Managing prescription drug costs remains one of the most pressing challenges for older adults on a fixed income. Rising healthcare expenses can force you to make impossible choices between essential medications and other basic needs. Fortunately, numerous pharmacy discounts and drug assistance programs exist specifically to lower your out-of-pocket costs and protect your financial health. Navigating these options might feel overwhelming at first, but understanding the available resources empowers you to take control of your pharmacy bills. You can access substantial savings through federal subsidies, state programs, nonprofit organizations, and pharmacy-specific discount cards. By learning how to leverage these tools effectively, you will secure the medications you need without jeopardizing your retirement budget.

Understanding Medicare Part D and Extra Help

Medicare Part D is the federal government’s prescription drug benefit, designed to help Medicare beneficiaries pay for self-administered medications. While Part D provides a critical safety net, out-of-pocket costs—including monthly premiums, annual deductibles, and copayments—can still add up rapidly. If you have limited income and resources, you might qualify for a federal program called Extra Help, also known as the Low-Income Subsidy (LIS).

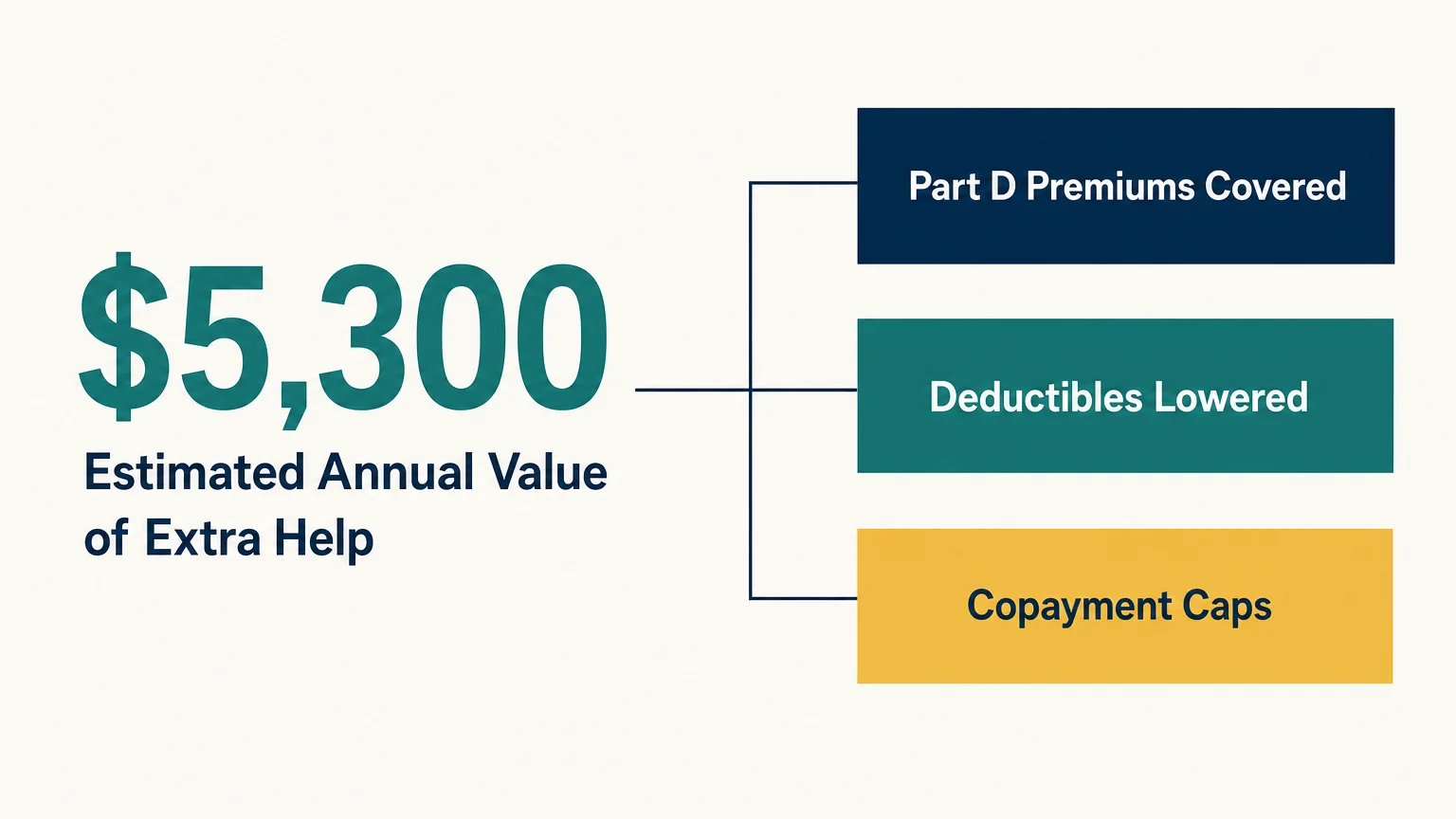

According to the Social Security Administration (SSA), the Extra Help program is estimated to be worth about $5,300 per year for those who qualify. This program covers your Part D premium, eliminates or lowers your deductible, and caps your copayments for covered drugs. Most importantly, qualifying for Extra Help automatically eliminates the Part D late enrollment penalty if you delayed signing up for coverage.

To determine your eligibility, the SSA looks at your annual income and your total resources. Resources include money in checking and savings accounts, stocks, and bonds. The government does not count your primary residence, your vehicles, or your personal possessions toward this limit. Because these limits adjust slightly each year for inflation, you should submit an application even if you think your income is slightly over the threshold. The application process is completely free, and a slight change in the annual guidelines could make you eligible.

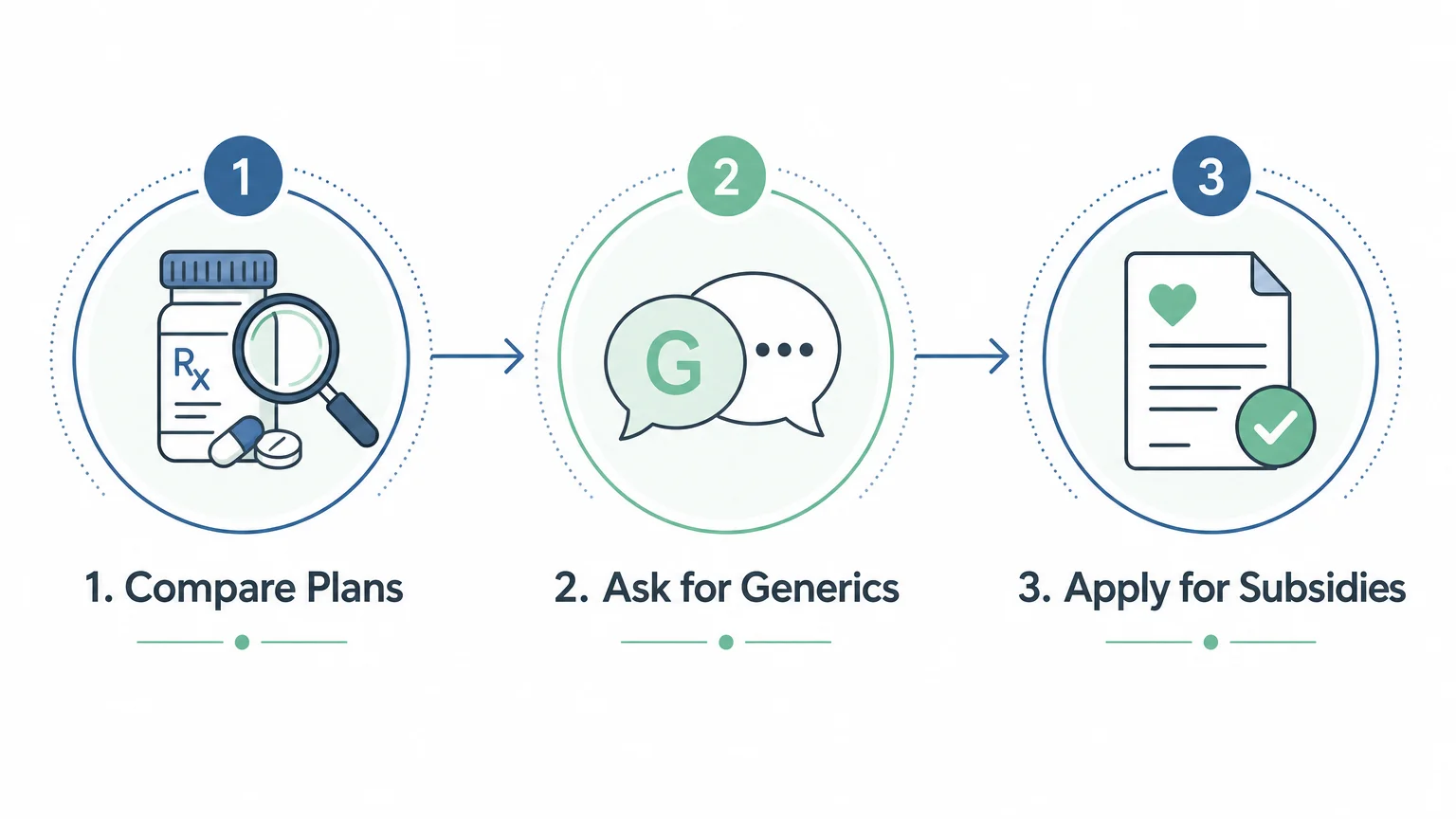

Applying for Extra Help is a straightforward process. You can complete the application online through the SSA website or call them directly to request a paper application. If you already receive Medicaid, Supplemental Security Income (SSI), or a Medicare Savings Program, you automatically qualify for Extra Help and do not need to submit a separate application. Always use the official Medicare.gov plan finder tool during the Annual Enrollment Period to ensure your current Part D plan still offers the best coverage for your specific list of medications.

State Pharmaceutical Assistance Programs (SPAPs)

If you do not qualify for the federal Extra Help program, your state government might offer alternative support. Many states fund State Pharmaceutical Assistance Programs (SPAPs) to help seniors and adults with disabilities pay for prescription drugs. These programs are tailored specifically to residents of the providing state and operate differently depending on where you live.

State programs typically “wrap around” your Medicare Part D coverage. This means the SPAP pays your Part D premiums, deductibles, or copayments up to a certain amount. Some state programs also cover specific medications that Medicare Part D excludes entirely. Eligibility rules for SPAPs are generally more generous than federal programs. They often have higher income limits and may not look at your total financial assets at all.

Because SPAPs vary wildly from state to state, your first step is identifying what your specific state offers. Some states manage robust, well-funded programs, while others offer no state-level assistance at all. The Benefits.gov portal provides a comprehensive, searchable database where you can filter assistance programs by your state and your specific needs. Additionally, your local State Health Insurance Assistance Program (SHIP) counselor can guide you through the local SPAPs available in your area and help you complete the necessary paperwork.

Patient Assistance Programs from Manufacturers

Pharmaceutical companies often run their own Patient Assistance Programs (PAPs) to help seniors access expensive, brand-name medications. These programs provide medications at a significantly reduced cost—or entirely for free—directly from the drug manufacturer. If you take an expensive medication for a chronic condition like diabetes, heart disease, or rheumatoid arthritis, a PAP can be a lifesaver.

Manufacturer assistance programs operate outside of your regular health insurance. When you use a PAP, the pharmaceutical company usually ships a 90-day supply of the drug directly to your home or to your doctor’s office. Each manufacturer sets its own eligibility criteria, but they generally require you to prove financial need and demonstrate that your current insurance does not adequately cover the drug.

Securing this type of assistance requires some paperwork and coordination with your healthcare provider. Here is a general breakdown of the application process:

- Identify the manufacturer: Look at the packaging of your brand-name medication to find the manufacturer’s name. Visit their official website and search for “patient assistance” or “financial help.”

- Download the application: Print the required forms from the manufacturer’s website.

- Gather financial documents: Collect your most recent tax return, social security benefit letter, or bank statements to prove your income.

- Consult your doctor: Most applications require a signature from your prescribing physician. Your doctor will also need to provide details about your diagnosis and why this specific medication is medically necessary.

- Submit and renew: Mail or fax the completed application. Once approved, pay close attention to the renewal dates; most PAPs require you to reapply every year.

Pharmacy Discount Cards and Coupons

Pharmacy discount cards—such as GoodRx, SingleCare, and Optum Perks—have become increasingly popular tools for securing cheaper medications. These programs negotiate discounted cash prices directly with pharmacy networks. Using a discount card is entirely free, and you do not need to meet any income requirements to access the savings.

It is crucial to understand how discount cards interact with your Medicare coverage. You cannot combine a pharmacy discount card with your Medicare Part D insurance at the pharmacy counter. You must choose one or the other for each transaction. When you present a discount card, you are choosing to bypass your insurance and pay the discounted cash price out of your own pocket. Experts at AARP recommend checking discount card prices against your insurance copayments, as the cash price is sometimes significantly lower than what your insurance charges.

The amount you spend using a discount card will not count toward your Medicare Part D deductible or your out-of-pocket maximum. Therefore, if you take multiple expensive medications and expect to hit your out-of-pocket maximum for the year, using your insurance is usually the better long-term strategy. However, if you take only a few inexpensive generic drugs, a discount card might save you money immediately.

Below is a comparison to help you understand when to use each option:

| Scenario | Medicare Part D Insurance | Pharmacy Discount Card |

|---|---|---|

| Medication Cost | Best for expensive, brand-name medications. | Best for inexpensive, generic medications. |

| Deductible Tracking | Money spent counts toward your annual limits. | Money spent does NOT count toward your limits. |

| Formulary Rules | Drug must be listed on your plan’s formulary. | Can be used for any drug, even those not covered by your plan. |

| Usage Complexity | Automatic once your pharmacy has your card on file. | Requires you to look up prices and present a new coupon code each time. |

Nonprofit and Charitable Assistance Options

When federal programs, state programs, and manufacturer discounts fall short, nonprofit organizations can step in to fill the gap. Several national charities operate disease-specific assistance funds. These organizations help underinsured seniors cover copayments, deductibles, and health insurance premiums for specific chronic illnesses.

Prominent organizations like the Patient Access Network (PAN) Foundation, HealthWell Foundation, and the Leukemia & Lymphoma Society provide grants directly to patients. Unlike manufacturer programs that provide the physical drug, these nonprofits provide a financial grant that you use at the pharmacy to pay your copayment.

Because these charities rely on public and corporate donations, their funding fluctuates throughout the year. They organize their grants by specific diseases—such as “Type 2 Diabetes” or “Prostate Cancer.” A fund will open when the charity receives money and close as soon as the funds are depleted. This means you must act quickly if you find an open fund for your specific condition. Check their websites frequently, and sign up for email alerts so you receive notifications the moment a relevant fund begins accepting applications.

Actionable Strategies to Lower Drug Costs

In addition to formal assistance programs, changing how you manage and fill your prescriptions can yield massive savings. By treating your pharmacy expenses just like any other household budget item, you can identify areas to cut costs without sacrificing your health.

Start by talking openly with your prescribing physician about your financial constraints. Doctors rarely know the retail price of the drugs they prescribe, nor do they know the details of your specific Medicare plan. If a medication is too expensive, tell your doctor immediately. They can often prescribe a cheaper alternative, switch you to a generic equivalent, or provide free sample packets to hold you over until you find a more affordable long-term solution.

Consider implementing these practical strategies at the pharmacy counter:

- Request generic alternatives: Generic medications contain the exact same active ingredients as their brand-name counterparts but cost up to 85% less. Always ask your pharmacist if a generic version is available.

- Switch to 90-day supplies: Many pharmacies and Medicare plans offer a bulk discount if you purchase a three-month supply of maintenance medications rather than a standard 30-day supply.

- Utilize preferred mail-order pharmacies: Check your Medicare Part D plan details. Insurance companies often partner with specific mail-order pharmacies, offering significantly lower copayments if you let them mail the drugs directly to your home.

- Ask about pill splitting: Some medications are priced similarly regardless of the dosage. For example, a 100mg pill might cost the same as a 50mg pill. If your doctor approves, they can prescribe the higher dose, and you can use a pill splitter to divide them in half, essentially getting two months of medication for the price of one. (Note: Never split capsules, extended-release pills, or medications without your doctor’s explicit approval).

Common Pitfalls and Scams to Avoid

Unfortunately, scammers actively target older adults by promising unrealistic discounts on expensive medications. Protecting your personal information is just as important as finding legitimate savings. If an offer sounds too good to be true, it almost always is.

One of the most common pitfalls involves unsolicited phone calls or mailers offering “unbelievable” pharmacy discount cards. Legitimate discount programs—like GoodRx or the cards offered by AARP—are free. You should never pay an upfront fee or a monthly subscription charge to join a basic prescription discount program. Scammers will ask for your credit card number, claiming it is required to “activate” the discount card, and then proceed to drain your accounts.

Furthermore, never give your Medicare number, Social Security number, or banking details to anyone who calls you out of the blue offering cheaper medications. Official government agencies like Medicare and the Social Security Administration will never call you unsolicited to ask for your personal information. If you need help finding legitimate programs, rely only on trusted community resources, your local SHIP counselor, or the official government websites.

Another major pitfall is failing to review your Medicare Part D plan during the Annual Enrollment Period (October 15 to December 7). Insurance companies change their formularies (the list of covered drugs) and their pricing tiers every single year. The plan that was perfect for you this year might drop your most important medication next year. Failing to log into the Medicare plan finder and verify your coverage annually is the quickest way to face unexpected, exorbitant pharmacy bills in January.

Frequently Asked Questions

Can I use a pharmacy discount card and Medicare Part D at the same time?

No, you cannot combine the two. At the pharmacy counter, you must choose to process the transaction through your Medicare insurance or use the discount card to pay the cash price. You cannot use a discount coupon to lower your Medicare copayment. Keep in mind that money spent using a discount card will not count toward your Medicare deductible.

How do I know if I qualify for Medicare Extra Help?

Eligibility is based on your annual income and total resources (excluding your home and car). Because the limits change yearly to account for inflation, you should apply if you struggle to pay for medications, even if you think you might be slightly over the limit. You can complete the application for free on the official Social Security Administration website.

Are online or mail-order pharmacies safe to use?

Yes, provided you use legitimate, licensed pharmacies. Your Medicare Part D plan likely has a preferred mail-order partner that is completely safe and often provides lower copayments. If you use an independent online pharmacy, ensure it ends in “.pharmacy” or carries a VIPPS (Verified Internet Pharmacy Practice Sites) seal to confirm it operates legally and dispenses genuine medications.

What happens if my drug is dropped from my Medicare plan’s formulary?

If your plan stops covering a medication you take, you have a few options. First, you can ask your doctor to prescribe a covered alternative. If no alternative works, your doctor can file a “formulary exception” request with your insurance provider, arguing that the specific drug is medically necessary. Finally, you can use the Annual Enrollment Period to switch to a different Part D plan that does cover your medication.

Do manufacturer assistance programs work if I am already on Medicare?

Yes, but the rules are strict. Because Medicare is a government-funded program, federal anti-kickback laws prevent patients from using manufacturer coupons directly at the pharmacy register if they are on Medicare. However, many manufacturers run separate Patient Assistance Programs (PAPs) specifically designed for underinsured Medicare beneficiaries. You must apply directly through the manufacturer’s foundation rather than using a simple register coupon.

For additional senior resources, visit

AARP, Alzheimer’s Association and American Heart Association.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply