Managing your money on a fixed income often requires stretching every dollar to cover rising housing costs, utility bills, and healthcare expenses. If you rely primarily on retirement savings or monthly pension checks, a sudden medical emergency or a spike in property taxes can derail your financial stability. Fortunately, numerous federal, state, and local programs exist to relieve this financial pressure—yet millions of older adults leave billions of dollars on the table every year simply because they do not know these resources exist or assume they do not qualify.

Taking control of your retirement finances means proactively seeking out the benefits you have earned. Whether you need help lowering your monthly prescription costs, reducing your tax burden, or securing utility assistance, these programs are designed to keep money in your pocket. Claiming these benefits early allows you to preserve your savings, reduce your daily financial stress, and protect your long-term independence.

Healthcare and Prescription Savings

Medical costs rank among the most significant threats to retirement security. Even with comprehensive insurance, copayments and deductibles can quickly drain your bank account. Claiming the right healthcare assistance programs can save you thousands of dollars annually.

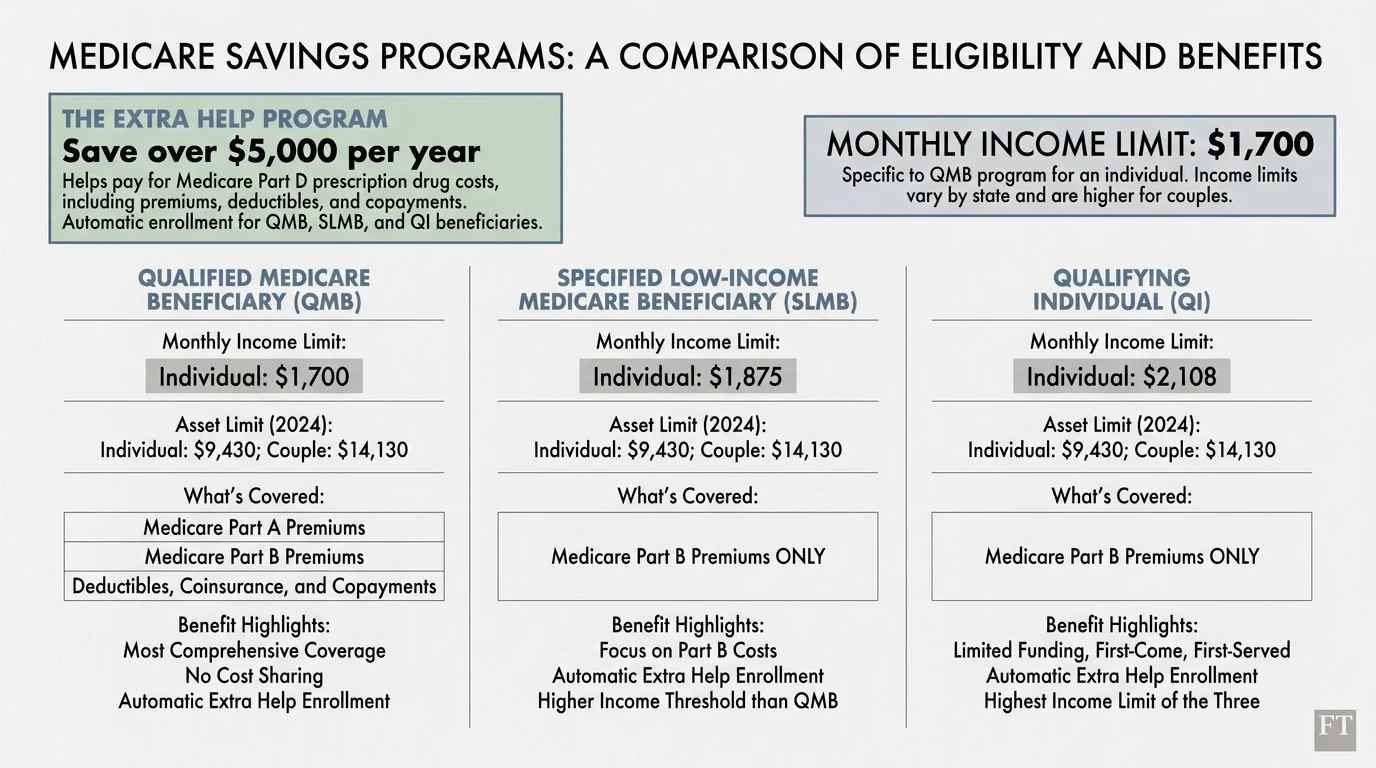

1. Medicare Savings Programs (MSPs)

If you struggle to pay your monthly Medicare premiums, you should immediately look into Medicare Savings Programs. Administered by individual states but funded federally, these programs help cover your Part A and Part B premiums, deductibles, coinsurance, and copayments. There are four main types of MSPs, each with different income and asset limits. Most beneficiaries interact with the top three:

| Program Name | What It Covers | Estimated Impact |

|---|---|---|

| Qualified Medicare Beneficiary (QMB) | Part A and Part B premiums, deductibles, coinsurance, and copays. | Saves you from out-of-pocket costs for Medicare-covered services. |

| Specified Low-Income Medicare Beneficiary (SLMB) | Part B premiums only. | Puts the standard Part B premium amount back into your monthly Social Security check. |

| Qualifying Individual (QI) | Part B premiums only. | Functions like SLMB but allows for slightly higher income thresholds. Requires annual re-application. |

To claim this benefit, you must apply through your state’s Medicaid office. Income limits adjust annually for inflation; however, if your individual monthly income hovers around or below $1,700, you should submit an application.

2. The Extra Help Program (Part D Low-Income Subsidy)

Prescription medications carry a heavy financial burden for seniors managing chronic conditions. According to Medicare.gov, the Extra Help program assists beneficiaries with limited income and resources in paying for Part D prescription drug premiums, deductibles, and coinsurance. The financial relief provided by Extra Help is substantial—beneficiaries typically save over $5,000 per year on medication costs.

To maximize this benefit, keep your financial documents organized and apply even if you think you might barely miss the income cutoff. Furthermore, anyone enrolled in a Medicare Savings Program is automatically enrolled in Extra Help.

3. State Pharmaceutical Assistance Programs (SPAPs)

If your income is too high to qualify for Extra Help but you still struggle with out-of-pocket medication costs, investigate whether your state offers a State Pharmaceutical Assistance Program. These state-funded programs help pay for prescription drugs specifically for older adults and individuals with disabilities. SPAPs work alongside Part D plans to pay your premiums, deductibles, and copayments—often covering medications during the coverage gap.

Essential Income and Nutrition Assistance

Maintaining a healthy diet and a steady cash flow is vital for your physical and financial well-being. Several safety net programs exist to ensure you have the funds necessary for basic survival.

4. Supplemental Security Income (SSI)

Many seniors confuse regular Social Security retirement benefits with Supplemental Security Income. According to the Social Security Administration (SSA), SSI is a distinct, needs-based program that provides monthly cash payments to older adults and individuals with disabilities who possess very limited income and resources.

If your work history was brief or your earnings were low throughout your career, your standard retirement check might not cover basic living expenses. SSI bridges this gap. For example, if your only income is a $600 monthly retirement check, SSI could provide an additional cash top-up to help you reach the federal baseline. Furthermore, qualifying for SSI often triggers automatic eligibility for Medicaid and SNAP benefits in many states.

5. Supplemental Nutrition Assistance Program (SNAP)

Grocery inflation severely impacts fixed-income households, yet older adults are the demographic least likely to enroll in SNAP. This reluctance often stems from complex application processes or the misconception that the benefit amount will be too small to justify the effort.

Seniors have access to a specific SNAP advantage: the medical deduction. If you are 60 or older and spend more than $35 a month on out-of-pocket medical expenses, you can deduct these costs from your gross income when applying. This deduction lowers your countable income, frequently resulting in a significantly higher monthly grocery benefit. You can claim transportation costs to medical appointments, prescription glasses, and dental care under this deduction.

Housing and Utility Bill Relief

Keeping a roof over your head and the lights on takes up a massive percentage of a retirement budget. Federal and state housing benefits help you maintain your independence safely.

6. Low-Income Home Energy Assistance Program (LIHEAP)

Utility costs fluctuate wildly depending on the season and global energy markets. LIHEAP provides a one-time financial grant to help cover the costs of heating your home in the winter and cooling it in the summer. Rather than sending cash to you directly, the program usually sends the payment straight to your utility provider to reduce your balance.

Steps to claim LIHEAP:

- Gather your recent utility bills and proof of income.

- Locate your local community action agency or state LIHEAP office.

- Apply early in the season—funds are distributed on a first-come, first-served basis and often run out before the winter ends.

- Ask about weatherization assistance, which can provide free home improvements like insulation and weatherstripping to lower your future bills permanently.

7. Section 202 Supportive Housing for the Elderly

Finding safe, affordable housing is a growing crisis for older adults. The Department of Housing and Urban Development (HUD) operates the Section 202 program to provide subsidized rental housing specifically for very low-income seniors. In these communities, you generally pay only 30% of your adjusted monthly income toward rent; the federal government covers the remainder.

Because waitlists for these properties can stretch for years, you should identify eligible properties in your area and submit your applications immediately. Do not wait until your current living situation becomes financially unsustainable.

Tax Deductions and Exemptions

You can effectively increase your monthly income by reducing the amount of taxes you owe. Tax codes feature several carve-outs specifically designed for seniors.

8. The Higher Standard Deduction for Seniors

When you file your annual tax return, you must choose between itemizing your deductions or taking the standard deduction. For the vast majority of older adults, the standard deduction offers the better financial outcome—especially because the IRS offers a larger standard deduction once you turn 65.

Based on IRS.gov guidelines, single filers and married couples over age 65 are entitled to an additional standard deduction amount on top of the base standard deduction. If both you and your spouse are 65 or older, you both receive this extra amount, significantly lowering your taxable income. You must check the specific box indicating your age on Form 1040 to claim this money; it is not applied automatically if you overlook the checkbox.

9. Property Tax Circuit Breakers and Homestead Exemptions

If you own your home, rising property taxes can threaten your ability to stay in it. Many states offer “circuit breaker” programs designed to prevent property taxes from overloading your budget. If your property tax bill exceeds a certain percentage of your income, the state provides a refund or tax credit to offset the difference.

Additionally, look into local homestead exemptions or senior property tax freezes. These programs either exempt a portion of your home’s assessed value from taxation or lock in your tax rate at the amount you paid when you reached a specific age. Visit your county assessor’s office to fill out the required paperwork; these exemptions rarely apply automatically.

10. Tax Counseling for the Elderly (TCE)

Paying a professional to prepare your taxes can cost hundreds of dollars. The Tax Counseling for the Elderly (TCE) program offers free tax help to individuals aged 60 and older. IRS-certified volunteers specialize in pension and retirement-related tax issues, ensuring you do not miss senior-specific credits or deductions. By utilizing this service, you save on preparation fees while ensuring your tax return is accurate and compliant.

Daily Living and Legal Resources

Beyond massive expenses like housing and healthcare, smaller daily expenses slowly chip away at your retirement savings. Several federal programs help mitigate these lifestyle costs.

11. The Lifeline Program

In today’s digital world, a reliable phone and internet connection is a necessity, not a luxury; you need it to schedule medical appointments, manage banking, and stay connected with family. The Lifeline Program is a federal initiative that lowers the monthly cost of phone or internet service.

If your income is at or below 135% of the Federal Poverty Guidelines, or if you already participate in programs like Medicaid, SNAP, or SSI, you qualify for a monthly discount on your telecommunications bill. You can apply this discount to either a wireline or wireless service, ensuring you always have access to emergency services.

12. Free Legal Assistance (Older Americans Act)

Drafting a will, navigating a tricky landlord dispute, or dealing with an aggressive debt collector requires professional legal intervention. Under Title IIIB of the Older Americans Act, funds are distributed to local agencies to provide free or heavily discounted legal services to individuals aged 60 and older.

These legal professionals handle non-criminal matters, focusing heavily on issues that threaten your income, healthcare, or housing. The Eldercare Locator connects older adults with their local Area Agency on Aging, where you can request referrals for these vital legal services without paying hefty hourly attorney fees.

Protecting Your Benefits from Scams

As you begin applying for these twelve benefits, you must remain vigilant. Scammers aggressively target older adults, knowing that seniors interact frequently with government agencies like the IRS, Medicare, and the SSA. According to the Consumer Financial Protection Bureau (CFPB), older adults are frequent targets of financial fraud, losing billions of dollars annually to sophisticated schemes.

Follow these strict rules to protect your identity and your assets:

- Never pay to claim a benefit: Government agencies will never ask you to pay a fee, buy a gift card, or wire money to “process” an application or unlock a benefit.

- Do not trust Caller ID: Scammers easily spoof phone numbers to make it look like Medicare or the SSA is calling you. If you receive an unexpected call demanding personal information, hang up immediately and dial the agency’s official public phone number.

- Guard your Medicare Number: Treat your Medicare card exactly like your Social Security card or credit card. Never provide your number to unsolicited callers offering “free” medical equipment or genetic testing.

- Use secure websites: When applying for benefits online, ensure the website address ends in “.gov”. Commercial sites ending in “.com” or “.org” might charge you unnecessary fees for applications that are entirely free on the official government portals.

Frequently Asked Questions

Does claiming state or federal benefits negatively impact my Social Security check?

No; participating in programs like SNAP, LIHEAP, or the Medicare Savings Programs has no negative impact on your earned Social Security retirement benefits. These programs are designed to supplement your fixed income, not replace or reduce your primary retirement funds.

Do I have to reapply for these benefits every year?

It depends on the program. Most income-based assistance—such as SNAP, Medicaid, and Medicare Savings Programs—requires an annual redetermination or recertification. You must submit updated financial information yearly to prove you still meet the eligibility thresholds. Failing to return this paperwork is the most common reason seniors lose their benefits.

What if I own a home; can I still qualify for financial assistance?

Yes. Owning a primary residence does not automatically disqualify you from needs-based assistance. For instance, programs like SSI and Medicaid generally exclude the value of your primary home and one vehicle when calculating your countable assets, provided you live in the home.

How do I know if my income is low enough to qualify?

Income limits vary by state, household size, and specific program rules. Rather than disqualifying yourself by guessing, you should submit formal applications. Many programs offer generous deductions—such as the SNAP medical deduction—that lower your countable income and help you qualify even if your gross income appears slightly too high.

For official financial guidance for seniors, visit Social Security Administration (SSA), Medicare.gov, Centers for Medicare & Medicaid Services (CMS), Consumer Financial Protection Bureau (CFPB) and IRS.gov.

Disclaimer: This article is for informational purposes and is not a substitute for professional financial or tax advice. Consult with a certified financial planner or tax professional for guidance on your specific situation.

Leave a Reply