Service (IRS) taxes your benefits based on your “Combined Income.” This calculation takes into account your entire household income when you file your taxes jointly.

To find your Combined Income, you must add together your Adjusted Gross Income (which includes your spouse’s wages, pensions, and traditional IRA withdrawals), your nontaxable interest, and exactly one-half of your annual Social Security benefits. Because your spouse is still working, their salary pushes your Adjusted Gross Income higher. This frequently causes retirees to cross the thresholds where Social Security benefits become taxable.

Here is how the taxation thresholds break down for married couples filing jointly:

| Combined Income Threshold | Portion of Social Security Subject to Tax |

|---|---|

| Under $32,000 | 0% (Your benefits remain tax-free) |

| Between $32,000 and $44,000 | Up to 50% of your benefits may be taxable |

| Over $44,000 | Up to 85% of your benefits may be taxable |

Keep in mind that these thresholds are not indexed for inflation, meaning more and more seniors find themselves paying taxes on their benefits each year. If your spouse earns a typical full-time salary, it is highly likely that your combined income will easily exceed the $44,000 mark. As a result, you must prepare to pay federal income tax on up to 85 percent of your Social Security payments.

To avoid a surprise tax bill in April, you have two practical options. First, you can request that the government withhold taxes directly from your monthly Social Security check by submitting IRS Form W-4V. Alternatively, your working spouse can increase the tax withholding on their workplace paycheck to cover the anticipated tax burden from your benefits.

Medicare Premiums and Higher Joint Incomes

Another major financial factor influenced by your spouse’s continued employment involves your healthcare costs. When you turn 65, you become eligible for Medicare. While Medicare Part A is generally premium-free, Medicare Part B (medical insurance) and Part D (prescription drug coverage) require you to pay monthly premiums.

If your household income is high because your spouse is still working, you might be subject to surcharges. As noted by experts at Medicare.gov, higher-income earners may pay an Income-Related Monthly Adjustment Amount (IRMAA) on top of their standard Part B and Part D premiums. The government bases this surcharge on your modified adjusted gross income from two years prior. So, the income your working spouse earns today could increase your Medicare premiums two years from now.

For married couples filing jointly, the IRMAA surcharges kick in when your combined modified adjusted gross income exceeds specific limits set annually by the government. If your spouse earns a substantial salary, or if they receive a large year-end bonus, it could push you into a higher IRMAA bracket. This effectively reduces the net amount of your Social Security check, since Medicare premiums are typically deducted directly from your monthly benefit payment.

If your spouse eventually retires or significantly reduces their working hours, you can appeal your IRMAA surcharge. The government considers retirement a “life-changing event.” By filing an appeal with documentation of your spouse’s retirement, you can ask to have your Medicare premiums recalculated based on your new, lower projected income rather than your past tax returns.

Timing Your Claims for Maximum Retirement Income

Deciding exactly when to claim your benefits requires looking at your household as a single financial unit. Because your spouse is still generating income, you have a unique opportunity to evaluate your timeline strategically.

Planning your financial future requires careful consideration, and the Consumer Financial Protection Bureau (CFPB) recommends evaluating your household’s total savings and expected longevity before finalizing your claiming strategy. If your spouse’s income fully covers your day-to-day living expenses, you might not actually need your Social Security check right now. In this scenario, delaying your claim past your full retirement age becomes a powerful wealth-building tool. Every year you delay up until age 70 guarantees an 8 percent increase in your permanent monthly payout.

Conversely, if you suffer from health issues and have a shortened life expectancy, claiming your benefits as early as age 62 might make more sense, even if your spouse continues to work. Taking the money early provides immediate cash flow that you can use to enjoy your retirement years together, pay down high-interest debt, or cover medical expenses.

You must also consider survivor benefits. Research from AARP shows that optimizing survivor benefits is one of the most crucial elements of married retirement planning. When one spouse passes away, the surviving spouse is entitled to inherit the higher of the two benefit amounts, while the lower benefit disappears. If your working spouse is the higher earner, it is generally best for them to delay claiming their benefit as long as possible. Their delay permanently increases the survivor benefit that you will eventually rely on if they pass away first.

Common Pitfalls for Married Retirees

The intersection of one spouse retiring and the other working creates a complex financial landscape. Avoiding common mistakes will protect your retirement nest egg. Pay close attention to these frequent pitfalls:

- Filing separately to avoid Social Security taxes: When couples realize that a working spouse’s income will cause their Social Security to be taxed, they sometimes attempt to file their taxes as “Married Filing Separately.” This is almost always a costly mistake. For married couples filing separately who live together at any time during the year, the base income threshold for taxing Social Security drops to zero. This means up to 85 percent of your benefits become taxable immediately, from the very first dollar.

- Misunderstanding the spousal benefit timeline: Many retirees file for spousal benefits as soon as they reach full retirement age, only to be shocked when their claim is denied. Remember, you absolutely cannot claim a spousal benefit if your working spouse has not yet filed for their own primary benefit.

- Forgetting about the Medicare enrollment window: If your working spouse provides your health insurance through an employer plan that covers 20 or more employees, you might be able to delay enrolling in Medicare Part B without a penalty. However, if the employer has fewer than 20 employees, you must sign up for Medicare at age 65, or you will face permanent late-enrollment penalties. Never assume your spouse’s workplace insurance automatically exempts you from Medicare deadlines.

- Triggering the tax torpedo: Taking large withdrawals from a traditional IRA or 401(k) while your spouse is still drawing a salary can spike your joint income. This sudden influx of taxable income can trigger the taxation of your Social Security benefits and push you into higher Medicare IRMAA brackets simultaneously.

Frequently Asked Questions

Can I get half of my spouse’s benefit while they are still working?

You can only claim a spousal benefit if your spouse is currently receiving their own Social Security retirement benefits. If your spouse is still working and has chosen to delay filing to let their benefits grow, you are not eligible for a spousal payout. You must wait until they officially file their claim.

Will my spouse’s income cause my Social Security to be taxed?

Yes, it is highly likely. The IRS uses your combined household income to determine if your benefits are taxable. Because your working spouse brings in an ongoing salary, your joint income will likely surpass the $32,000 base threshold, meaning up to 50 percent or 85 percent of your Social Security payments will be subject to federal income tax.

Does the earnings limit apply to my spouse’s income if I am the only one claiming?

No. If you are claiming benefits on your own work record, the Retirement Earnings Test only looks at the income you personally earn from working. Your spouse’s wages do not count against your earnings limit, and their high salary will not cause your personal benefits to be withheld.

What happens if we divorce while my ex-spouse is still working?

If you were married for at least 10 years and have been divorced for at least two years, you can claim benefits based on your ex-spouse’s record even if they have not yet filed for benefits themselves. This is a unique exception to the standard spousal rule. Your ex-spouse can continue working and delaying their own claim, and it will not prevent you from receiving your divorced spousal benefit.

Should I delay my claim if my spouse makes enough to support us?

If you do not need the immediate income, delaying your claim is often an excellent strategy. Waiting until your full retirement age guarantees you 100 percent of your earned benefit, and delaying until age 70 maximizes your payout through delayed retirement credits. This provides a guaranteed, inflation-protected increase to your lifetime income.

For additional senior resources, visit

Centers for Medicare & Medicaid Services (CMS), Social Security Administration (SSA), Consumer Financial Protection Bureau (CFPB), Administration for Community Living (ACL) and Eldercare Locator.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply