Managing your money on a fixed income requires constant vigilance. When inflation drives up the cost of groceries, utilities, and healthcare, the standard cost-of-living adjustments to your Social Security benefits rarely feel like enough to bridge the gap. You already know to ask for a senior menu at a local restaurant or a discounted ticket at the movie theater, but relying on small, incidental markdowns will not fundamentally change your monthly budget.

The most impactful senior discounts are rarely advertised on a storefront window. They are buried in municipal tax codes, hidden within utility company policies, and nested deep inside federal benefit programs. These high-value savings require a bit of paperwork and persistence, but the payoff is substantial. By strategically applying for these lesser-known programs, you can permanently lower your recurring expenses, keeping more of your retirement savings in your bank account where they belong.

You have earned the right to utilize these financial advantages. The key is knowing where to look, what to ask for, and how to navigate the application processes. Below, you will find a breakdown of seven major discount categories that go far beyond a cheap cup of coffee, offering concrete ways to reduce your largest annual expenses.

Auto Insurance and Defensive Driving Discounts

Vehicle insurance premiums often creep up steadily year after year, even if your driving record remains flawless. Many older adults simply pay their renewal bills without realizing they qualify for substantial age-based premium reductions. One of the most reliable ways to slash your auto insurance costs is by completing a mature driver safety course.

Dozens of states legally mandate that insurance companies provide a multi-year premium discount to drivers over a certain age—typically 50 or 55—who complete an approved defensive driving class. These courses refresh your knowledge of traffic laws, teach strategies for adapting to age-related physical changes, and usually take only a few hours to complete online or in person.

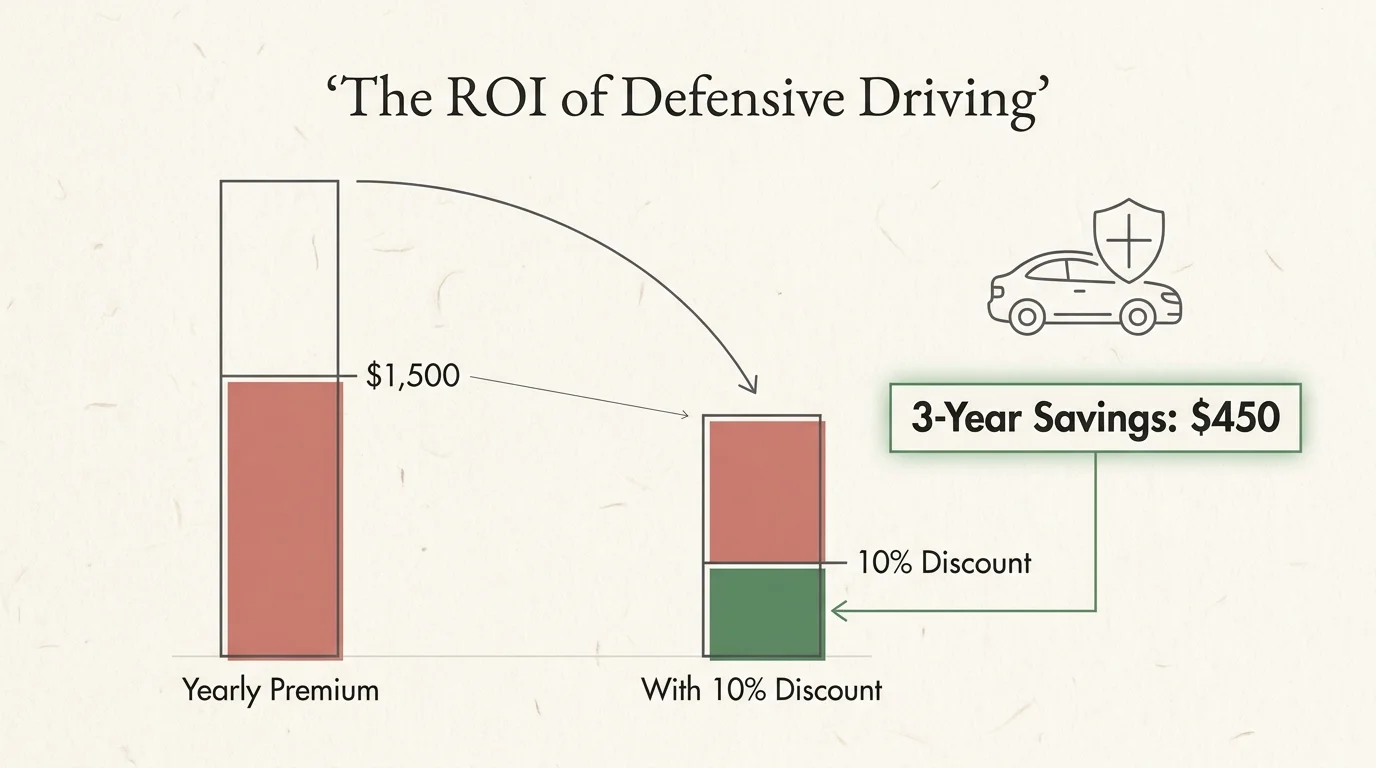

Organizations like AARP offer state-approved Smart Driver courses that can trigger these mandatory insurance rate reductions. The math heavily favors taking the class. If you pay $1,500 annually for car insurance, a standard 10% discount saves you $150 a year. Because the discount usually applies for three consecutive years before you need to retake the course, a $20 to $25 class fee translates into $450 in total savings.

Additionally, you should call your insurance agent to update your annual mileage. If you are retired and no longer commuting to a daily job, your annual mileage has likely plummeted. Transitioning from a “commuter” profile to a “pleasure use” profile often triggers an automatic drop in your premium.

Property Tax Exemptions and Freezes

For seniors who own their homes, property taxes represent a massive, unpredictable burden. As local real estate values climb, your tax bill climbs with them, creating a dangerous scenario when your income remains flat. Fortunately, local governments frequently offer substantial property tax relief programs exclusively for older adults, though they rarely advertise them directly to homeowners.

These relief programs generally fall into three categories:

- Senior Exemptions: A flat reduction in the assessed value of your home. For example, if your home is assessed at $300,000, a $50,000 senior exemption means you only pay taxes on $250,000.

- Property Tax Freezes: These programs lock your property’s assessed value or your actual tax bill at the amount it was the year you turned a qualifying age (usually 65). Even if your home doubles in value over the next decade, your tax bill remains anchored to that baseline year.

- Tax Deferrals: This allows you to postpone paying some or all of your property taxes until your home is sold or your estate is settled. While this does not erase the debt, it provides immediate cash flow relief for those struggling to cover daily living expenses.

Because property taxes are handled at the county or municipal level, the rules vary wildly depending on your zip code. Most programs enforce strict income limits to qualify, and you must apply proactively through your county tax assessor’s office. Make it a priority to search your local tax assessor’s website for terms like “homestead exemption,” “senior freeze,” or “elderly tax relief.”

Utility Bill Assistance and Weatherization

Heating and cooling your home accounts for a massive portion of your monthly expenses. Utility providers and government programs offer multiple layers of financial assistance for seniors, yet many older adults assume they do not qualify because they are not completely impoverished.

Start by contacting your local electric and gas providers directly. Many mandate a reduced base rate or waive monthly service fees for customers over the age of 60 or 65. You simply have to call their billing department, prove your age, and ask to be placed on the senior tariff.

For more substantial savings, look into the Low Income Home Energy Assistance Program (LIHEAP). This federally funded initiative helps low-income households cover heating and cooling costs. Depending on your state’s specific income limits, LIHEAP can provide hundreds of dollars a year paid directly to your utility company on your behalf.

Beyond direct bill payment, the Weatherization Assistance Program (WAP) provides free home energy upgrades. If you qualify, contractors will upgrade your insulation, seal drafty windows, and tune up your HVAC system at zero cost to you. According to Benefits.gov, you can locate exact eligibility requirements and application portals for these energy assistance grants in your specific state. Fixing a drafty house permanently lowers your utility bills for the rest of your retirement.

Unadvertised Healthcare and Prescription Savings

Medicare covers a significant portion of your healthcare, but the out-of-pocket costs for premiums, deductibles, and prescription drugs can easily drain your savings. Identifying hidden healthcare discounts requires a multifaceted approach.

First, evaluate the Medicare Part D Extra Help program. This federal initiative helps people with limited income and resources pay Medicare prescription drug program costs, including premiums, deductibles, and coinsurance. Data from Medicare.gov outlines that qualifying for Extra Help is estimated to save beneficiaries roughly $5,300 per year. Even if you were denied in the past, income limits adjust annually, making it worth reapplying.

If you do not meet the strict income limits for federal assistance, you can still save heavily through State Pharmaceutical Assistance Programs (SPAPs). Many states operate their own secondary programs to help middle-income seniors afford necessary medications.

Furthermore, do not pay cash for expensive brand-name drugs without checking manufacturer assistance programs. Pharmaceutical companies often run patient assistance foundations that provide expensive medications for free or at a steep discount to seniors who lack adequate Part D coverage. You can usually find the application for these programs on the drug manufacturer’s official website.

Internet and Cellular Lifeline Programs

Staying connected with family, accessing telehealth services, and managing your finances online are not luxuries; they are necessities. Yet, seniors frequently overpay for massive data plans and high-speed internet packages they simply do not need.

Almost every major cellular provider offers a “55+” or “60+” discounted plan, but they rarely market them aggressively. If you currently pay $85 a month for a standard single-line cellular plan, switching to a provider’s senior-specific tier can drop that bill to $40 or $50 a month, saving you roughly $400 a year without changing your phone number or sacrificing coverage.

For those living on a strict low income, the federal Lifeline program provides a monthly discount on communications services. Lifeline offers a subsidy of up to $9.25 per month toward telephone or broadband internet service (and up to $34.25 for those living on Tribal lands). While $9.25 may sound small, many participating telecommunications providers offer specific, low-cost plans designed to cost exactly $9.25, effectively making your basic phone or internet service completely free.

Take an hour this week to review your current data usage on your cell phone and home internet bills. If you only use Wi-Fi at home and rarely stream video on the go, downgrade your plan and demand the senior rate.

Lifetime Recreational and National Park Passes

Maintaining an active, engaging lifestyle in retirement helps preserve both physical and mental health. While travel can be expensive, recreational discounts offer incredible value for seniors who enjoy the outdoors.

The crown jewel of senior discounts is the America the Beautiful National Parks & Federal Recreational Lands Senior Pass. Available to U.S. citizens or permanent residents age 62 or older, this lifetime pass costs an $80 one-time fee (plus a small processing fee if ordered online). Compare this to the standard annual pass, which costs $80 every single year.

The lifetime senior pass covers entrance fees at thousands of federal recreation sites across the country, including all National Parks, national wildlife refuges, and national forests. More importantly, the pass provides a 50% discount on expanded amenity fees. This means half-price access to federal campsites, swimming areas, and boat launches. If you plan to travel by RV or camp during your retirement, this pass will pay for itself on your first major road trip.

Do not forget to check your state park system as well. Many states offer free or heavily discounted lifetime passes to residents over 65, granting free parking and discounted lodging at state-level natural reserves.

Retail and Grocery Age-Threshold Strategies

The landscape of retail senior discounts has shifted over the last decade. Blanket “10% off for seniors” signs are disappearing, replaced by loyalty programs and specific “senior days.” To maximize these savings, you must understand the rules of the stores you frequent.

Many major grocery chains designate a specific day of the week or the first Tuesday of the month as their senior discount day, offering 5% to 10% off your total basket. Because groceries are a massive recurring expense, consolidating your shopping trips to align with these days yields serious returns.

Keep in mind that cashiers rarely apply these discounts automatically. You must verbally declare your eligibility at checkout. Age thresholds also vary wildly; some stores consider 55 the starting point for senior status, while others require you to be 60 or 65.

To visualize the impact of combining just a few of the strategies discussed in this guide, review the estimated annual savings potential below:

| Discount Category | Action Required | Estimated Annual Savings |

|---|---|---|

| Auto Insurance | Complete an approved defensive driving course. | $100 – $250 |

| Property Tax Relief | Apply for county homestead exemption or freeze. | $300 – $1,200+ |

| Cellular Service | Switch to a 55+ unlimited talk/text/data plan. | $300 – $600 |

| Grocery Shopping | Consolidate purchases on 10% off senior days ($400/mo spend). | $480 |

| Potential Total | Implementing these four core strategies. | $1,180 – $2,530+ |

Avoiding Senior Discount and Benefit Scams

Wherever there is an opportunity to save money, unscrupulous actors will attempt to take advantage. Scammers specifically target older adults with fake discount programs, counterfeit benefit cards, and deceptive medical alert services.

The most common pitfall is the “fee for free discount” scam. You may receive an official-looking letter or email offering you a “Premium Senior Savings Card” that promises 50% off groceries and utilities for a one-time processing fee of $49. Legitimate municipal, state, and federal discount programs never charge processing fees to apply for benefits.

Furthermore, fiercely protect your personal information. As noted by the Consumer Financial Protection Bureau (CFPB), older adults are frequent targets of financial exploitation. If a representative from a “discount club” calls you out of the blue and demands your Social Security number or Medicare number to verify your eligibility for a grocery markdown or utility credit, hang up immediately. Real utility companies already have your account details, and legitimate retail discounts only require a flash of your driver’s license at the register.

Always verify the legitimacy of a program by going directly to the official source. If someone claims they can lower your property taxes for a fee, bypass them entirely and call your county tax assessor directly to learn about the actual, free application process.

Frequently Asked Questions

How do I know if I qualify for low-income senior discounts?

Income limits vary dramatically depending on the specific program and your geographic location. Federal programs like Extra Help or LIHEAP rely on specific percentage thresholds of the Federal Poverty Level. Local property tax freezes often look at your household’s Adjusted Gross Income (AGI) from your previous year’s tax return. The best approach is to contact your local Area Agency on Aging or visit your state’s Department of Health and Human Services website to view the exact income tables for your region.

Do I have to ask for a senior discount, or is it applied automatically?

You must almost always ask. Whether you are paying a cashier at a grocery store, booking a hotel room, or setting up a new cell phone plan, assume the discount will not be applied automatically. Cashiers are often instructed not to assume a customer’s age to avoid causing offense. Always present your ID and explicitly ask, “Do you offer a discount for seniors over 55 or 65?”

Are paid senior discount memberships worth the cost?

It depends entirely on your spending habits. Paid memberships like AARP cost a small annual fee but provide access to substantial discounts on car rentals, hotels, restaurant chains, and cellular plans. If you travel frequently or dine out often, the membership pays for itself quickly. However, if you rarely travel and spend most of your money on basic groceries and utilities, a paid membership may not yield enough return to justify the upfront cost. Always review the exact list of participating vendors before paying a membership fee.

What age qualifies as a “senior” for most discounts?

There is no universal standard. Retailers and restaurants often set the bar at 55 or 60 to attract early retirees. Federal programs like Medicare require you to be 65. The National Parks pass activates at 62. Because the threshold fluctuates so wildly, you should start asking about age-based discounts the moment you turn 55, as you may be leaving money on the table for a decade if you wait until 65.

Does Medicare offer any specific discounts on everyday items?

Original Medicare (Parts A and B) does not offer retail discounts. However, if you are enrolled in a Medicare Advantage (Part C) plan, you may have access to an Over-the-Counter (OTC) benefit. These plans often provide a pre-loaded debit card or a quarterly allowance—sometimes $50 to $100 every three months—that you can spend at local pharmacies on everyday health items like vitamins, pain relievers, bandages, and toothpaste. Check your specific Advantage plan’s summary of benefits to see if you have this allowance.

For official financial guidance for seniors, visit AARP, National Institute on Aging (NIA) and Administration for Community Living (ACL).

Disclaimer: This article is for informational purposes and is not a substitute for professional financial or tax advice. Consult with a certified financial planner or tax professional for guidance on your specific situation.

Leave a Reply