Managing Your Earnings and Retirement Benefits

Earning extra money is a wonderful perk, but you must understand how your new paycheck affects your fixed retirement income. If you are not careful, working could temporarily reduce your government benefits or push you into a higher tax bracket.

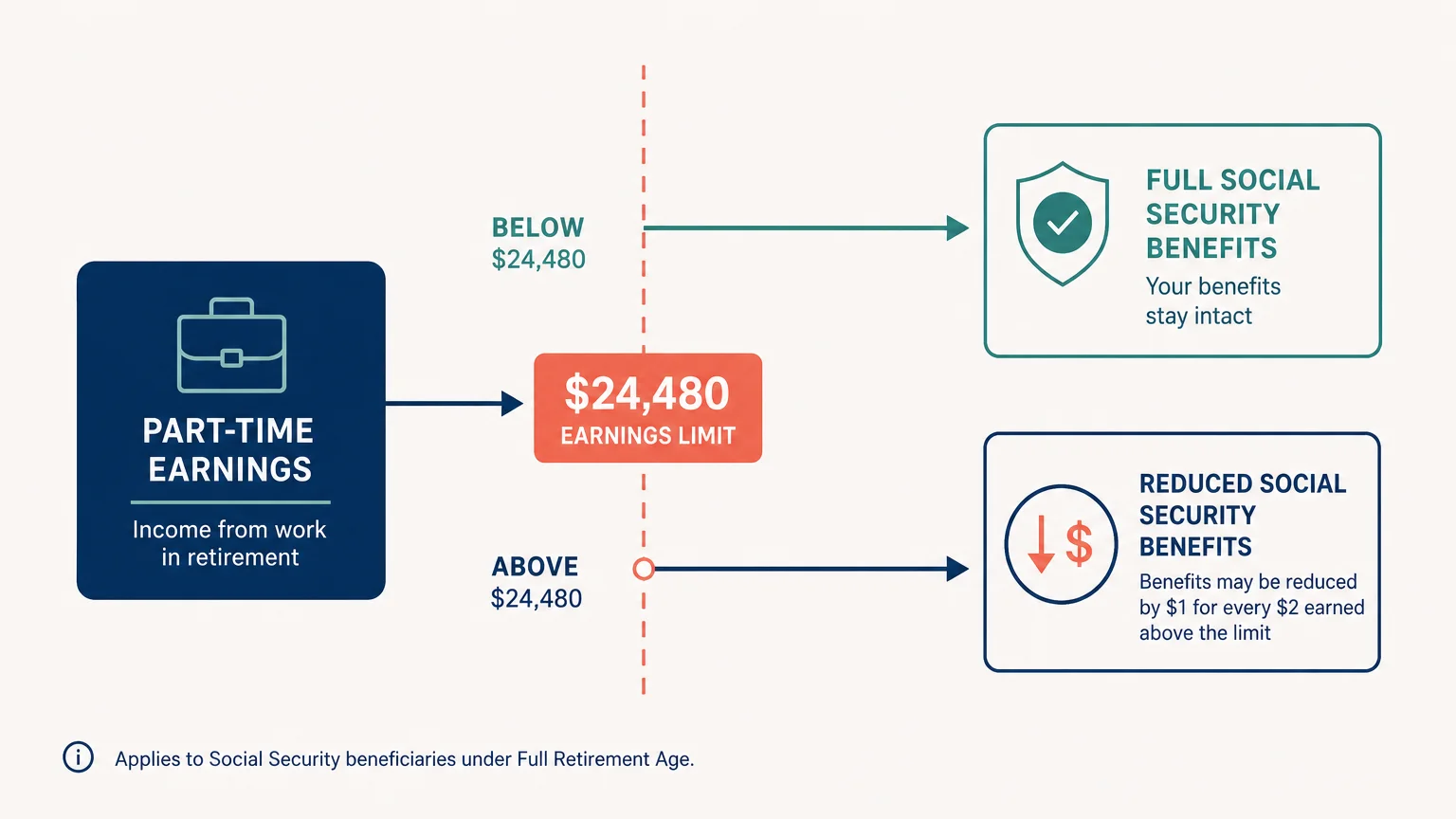

According to the Social Security Administration (SSA), if you claim benefits before your full retirement age and earn above a specific yearly limit, a portion of your monthly benefit will be temporarily withheld. The SSA adjusts this earnings limit annually. For example, if you exceed the limit, they deduct $1 from your benefit payments for every $2 you earn above the annual threshold. However, this money is not lost forever; once you reach your full retirement age, the SSA recalculates your benefit amount to give you credit for the months your benefits were withheld. Once you reach full retirement age, you can earn as much as you want without any reduction in your Social Security checks.

Additionally, remember that your wages are taxable. Earning part-time income could increase your combined income to a level where a larger portion of your Social Security benefits becomes subject to federal income tax. Consult a tax professional to determine exactly how many hours you should work to maximize your social benefits without unnecessarily complicating your tax situation.

I am interested, although, I do have bad knees and back problem, that may limit, the extent of my physical activity.

However, I am not limiting myself. Even though, I am concentrating, currently, on ‘Work from home’ – Remote jobs search.

I am interested in taking a part time job.

I am looking for a remote position that allows me to work from home. I have a very bad back and can hardly walk. I can do customer service. I can work about 20 hours a week.

I am interested in a part time remote position if you can assist with this option.