Managing a fixed income requires strict budget discipline, yet thousands of older Americans unknowingly overpay for essential connectivity every single month. You can significantly reduce your recurring bills by claiming hidden phone and internet discounts designed specifically for seniors and low-income households. From federal subsidies that slash your connectivity costs to exclusive age-based rate reductions at major carriers, these benefits remain chronically underutilized simply because telecom providers rarely advertise them. Securing these reductions keeps more money in your pocket for crucial necessities like groceries, healthcare, and housing. By taking immediate action to audit your current plans and apply for these eight specific programs, you can lock in substantial monthly savings while maintaining reliable access.

1. The Federal Lifeline Program for Essential Connectivity

The Federal Communications Commission (FCC) manages a long-standing initiative known as the Lifeline program, which provides a direct monthly discount on telecommunications services. Despite its availability, this Lifeline program seniors qualify for is largely ignored because many assume it only applies to extreme poverty. In reality, the qualification thresholds accommodate many retirees living on fixed incomes.

If you qualify, the Lifeline program deducts up to $9.25 directly from your monthly phone or internet bill. For seniors living on recognized Tribal lands, this discount increases to up to $34.25 per month. While $9.25 may sound modest, saving over $110 annually on a bill you must pay regardless is a smart financial move.

You can qualify for Lifeline in one of two ways. The first is based on income; your total household income must be at or below 135% of the Federal Poverty Guidelines. The second, and often easier route for retirees, is through program participation. According to the Social Security Administration (SSA), receiving Supplemental Security Income (SSI) automatically makes you eligible for several federal assistance initiatives, including Lifeline. You also qualify automatically if you participate in Medicaid, the Supplemental Nutrition Assistance Program (SNAP), or Veterans Pension and Survivors Benefit programs.

Steps to claim the Lifeline discount:

- Gather your proof of identity and proof of program participation (such as your Medicaid card or SSI award letter).

- Visit the official Lifeline National Verifier website to apply directly.

- Once approved, contact your current phone or internet provider and inform them you have been approved for Lifeline. They will apply the discount to your next billing cycle.

2. Specific Carrier Discounts for Seniors Over 55

If you prefer to stay with one of the major wireless networks, you should never pay standard retail pricing once you turn 55. Major telecommunications companies offer dedicated senior phone plan savings, but their sales representatives rarely offer these plans upfront unless you specifically ask for them.

T-Mobile currently offers the most widely available senior pricing through its Unlimited 55+ plans. For example, a standard two-line unlimited plan might cost $120 to $140 per month. T-Mobile’s base 55+ plan can drop that exact same service to around $80 per month for two lines. That creates an immediate savings of $480 per year. Verizon and AT&T also offer 55+ plans, though they often restrict these deeply discounted rates to residents of specific states, such as Florida, to compete in heavy retiree markets.

Even if your carrier restricts its official 55+ plan to certain regions, you should always ask about unadvertised senior discounts. When auditing your bill, pay attention to the exact features you are paying for. These senior plans typically include unlimited talk, text, and data, but they may limit premium features like mobile hotspot data or high-definition streaming—features that many seniors rarely use anyway.

3. Low-Income Internet Plans from Major Providers

High-speed internet is no longer a luxury; it is a necessity for managing your bank accounts, communicating with healthcare providers through telehealth portals, and staying in touch with family. Recognizing this, almost all major internet service providers (ISPs) offer heavily discounted low-income tiers. Securing an internet discount elderly individuals can afford is simply a matter of knowing which program to request.

These plans operate entirely separate from the federal Lifeline program, meaning you can often utilize both. If you meet the income requirements or participate in SNAP or SSI, you can apply for these direct-from-provider plans. You can use official resources like Benefits.gov to check your eligibility for foundational assistance programs, which subsequently unlocks these ISP-specific discounts.

Here is a breakdown of the most common low-income internet programs available to seniors:

| Provider | Program Name | Estimated Monthly Cost | Typical Speeds |

|---|---|---|---|

| Comcast Xfinity | Internet Essentials | $9.95 | Up to 50 Mbps |

| Spectrum | Internet Assist | $24.99 | Up to 50 Mbps |

| AT&T | Access from AT&T | $30.00 | Up to 100 Mbps |

| Optimum | Optimum Advantage | $14.99 | Up to 50 Mbps |

To claim these rates, you must apply directly through the provider’s dedicated low-income portal. Customer service representatives on the standard sales line often do not have the authority to process these specialized applications, so you must specifically request the “Internet Essentials” or “Access” department when calling.

4. AARP Membership Telecommunications Benefits

If you hold an AARP membership, you are sitting on several valuable telecom savings 60+ individuals frequently ignore. The cost of an AARP membership (roughly $16 a year) pays for itself entirely within the first two months if you leverage their telecommunications partnerships.

According to AARP, active members qualify for immediate rate reductions with partnered providers like AT&T and Consumer Cellular. For AT&T customers, linking your AARP membership to your wireless account typically removes up to $10 per line, per month, on premium unlimited plans. Furthermore, AARP members often get activation and upgrade fees completely waived. Since carriers typically charge $35 just to activate a new phone or upgrade a line, waiving this fee provides instant financial relief.

Consumer Cellular, an alternative carrier known for catering to seniors, offers AARP members a flat 5% discount on monthly fees and routine equipment purchases. If your monthly bill is $40, a 5% discount saves you $24 annually. To apply these discounts, log into your carrier’s online portal and look for a “Discount or Signature Program” tab, or bring your physical AARP card directly to a retail store and ask the representative to attach the code to your profile.

5. State-Specific Telecommunications Assistance Programs

While the federal Lifeline program is the most prominent, many seniors do not realize their specific state operates its own Universal Service Fund. These state-level programs provide additional monthly subsidies that can be stacked on top of federal discounts, pushing your monthly bill even closer to zero.

For example, the California LifeLine program provides significant discounts on both home phone and cell phone services for qualified households. Texas operates the Texas Lifeline program, which offers additional landline and mobile discounts for low-income residents. The rules, income limits, and discount amounts vary wildly across state lines.

Finding these obscure state programs can be frustrating. Based on guidance from the Eldercare Locator, contacting your local Area Agency on Aging (AAA) is the most efficient way to discover localized telecommunications discounts. These agencies employ counselors whose sole job is to connect seniors with state and municipal financial relief programs. Ask them specifically about “state-level telecommunications subsidies” or “municipal utility assistance.”

6. Pre-Paid and Alternative Mobile Virtual Network Operators (MVNOs)

One of the most practical ways to secure phone discounts seniors need is to stop buying service directly from the major three networks. Instead, look into Mobile Virtual Network Operators (MVNOs). These companies lease cellular tower space from AT&T, Verizon, and T-Mobile at wholesale rates, passing the massive savings directly to you.

Popular MVNOs include Mint Mobile, Consumer Cellular, US Mobile, and Lively. Because they do not maintain thousands of expensive retail storefronts, their overhead is incredibly low. If you currently pay Verizon $80 a month for a single line, you spend $960 annually. By switching to an MVNO like Mint Mobile, you could pay as little as $15 a month for unlimited talk, text, and 5GB of data. That brings your annual cost down to $180, instantly returning $780 to your yearly budget.

Checklist for switching to an MVNO:

- Check your data usage. Look at your past three bills to see how many gigabytes (GB) of data you actually consume. Most seniors use less than 5GB a month if they connect to Wi-Fi at home.

- Ensure your current phone is paid off and unlocked. You cannot switch carriers if you are still paying installments on your device.

- Choose an MVNO that uses the network with the strongest coverage in your neighborhood. (For instance, if Verizon works best at your house, choose an MVNO like US Mobile that operates on Verizon’s towers).

- Request a SIM card or eSIM, port your existing phone number over, and begin saving immediately.

7. Bundling and Retention Department Negotiations

If you are entirely unwilling to switch providers, you can still manufacture your own discount simply by knowing how to negotiate. Telecommunications companies spend hundreds of dollars in marketing just to acquire a single new customer; therefore, it is significantly cheaper for them to give you a discount than to let you cancel your service.

Standard customer service agents cannot give you the best deals. You must speak to the “Retention Department” or “Loyalty Department.” To reach them, call your provider’s main number and navigate the automated menu by saying, “Cancel service.” This phrase automatically bypasses frontline workers and connects you to a retention specialist who possesses the authority to lower your rate.

When you speak to the retention agent, use this exact script: “I have been a loyal customer for several years, but I am now on a strict fixed income. My current bill of [Insert Amount] is too high for my budget. I found a competitive offer from [Competitor Name] for [Lower Amount]. Before I switch, what can you do to lower my monthly rate to keep me as a customer?”

In many cases, the representative will offer a promotional credit, un-bundle unnecessary services (like landlines you no longer use), or upgrade you to a modern, cheaper tier. You should repeat this call every 12 to 24 months as promotional credits expire.

8. Local Library and Community Center Connectivity Alternatives

If you only require internet access for occasional tasks—like checking email twice a week, paying a few bills online, or sending photos to grandchildren—you might not need to pay for home internet at all. Many communities provide robust, free technological support specifically for older adults.

Your local public library is one of the most powerful financial resources available. Beyond free high-speed Wi-Fi inside the building, thousands of libraries across the country now offer Wi-Fi Hotspot Lending Programs. You can check out a small mobile hotspot device just like you would a book. You bring it home, plug it in, and enjoy completely free home internet for a lending period of two to four weeks.

Furthermore, local senior centers often maintain open computer labs and offer free technology classes. By utilizing these community resources, you completely eliminate the need for a $60-per-month home internet bill. Over a five-year retirement span, eliminating that single bill saves you $3,600.

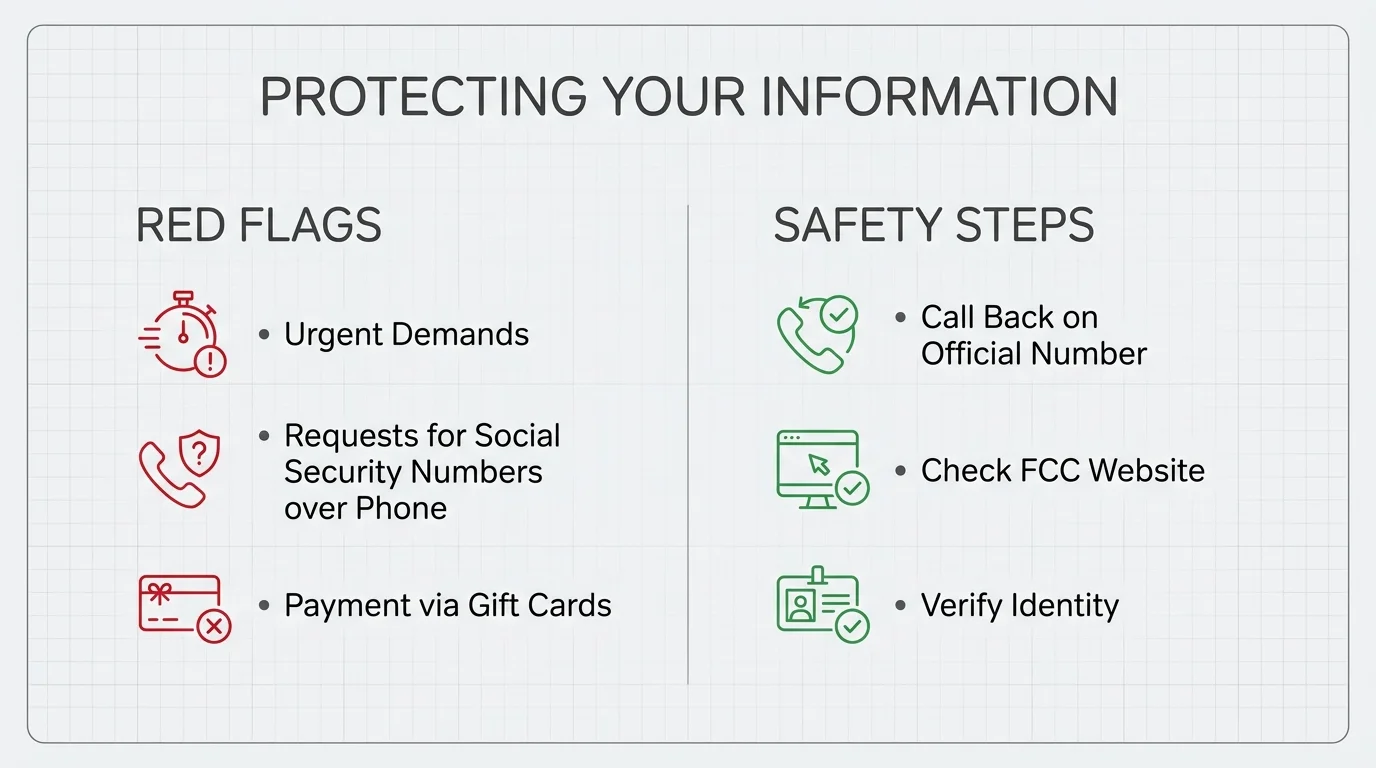

Common Pitfalls and Telecommunications Scams to Avoid

When seeking out financial relief, seniors frequently become targets for predatory scammers. Fraudsters understand that older adults on fixed incomes are actively looking for ways to reduce their bills, and they exploit this vulnerability through highly sophisticated telecommunications scams.

Data from the Consumer Financial Protection Bureau (CFPB) shows that older adults are disproportionately targeted by utility and telecom fraud. You must be vigilant when navigating discount offers. Here are the most common traps to avoid:

- The “Free Device” Trap: You may see advertisements promising a “Free Medical Alert Tablet” or “Free Senior iPad.” While the device itself costs nothing upfront, the paperwork you sign locks you into an exorbitant monthly data contract that costs far more than the tablet is worth. Always read the fine print regarding monthly recurring charges.

- Caller ID Spoofing: Scammers will use software to make their phone number appear as “Verizon Support” or “Comcast Billing” on your caller ID. They will claim your account is past due and demand immediate payment via gift cards or wire transfer to prevent a service shutoff. Real telecom providers will never demand payment via gift cards. If you receive a threatening call, hang up and dial the official number located on your physical paper bill.

- Third-Party Application Fees: Applying for the federal Lifeline program or carrier low-income internet plans is completely free. If a website or “consultant” asks for a processing fee to secure your discount, you are dealing with a scam.

Frequently Asked Questions

Can I have both the federal Lifeline benefit and a low-income internet plan?

Yes, you can often stack these benefits. The federal Lifeline program is a government subsidy, whereas plans like Comcast Internet Essentials or AT&T Access are private corporate programs. If you meet the income requirements, you can apply your $9.25 Lifeline credit to your mobile phone bill, while separately maintaining a $10-$30 low-income home internet plan directly through your ISP.

Does Medicare cover any internet, mobile phone, or connectivity costs?

No. As outlined by Medicare.gov, standard Medicare Parts A and B, as well as Part D, do not cover utility bills, telecommunications, or internet connectivity. Even if you require internet access for a telehealth appointment with your doctor, Medicare will only cover the medical appointment itself, not the data connection required to facilitate it. Some highly specialized Medicare Advantage (Part C) plans may offer a small allowance for over-the-counter utilities, but this is rare and heavily restricted.

Are 55+ senior plans always the cheapest option for my cell phone?

No. While 55+ plans offer great savings compared to standard major carrier rates, they are rarely the absolute cheapest option on the market. If you only use a few gigabytes of data each month, switching to an MVNO like Mint Mobile or Consumer Cellular will almost always result in a lower monthly bill than a major carrier’s 55+ unlimited plan.

How do I prove my income to qualify for federal discount programs?

When applying through the Lifeline National Verifier, you must submit official documentation. Acceptable documents include your prior year’s state or federal tax return, a current income statement from an employer, a Social Security statement of benefits, or an official award letter for programs like Medicaid or SNAP. Bank statements are generally not accepted as sole proof of income.

Can I keep my current phone number if I switch to a cheaper senior discount plan or a new MVNO?

Absolutely. The FCC mandates “Local Number Portability.” This federal rule requires telecom providers to allow you to take your phone number with you when you switch to a new carrier, provided your account is active and in good standing. Do not cancel your old service first; simply set up the new discount plan, and the new provider will handle the number transfer automatically.

For official financial guidance for seniors, visit

Medicare.gov, Centers for Medicare & Medicaid Services (CMS) and Consumer Financial Protection Bureau (CFPB).

Disclaimer: This article is for informational purposes and is not a substitute for professional financial or tax advice. Consult with a certified financial planner or tax professional for guidance on your specific situation.

Leave a Reply