Navigating healthcare costs in retirement requires a clear understanding of your available safety nets. As you cross into your late sixties and beyond, the statistical likelihood of needing long-term care increases dramatically. Nursing home care, assisted living, and in-home health aides come with staggering price tags that can drain a lifetime of savings in a matter of months. This is where Medicaid steps in.

Medicaid is a joint federal and state program designed to help individuals with limited income and resources cover medical costs. More importantly for seniors, it is the primary payer across the nation for long-term custodial care. Because states administer their own Medicaid programs within broad federal guidelines, the rules for 2026 remain complex, strictly enforced, and highly specific to your location. Understanding the eligibility criteria, asset limits, and application protocols well before you actually need care is the most effective way to protect your life savings and secure the care you deserve.

The Difference Between Medicare and Medicaid

One of the most dangerous financial assumptions seniors make is believing that Medicare will pay for their long-term nursing home care. The reality is far different. Understanding the distinction between these two programs is your first step in building a resilient retirement plan.

According to Medicare.gov, original Medicare is an age-based health insurance program that covers acute care. It pays for hospital stays, doctor visits, and short-term skilled nursing rehabilitation after a qualifying hospital stay. It strictly limits skilled nursing facility coverage to a maximum of 100 days, and copayments apply after day 20. It does not cover custodial care—the help you need with daily activities like bathing, dressing, and eating over a long period.

Medicaid, on the other hand, is a needs-based program. Data from the Centers for Medicare & Medicaid Services (CMS) outlines that Medicaid serves as the payer of last resort for long-term custodial care, either in a nursing facility or through home and community-based services. You can hold both Medicare and Medicaid simultaneously; in these dual-eligible cases, Medicare pays for your medical services first, and Medicaid covers long-term care and remaining out-of-pocket medical costs.

| Feature | Medicare | Medicaid |

|---|---|---|

| Primary Purpose | Acute medical care and short-term rehab. | Long-term custodial care and broad medical assistance for low-income individuals. |

| Eligibility | Age-based (65+) or specific disabilities. | Needs-based (strict income and asset limits apply). |

| Long-Term Care Coverage | No. Covers maximum 100 days of skilled rehab. | Yes. Covers indefinite nursing home care and some in-home care. |

| Cost to Beneficiary | Monthly premiums, deductibles, and copays. | Little to no cost, though nursing home residents must contribute most of their income to care. |

Understanding Medicaid Eligibility for Seniors

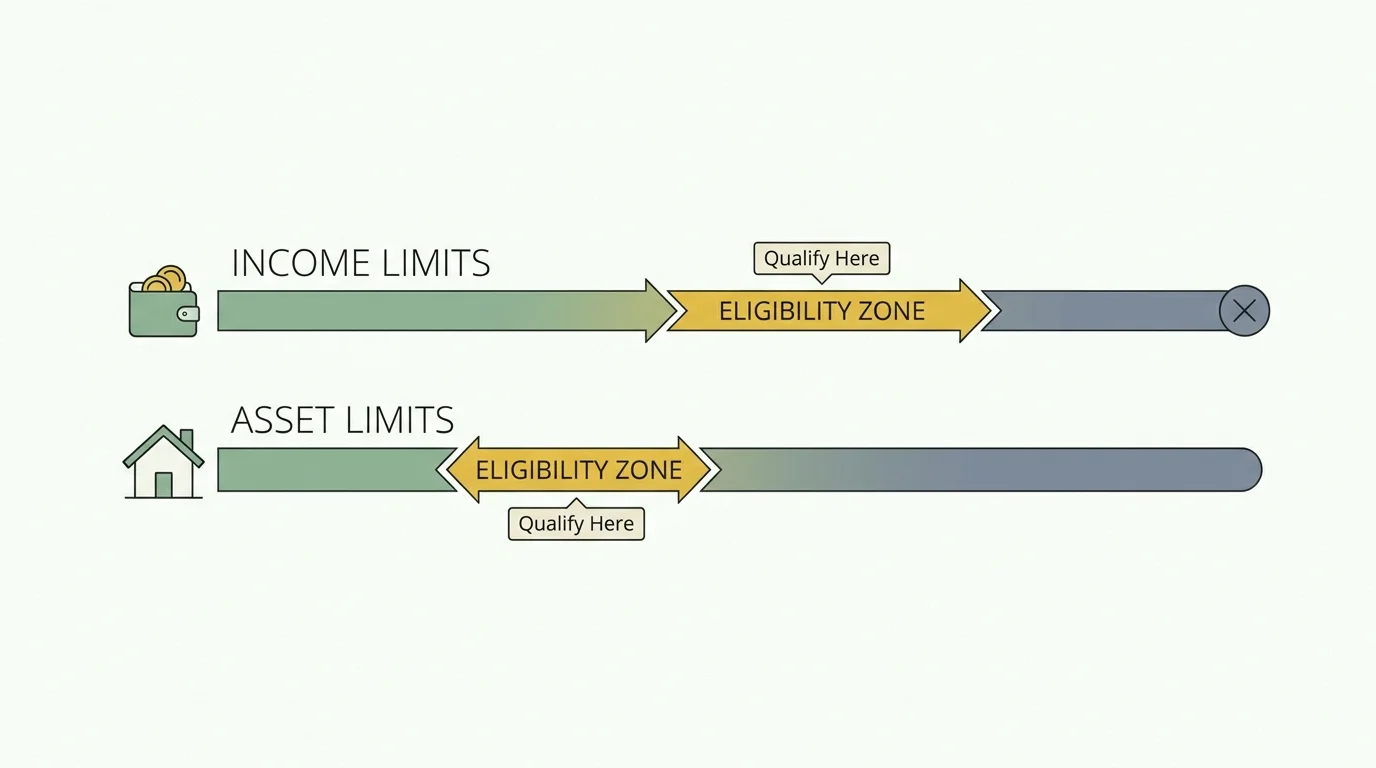

Qualifying for Medicaid as a senior—often referred to as Aged, Blind, or Disabled (ABD) Medicaid or Long-Term Care Medicaid—requires passing stringent financial tests. The government looks at both your monthly income and your total countable assets. Because these rules are adjusted for inflation and vary by state, you must review the specific limits for 2026 in your state of residence.

For most states, the individual asset limit for long-term care Medicaid remains incredibly low—typically locked at $2,000 for a single applicant. If you have $2,001 in countable assets, you do not qualify. However, not everything you own is counted toward this limit.

Countable Assets (Non-Exempt):

- Checking and savings accounts

- Certificates of Deposit (CDs)

- Stocks, bonds, and mutual funds

- Investment properties and vacation homes

- Cash surrender value of whole life insurance policies (if the face value exceeds a state-specific limit, often $1,500)

Exempt Assets (Not Counted):

- Your primary home: Your home is exempt as long as your home equity falls below the state’s limit (ranging generally from $713,000 to over $1,000,000 in 2026, depending on the state) and you express an intent to return home, or your spouse lives there.

- One vehicle: One car of any value is exempt if used for transportation of the applicant or a household member.

- Personal belongings: Household furnishings, clothing, and jewelry are generally exempt.

- Prepaid funeral plans: Irrevocable burial contracts are fully exempt in most states.

Income limits also apply. Many states use an income cap for nursing home Medicaid, generally around $2,829 per month for a single applicant (exact 2026 figures depend on federal cost-of-living adjustments). If your income exceeds this limit, many states allow you to establish a Qualified Income Trust (often called a Miller Trust) to legally funnel the excess income toward your care while establishing Medicaid eligibility.

The Medicaid Look-Back Period Explained

You cannot simply give away all your money to your children on Monday and apply for Medicaid on Tuesday. To prevent individuals from artificially impoverishing themselves to qualify for taxpayer-funded care, the government enforces a strict look-back period.

In 49 states, the look-back period is 60 months (5 years) from the date of your Medicaid application. California is the lone exception, having phased out its look-back period and asset limits entirely for most Medicaid programs by 2024. During this 60-month window, the state Medicaid agency will review all of your financial transactions.

If the agency discovers you transferred assets for less than fair market value—such as gifting cash to a grandchild, transferring a property deed to a child, or selling a $20,000 car to a friend for $1,000—you will incur a penalty period. During this penalty period, Medicaid will not pay for your long-term care, and you will be responsible for the full cost out of pocket.

How the Penalty is Calculated:

The state calculates the penalty by dividing the total amount of the uncompensated transfer by the average private-pay cost of a nursing home in your state (known as the penalty divisor).

Imagine you live in a state where the average nursing home cost is $10,000 per month. Three years before applying for Medicaid, you gifted $50,000 to your daughter to help her buy a house. Because this gift occurred within the 5-year look-back window, the state divides the $50,000 gift by the $10,000 monthly cost. The result is 5. You will face a 5-month penalty period where Medicaid refuses to pay for your care, leaving you to source $50,000 to cover your nursing home bills.

Spousal Impoverishment Rules: Protecting the Healthy Spouse

When one spouse needs nursing home care and the other remains at home (the “community spouse”), federal law provides robust protections. Medicaid does not expect the healthy spouse to live in poverty to pay for the ailing spouse’s care. These protections govern both assets and income.

Community Spouse Resource Allowance (CSRA):

The CSRA dictates how much of the couple’s combined countable assets the healthy spouse is legally allowed to keep. While the institutionalized spouse is usually restricted to $2,000, the community spouse can keep a significantly larger portion. In 2026, the maximum CSRA varies by state but generally allows the healthy spouse to retain up to roughly $154,000 in liquid assets, plus the exempt primary home and vehicle.

Minimum Monthly Maintenance Needs Allowance (MMMNA):

This rule protects the healthy spouse’s income. If the community spouse has a low monthly income, they are legally entitled to receive a portion of the institutionalized spouse’s income (like their Social Security or pension) to meet a minimum standard of living. In 2026, this allowance guarantees the healthy spouse an income ranging from approximately $2,500 to $3,800 per month, depending on state guidelines and housing costs. Any income the institutionalized spouse has left over after the MMMNA deduction and a small personal needs allowance must go toward their nursing home bill.

Medicaid Estate Recovery Program: What Happens to Your Home

One of the most misunderstood aspects of long-term care Medicaid is the Medicaid Estate Recovery Program (MERP). While your primary home is considered an exempt asset while you are alive and applying for Medicaid, the state has the legal right to seek reimbursement for your care costs after you pass away.

If Medicaid spends $300,000 on your nursing home care over several years, the state will place a claim against your estate—most commonly targeting your house—to recoup that $300,000 upon your death. For many families, this means the family home must be sold rather than inherited.

However, there are legal strategies to protect the home, provided you plan early:

- The Caregiver Child Exemption: If an adult child lived in your home and provided care that kept you out of a nursing home for at least two years immediately before you enter the facility, you may be able to transfer the home to them without a look-back penalty or estate recovery claim.

- Sibling Exemption: If a sibling with an equity interest in the home has lived there for at least one year before you enter the nursing facility, they are protected from estate recovery while they continue to live there.

- Surviving Spouse Protection: The state cannot enforce an estate recovery claim while a surviving spouse, a child under 21, or a permanently disabled child of any age remains living in the home.

- Medicaid Asset Protection Trusts (MAPTs): If executed more than five years before applying for Medicaid, transferring your home into an irrevocable trust can shield it from both the asset limit test and estate recovery.

Common Medicaid Mistakes and Scams to Avoid

Because the stakes are so high, the landscape of Medicaid planning is rife with pitfalls. Making a hasty decision can delay your care, while falling for a scam can drain your resources entirely.

Mistake: The Spend-Down Trap

Many seniors think they must “spend down” their excess assets by paying for their own care until they reach $2,000. While paying for care is one way to spend down, you can also legally spend excess assets on exempt items. You can use excess cash to pay off a mortgage, buy a reliable car, prepay a funeral, or make home modifications like installing a wheelchair ramp.

Mistake: Hiding Assets

Do not attempt to hide bank accounts or transfer property to a relative secretly. Medicaid applications require you to sign under penalty of perjury. Financial institutions report to the IRS, and Medicaid agencies use sophisticated software to trace property transfers and tax records. Fraudulent applications can result in severe financial penalties and criminal charges.

Scam Warning: Predatory “Planners”

The Consumer Financial Protection Bureau (CFPB) warns older adults to be wary of aggressive, uncredentialed advisors who promise hidden loopholes to qualify for Medicaid instantly. Many of these bad actors charge exorbitant upfront fees only to sell you high-commission annuities that actually violate Medicaid rules. Always work with a certified Elder Law Attorney who specializes in Medicaid planning in your specific state.

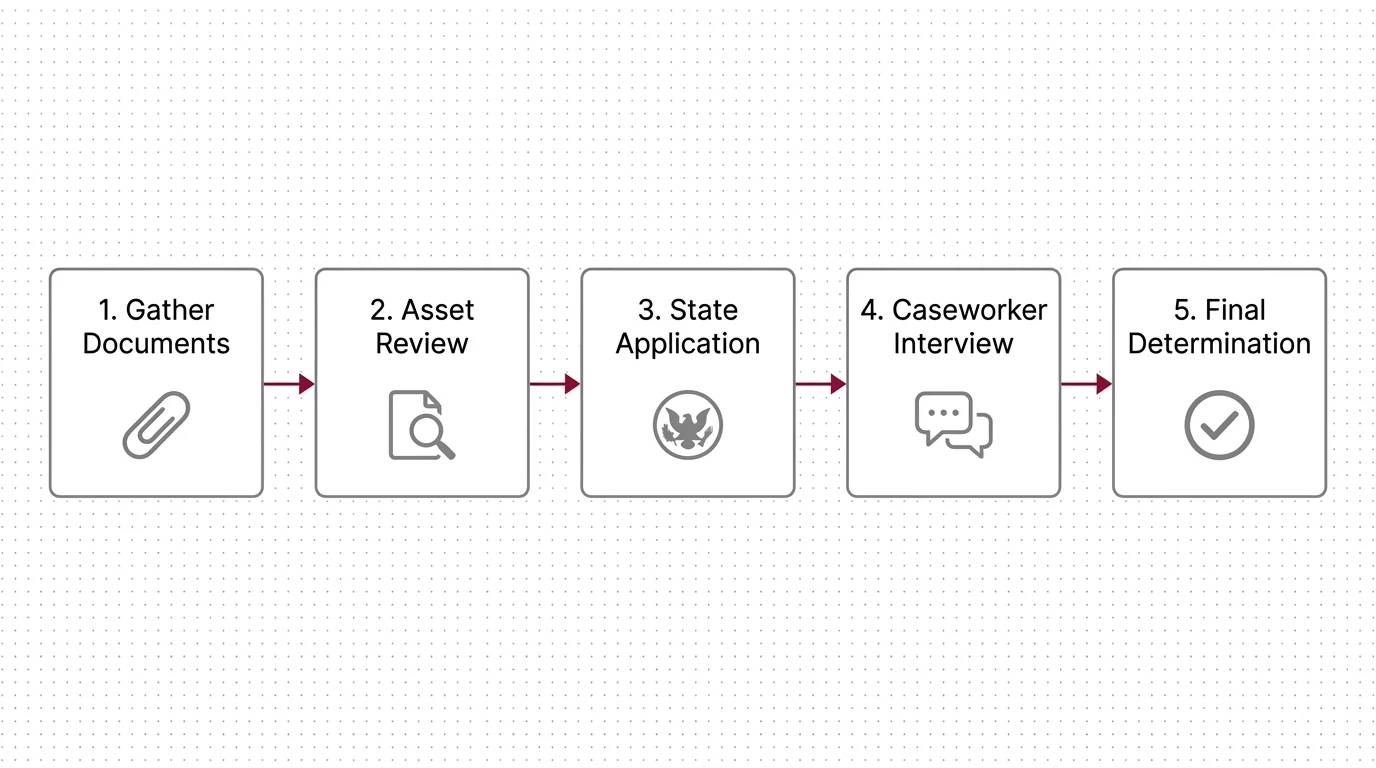

Step-by-Step Guide to Applying for Medicaid

Applying for Medicaid is a rigorous, documentation-heavy process. Approaching it methodically prevents application denials and delays in your care.

Step 1: Check Baseline Eligibility

To check your baseline eligibility and explore other state-specific assistance programs, you can use the screening tools provided by Benefits.gov. This will give you a high-level view of what programs you may qualify for before beginning the formal paperwork.

Step 2: Gather Five Years of Financial Records

Because of the 60-month look-back period, you must prove every financial transaction you made over the last five years. Begin compiling:

- Bank statements for all checking, savings, and investment accounts.

- Deeds to all real estate owned in the last five years.

- Titles to all vehicles.

- Life insurance policies showing cash surrender values.

- Five years of federal and state tax returns.

- Proof of income (Social Security award letters, pension statements).

Step 3: Organize Personal Documentation

You will need your birth certificate, proof of U.S. citizenship or lawful residency, Medicare card, Social Security card, and marriage certificate (if applying with spousal protections).

Step 4: Consult an Expert if Assets are High

If you are over the asset limit or have made large financial gifts in the last five years, pause your application. Consult an Elder Law Attorney. They can establish trusts, execute caregiver agreements, or utilize Medicaid-compliant annuities to protect your remaining assets before you submit the application.

Step 5: Submit the Application

You can apply online through your state’s Medicaid portal, by mail, or in person at your local Department of Social Services or Medicaid office. Once submitted, expect the review process to take anywhere from 45 to 90 days. If you are already in a nursing home, the facility’s social worker can often expedite the submission process and coordinate with the state agency.

Frequently Asked Questions

Can I keep my income if I go into a nursing home on Medicaid?

Generally, no. When you reside in a nursing home on Medicaid, almost all of your monthly income (Social Security, pensions) must be paid to the nursing facility as your “Share of Cost.” You are only allowed to keep a small Personal Needs Allowance—which ranges from $30 to $130 per month depending on your state—to pay for haircuts, clothing, or snacks. The only exception is if a portion of your income is diverted to your healthy spouse at home under the spousal impoverishment rules.

Does Medicaid cover assisted living or only nursing homes?

While Medicaid is federally mandated to cover nursing home care, coverage for assisted living facilities is optional and managed at the state level through Home and Community-Based Services (HCBS) waivers. Most states offer some form of assisted living waiver, but these programs often have strict enrollment caps and long waiting lists. You must check your specific state’s waiver programs to see if assisted living is covered.

What happens if my income is too high to qualify, but not enough to pay for care?

If you live in an “income cap” state and your monthly income exceeds the Medicaid threshold (around $2,829), you will be denied coverage unless you use a Qualified Income Trust (QIT), also known as a Miller Trust. By redirecting your excess income into this legal trust each month, Medicaid no longer counts that money toward your eligibility. The funds in the trust are then used to pay your Share of Cost to the nursing home.

Will my adult children be financially responsible for my Medicaid debt?

Medicaid will never force your adult children to pay for your nursing home care out of their own personal bank accounts. The state can only pursue recovery from the assets left in your estate after you die. However, if you transferred assets (like a house or cash) to your children during the five-year look-back period, those transfers will trigger a penalty, meaning the children would either need to return the money or pay for your care during the penalty period.

Can Medicaid force me to surrender my life insurance policy?

Medicaid does not target term life insurance policies because they have no cash value. However, if you own a whole life insurance policy that accumulates a cash surrender value, Medicaid does count it as an asset if the death benefit (face value) exceeds a certain threshold, typically $1,500. If it exceeds this limit, you may be required to cash out the policy and spend down the proceeds on your care before you can qualify for benefits.

For official financial guidance for seniors, visit

Centers for Medicare & Medicaid Services (CMS), Consumer Financial Protection Bureau (CFPB), IRS.gov, Benefits.gov and AARP.

Disclaimer: This article is for informational purposes and is not a substitute for professional financial or tax advice. Consult with a certified financial planner or tax professional for guidance on your specific situation.

Leave a Reply