1. Maximize Your Social Security Returns

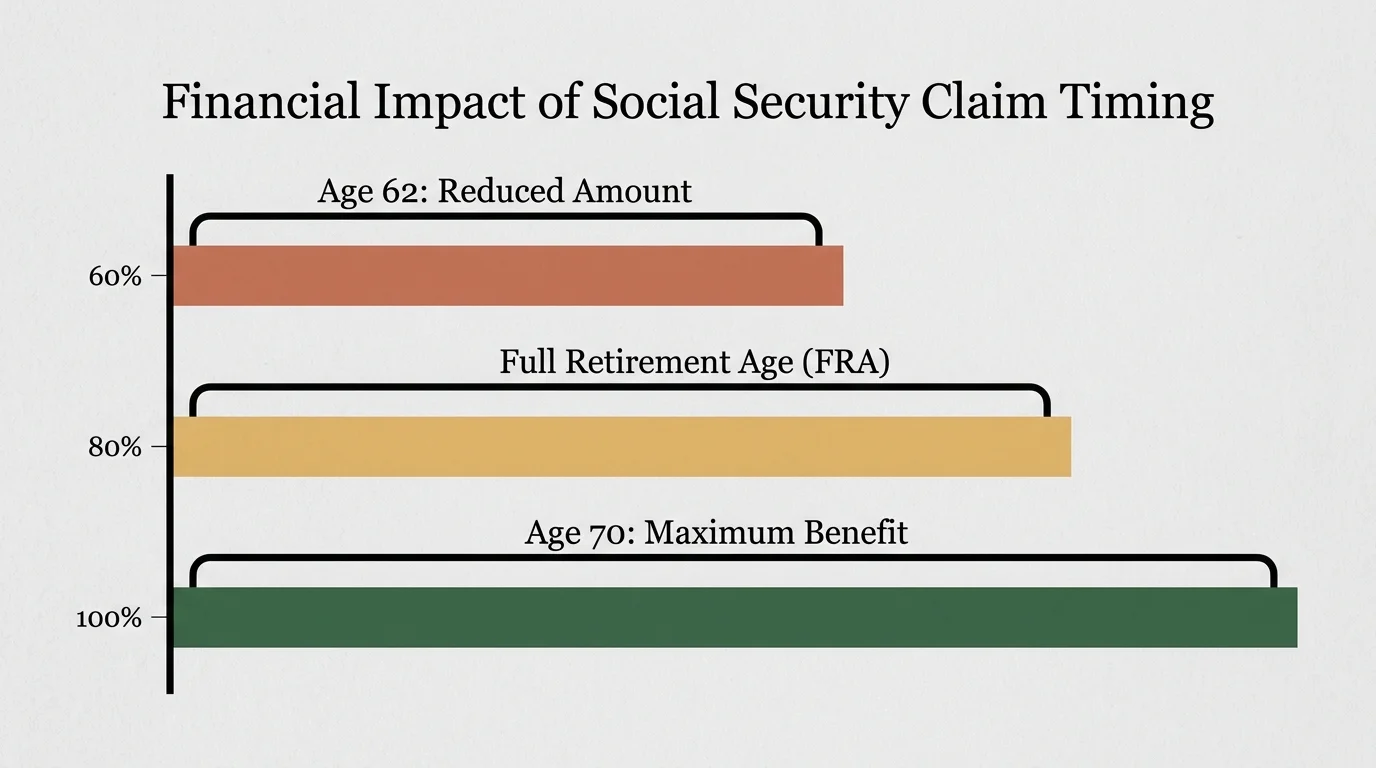

Your Social Security benefit serves as the foundation of your retirement income. However, the age at which you choose to start collecting dramatically impacts your monthly check for the rest of your life. If you were born between 1941 and 1969, you face a critical decision: claim early at 62 for a reduced amount, wait until your Full Retirement Age (FRA), or delay claiming to maximize your payout.

According to the Social Security Administration (SSA), delaying your claim beyond your Full Retirement Age increases your benefit by 8% for every year you wait, up until age 70. This guaranteed return easily outperforms most conventional investments. If you claim at age 62, you could face a permanent reduction of up to 30% on your monthly payments.

Consider your health status, life expectancy, and current financial needs before claiming. If you plan to continue working, claiming early might trigger the earnings test, which temporarily withholds some of your benefits. You should create an online account on the SSA website to review your personalized statements and calculate the exact difference between claiming early and waiting.

Leave a Reply