Estate planning often focuses entirely on bank accounts, property deeds, and tax brackets, but the legacy you leave behind means far more to your family than just dollars and cents. When your children picture the future, they secretly hope to receive a blend of financial stability, profound personal history, and deep emotional connection. Passing down your life’s work involves sharing your memories, organizing your crucial documents, and ensuring your final wishes bring your family closer together rather than driving them apart. By understanding the twelve distinct things your loved ones actually want to inherit, you can craft a comprehensive, heartfelt legacy that provides lasting comfort, clarity, and guidance for generations to come.

The Tangible Treasures They Cherish Most

When thinking about inheritance, many people immediately picture large sums of money or valuable real estate. However, the items your children often cherish the most hold little monetary value. These tangible treasures serve as physical touchstones to your memory, offering comfort long after you are gone.

1. Meaningful Family Heirlooms

Your children do not necessarily want your most expensive jewelry; they want the pieces you wore every day. They want the pocket watch that belonged to your grandfather, the quilt you stitched by hand, or the worn armchair where you read to them. These items carry the energy of your daily life. To ensure these items go to the right person, take time now to write small index cards detailing the history of each piece and who you would like to have it. Tape these cards to the bottom or back of the items to prevent future confusion.

2. Secret Family Recipes

Taste and smell are powerfully tied to memory. That special holiday casserole, your famous chocolate chip cookies, or the Sunday roast recipe you perfected over decades are invaluable family assets. Write these recipes down exactly as you make them—including the “pinch of this” and “dash of that” measurements. Compiling a small, handwritten recipe book gives your children the ability to recreate the warmth of your kitchen for their own families.

3. Labeled and Organized Photographs

A box of thousands of loose, unlabeled photographs is overwhelming for grieving children. They may not recognize your distant relatives or know the context of an old vacation photo. Take the time to sort through your photo albums. Discard the blurry duplicates and carefully label the backs of the keepers with a soft lead pencil. Include the names, dates, and locations. Curating your photo collection turns a daunting chore into a beautiful, accessible visual history of your family.

Your Personal History and Wisdom

Beyond physical objects, your children crave an understanding of who you are as a person. Sharing your inner world provides them with a profound sense of roots and identity.

4. Family Stories and Journals

Children often realize too late that they forgot to ask about your youth. They secretly hope you will leave behind written stories, audio recordings, or journals detailing your life. What was your first job? How did you meet your spouse? What was your proudest moment, and how did you overcome your biggest failure? You do not need to be a professional writer to start a journal. Buy a simple notebook and aim to answer one question about your life each week.

5. Your Core Values and Life Advice

Many cultures practice the tradition of leaving an “ethical will.” Unlike a legal will that dictates the distribution of property, an ethical will passes down your values, beliefs, life lessons, and hopes for your family’s future. Writing a heartfelt letter to your children explaining what you learned about love, resilience, and forgiveness gives them an enduring compass to navigate their own lives. It is perhaps the most enduring gift you can offer.

Financial Stability and Organized Assets

While sentimental items bring emotional comfort, your children also rely on your diligence in managing your financial affairs. Leaving a clean, organized financial estate prevents unnecessary stress and legal expenses.

6. Financial Wealth and Real Estate

Whether your savings are modest or substantial, your children hope you have managed your finances responsibly. They hope to inherit assets that can help pay for their own children’s education, pay down a mortgage, or provide a safety net. Keep your beneficiary designations updated on all retirement accounts and life insurance policies. According to the Social Security Administration (SSA), establishing a clear record of your earnings and understanding potential survivor benefits can significantly ease the financial transition for your surviving spouse and dependents.

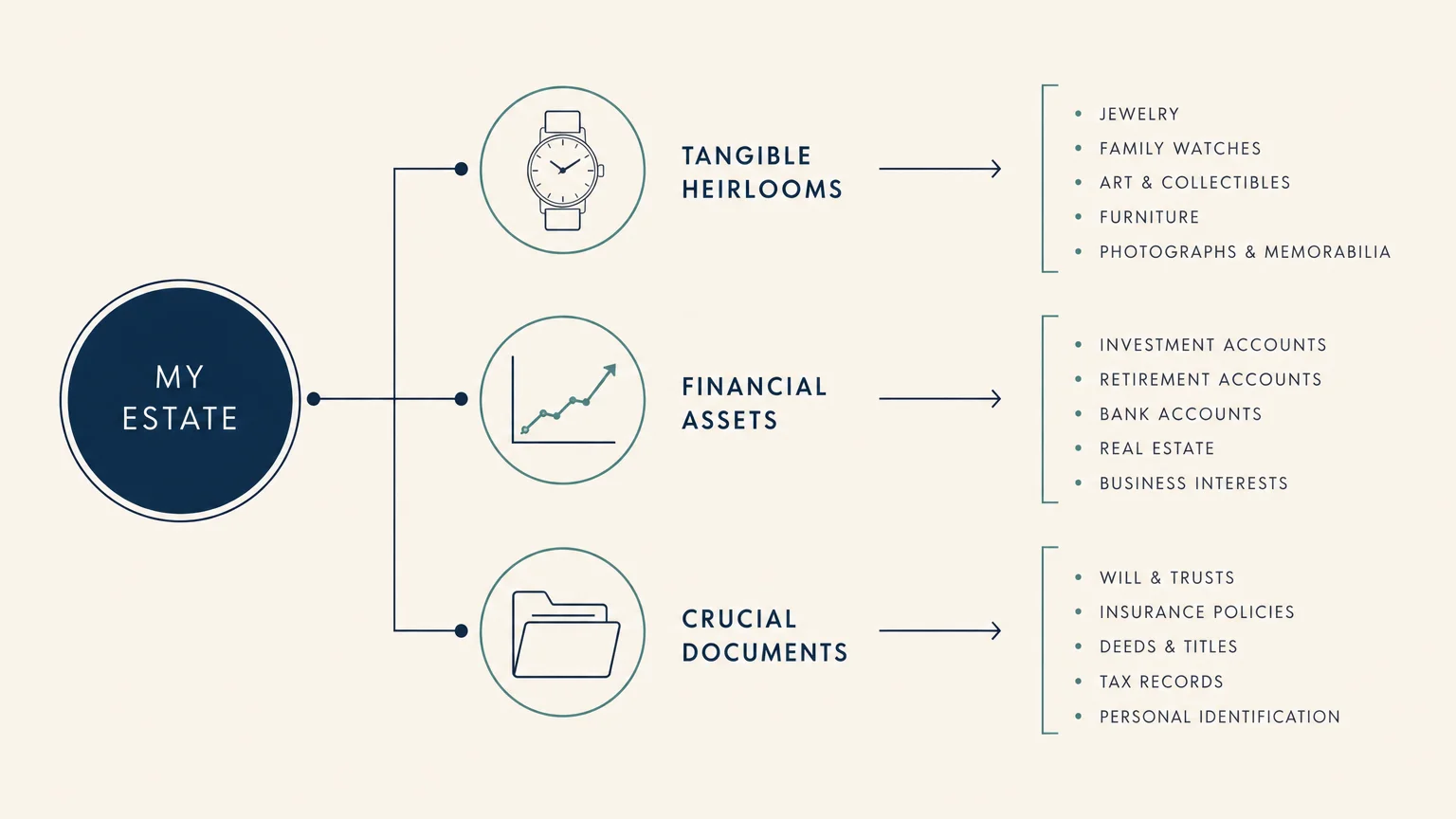

7. A Clear, Organized Estate Plan

An unorganized estate forces your children into a maze of legal and financial hurdles. They secretly hope you have compiled everything they need into one secure location. Experts at the Consumer Financial Protection Bureau (CFPB) emphasize that keeping your financial documents organized and accessible prevents your family from scrambling to locate assets during a time of grief.

Create a master binder or a secure digital file containing the following critical documents:

| Document Type | What It Does | Where to Keep It |

|---|---|---|

| Last Will and Testament | Dictates asset distribution and names your executor. | Fireproof safe or attorney’s office. |

| Revocable Living Trust | Bypasses probate for assets titled within the trust. | With your estate planning attorney. |

| List of Financial Accounts | Details bank names, account numbers, and contact info. | Secure master binder at home. |

| Property Deeds and Titles | Proves ownership of real estate and vehicles. | Safe deposit box or fireproof safe. |

Crucial Information for Their Future

Your children need access to specific information that directly impacts their own well-being and daily lives. Preparing this data requires foresight.

8. A Detailed Family Medical History

Genetics play a massive role in our health. Your children and grandchildren need to know the specific illnesses, chronic conditions, and causes of passing within your family tree. Research from the National Institute on Aging (NIA) highlights that sharing your comprehensive medical history helps your children and grandchildren make informed, proactive decisions about their own preventive healthcare. Document details like ages of onset for heart disease, cancer, diabetes, or Alzheimer’s disease.

9. Access to Digital Accounts and Passwords

We live in a digital age. Your children will need to shut down your social media profiles, access online bank accounts, cancel subscriptions, and retrieve digital photos. If you leave no instructions, these accounts can remain locked permanently. Utilize a reputable password manager, or maintain an offline, handwritten ledger of your usernames, passwords, and security questions. Keep this ledger locked in a safe and inform your trusted executor exactly where to find it.

Peace of Mind and Family Harmony

The greatest burden you can remove from your children’s shoulders is the burden of guessing what you would have wanted. Clarity brings peace, and peace fosters lasting family harmony.

10. Clear End-of-Life Instructions

No child wants to make agonizing decisions about life support or medical interventions for a parent without guidance. Your children secretly hope you have legally documented your healthcare preferences. Establish an advance directive and a living will. Appoint a healthcare proxy—someone you trust to make medical decisions if you become incapacitated. Discussing these choices openly beforehand relieves your children of tremendous guilt and anxiety.

11. Sibling Harmony Through Fair Distribution

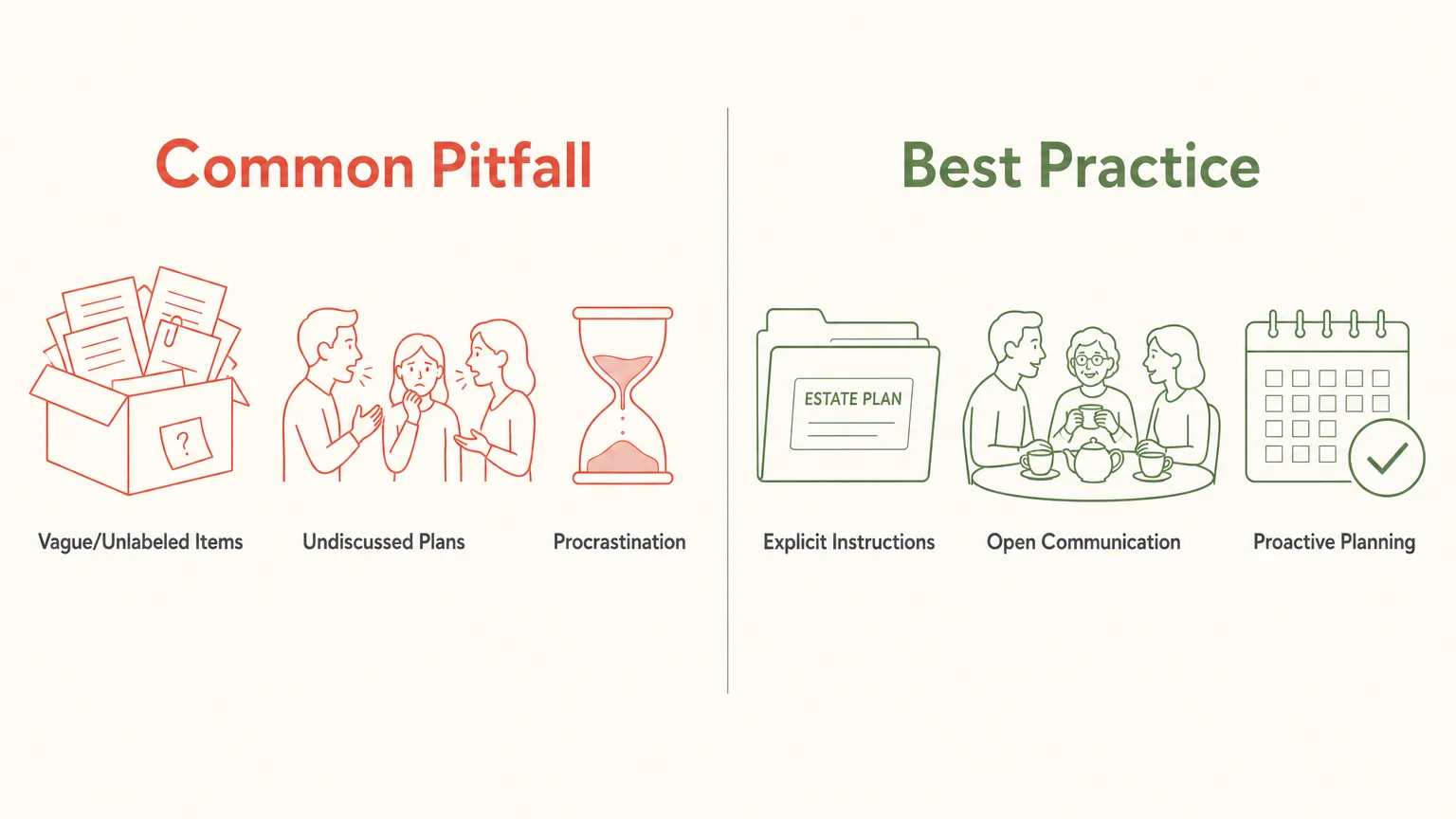

Unclear or seemingly unfair inheritance distributions destroy sibling relationships every day. Your children deeply hope your estate plan does not ignite a family feud. Remember that “fair” does not always mean “equal.” For example, if you provided the down payment for one child’s home a decade ago, you might adjust the inheritance of the other children to balance the scales. The most important step you can take is to communicate your reasoning while you are still alive. Hold a family meeting to explain your decisions so there are no surprises during the reading of the will.

12. Specialized Hobbies and Tools

Did you spend decades restoring classic cars, cultivating a rose garden, or building model trains? Your children want the physical manifestations of your passions. They hope to inherit your woodworking tools, your sewing machine, or your gardening shears. Even better, they hope you will teach them how to use these items now. Invite them into your hobby. Show them how to care for your tools so they can continue your legacy with their own hands.

Common Estate Planning Mistakes to Avoid

Even with the best intentions, seniors often fall into predictable traps that frustrate their heirs. Review your current plans to ensure you are not making these common errors.

Failing to Update Beneficiaries

Your will does not override a beneficiary designation on a life insurance policy or a 401(k). If you named an ex-spouse as a beneficiary thirty years ago and forgot to update it, that person will receive the funds, regardless of what your current will states. Review your beneficiary forms annually.

Hiding Important Documents Too Well

If you hide your will in the floorboards or a secret compartment, your family might never find it. If they cannot find the original document, the state may treat your estate as if you died intestate (without a will), handing control over to a judge. Always tell your executor exactly where your documents reside.

Avoiding the Conversation

According to AARP, one of the most common pitfalls in legacy planning is simply avoiding the conversation altogether, which can leave families confused and vulnerable to unnecessary legal hurdles. Do not let discomfort prevent you from discussing death. Approaching the topic calmly and practically reduces fear for everyone involved.

Not Accounting for Physical Limitations

As we age, managing complex real estate portfolios or stock trades becomes difficult. Simplify your assets while you have the energy. Consolidate stray bank accounts. Sell off burdensome physical property if maintaining it drains your fixed income. A simplified estate is much easier for your children to manage.

Frequently Asked Questions

Do I need a lawyer to create an estate plan?

While there are numerous online templates available, consulting with an estate planning attorney is highly recommended. Laws vary significantly by state, and a small error in a DIY will can render it invalid. An attorney ensures your documents hold up in court and accurately reflect your wishes.

How do I divide my assets fairly if one child cares for me more than the others?

This is a common and delicate situation. Many seniors choose to compensate the caregiving child through a larger portion of the estate, or by paying them a salary while living. If you choose an unequal distribution, it is vital to explain your reasoning directly to all your children in a family meeting to prevent resentment later.

What happens to my debt when I pass away?

In most cases, your debt does not pass directly to your children. Instead, your estate is responsible for settling your debts using your remaining assets. If the estate does not have enough funds to cover the debt, the creditors usually take the loss. However, co-signed loans or shared credit cards are an exception, as the surviving co-signer remains responsible.

How should I store my will and important documents?

Store your original documents in a fireproof, waterproof safe at home or with your attorney. Avoid using a bank safe deposit box for your original will; if the box is rented solely in your name, your family will need a court order to open it after you pass, which delays the entire probate process.

Is a handwritten letter legally binding for passing down personal items?

A handwritten letter (often called a letter of instruction) is generally not legally binding for distributing money or real estate. However, in many states, you can create a legally binding “personal property memorandum” if it is explicitly referenced in your formal will. This allows you to easily update who gets the grandfather clock or the silver tea set without paying an attorney to rewrite your entire will.

For additional senior resources, visit

American Heart Association, Benefits.gov, National Institute on Aging (NIA) and Centers for Disease Control and Prevention (CDC).

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply