Where you live during your working years significantly shapes your financial security in retirement. Your Social Security benefit relies entirely on your lifetime earnings, meaning retirees from states with higher average wages receive substantially larger monthly checks. Currently, retirees in states like New Hampshire, Connecticut, and Maryland take home the highest average Social Security payments in the country. However, a larger check often comes with a higher cost of living and heavier tax burdens. Understanding the relationship between geography, lifetime income, and your final benefit amount empowers you to make smarter financial decisions. You can maximize your retirement income—regardless of your zip code—by strategically timing your claim and avoiding the common financial pitfalls that catch many seniors off guard.

Why Your Working Location Influences Your Social Security Income

It is a common misconception that the government adjusts your retirement check based on the state you live in. The reality is far more straightforward, though deeply tied to geography. Your Social Security benefit is a reflection of your career earnings, not your current mailing address. States with robust economies, major metropolitan hubs, and specialized industries naturally offer higher salaries to their workers. When you spend decades earning a high salary in states like Connecticut or New Jersey, you pay more into the Social Security system.

According to the Social Security Administration (SSA), your monthly benefit is calculated using your 35 highest-earning years in the workforce. The agency adjusts your historical earnings for inflation and determines your Average Indexed Monthly Earnings (AIME). From there, a standard formula is applied to establish your Primary Insurance Amount (PIA)—the base amount you will receive if you claim benefits at your exact Full Retirement Age. Because residents of high-cost states generally command larger paychecks to afford housing and basic needs during their working years, their lifetime earnings records are mathematically higher. Consequently, their eventual retirement benefits are larger than those of individuals who spent their careers in states with lower median incomes.

The Top 10 States With the Highest Average Monthly Checks

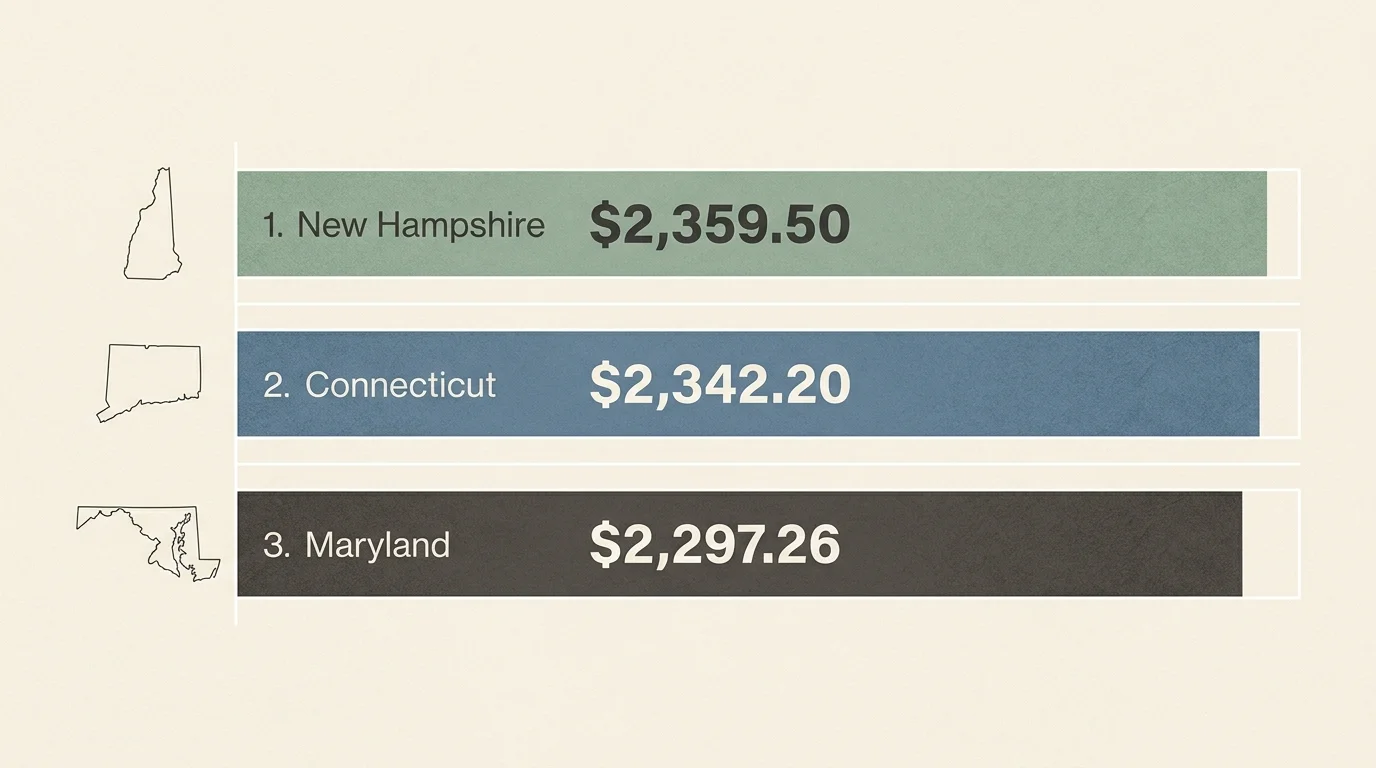

Recent data reveals a clear geographic trend when it comes to retirement income. The states with the highest average Social Security checks are heavily concentrated in the Northeast and Mid-Atlantic regions. These areas historically feature a high concentration of advanced industries, corporate headquarters, and technical professions that pay premium salaries. By examining the national data, you can see exactly which states produce the most substantial retirement benefits.

| Rank | State | Average Monthly Social Security Benefit |

|---|---|---|

| 1 | New Hampshire | $2,359.50 |

| 2 | Connecticut | $2,342.20 |

| 3 | Maryland | $2,297.26 |

| 4 | New Jersey | $2,291.59 |

| 5 | Delaware | $2,251.59 |

| 6 | Massachusetts | $2,243.46 |

| 7 | Minnesota | $2,228.27 |

| 8 | Washington | $2,210.17 |

| 9 | Rhode Island | $2,192.99 |

| 10 | Virginia | $2,178.00 |

While an average check of over $2,300 per month sounds appealing, it is important to remember that these numbers represent the average. Many retirees in these states receive significantly more, while others collect much less, depending entirely on their personal work histories and the exact age they decided to claim their benefits.

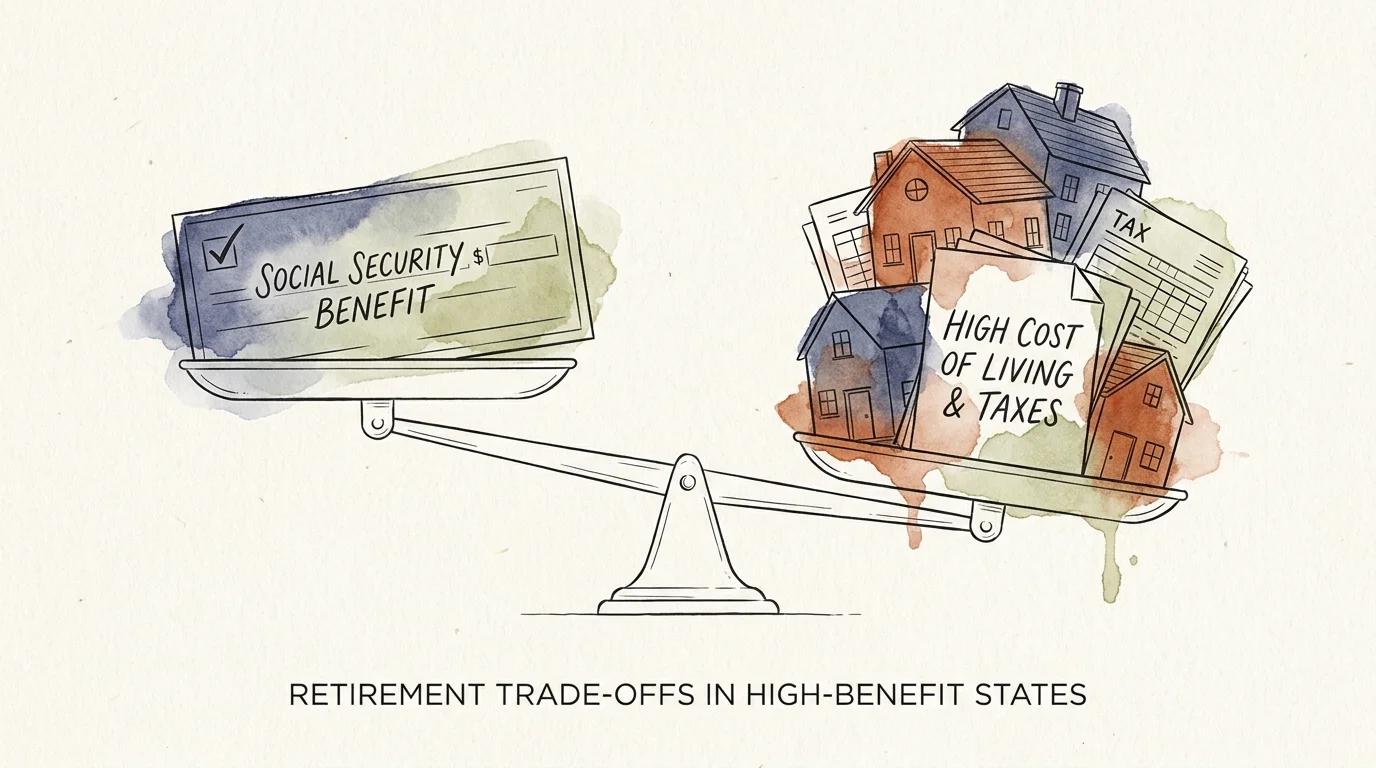

The Hidden Catch of High-Benefit States

Receiving a larger Social Security check does not automatically guarantee a comfortable retirement. In fact, many seniors in top-ranking states face severe financial pressure. A monthly check of $2,300 in New Hampshire or Massachusetts simply does not have the same purchasing power as a $1,800 check in Mississippi or Arkansas. The states that produce the highest lifetime earnings are almost always the states with the highest ongoing costs for housing, property taxes, healthcare, and everyday groceries.

Furthermore, managing a tight budget in an expensive region can take a heavy toll on your overall well-being. Studies by the National Institute on Aging (NIA) indicate that chronic financial stress can lead to severe health outcomes, including accelerated cognitive decline and cardiovascular issues. Worrying about how to pay high property taxes on a fixed income creates a cycle of anxiety that prevents seniors from enjoying their golden years.

Another crucial factor is state-level taxation. While the federal government taxes Social Security benefits if your provisional income exceeds certain thresholds, individual states have their own rules. A handful of states—including Connecticut and Rhode Island, which appear in the top 10 list—still tax Social Security benefits for some residents. This means that a portion of that larger average check may go straight back to the state revenue department, shrinking your actual take-home pay.

Will Relocating in Retirement Change Your Monthly Payment?

One of the most persistent myths among retirees is that moving to a new state will prompt the government to adjust their Social Security payment. You can rest easy knowing that your benefit amount is locked in based on your lifetime earnings and your claiming age. If you retire in New Jersey with a $2,400 monthly benefit and subsequently move to South Carolina, your check will remain exactly $2,400.

This reality is driving a massive wave of retiree migration. Thousands of seniors are choosing to earn their high salaries in expensive coastal states and then move to the Sunbelt or the Midwest to stretch their retirement dollars further. By keeping a large Northeast-sized benefit but adopting a Southern cost of living, you can dramatically improve your financial comfort. If you are considering a move to stretch your Social Security income, you should carefully evaluate several factors beyond just the cost of housing.

- Healthcare Quality and Access: Ensure your new location has robust medical facilities and specialists who accept your specific Medicare coverage.

- Tax Friendliness: Look for states that do not tax Social Security benefits, pensions, or withdrawals from retirement accounts.

- Proximity to Support Networks: Relocating far from family and longtime friends can lead to isolation, which presents its own health risks as you age.

- Transportation Options: Consider whether the new city offers reliable public transit or senior transport services, as driving may become difficult later in life.

Proven Strategies to Maximize Your Own Benefit Amount

You do not need to live in New Hampshire or Connecticut to secure a substantial retirement check. The most powerful levers for increasing your Social Security income are entirely within your control. As noted by experts at the Consumer Financial Protection Bureau (CFPB), deciding when to claim your retirement benefits is one of the most critical financial choices you will ever make. To ensure you receive the highest possible payout, consider implementing the following strategies.

- Work for a Full 35 Years: Because your benefit is calculated based on your 35 highest-earning years, any missing years are entered into the calculation as zeros. Even a few years of zeros will significantly drag down your average. If you only have 32 years of work history, working three more years—even part-time—can visibly boost your permanent benefit.

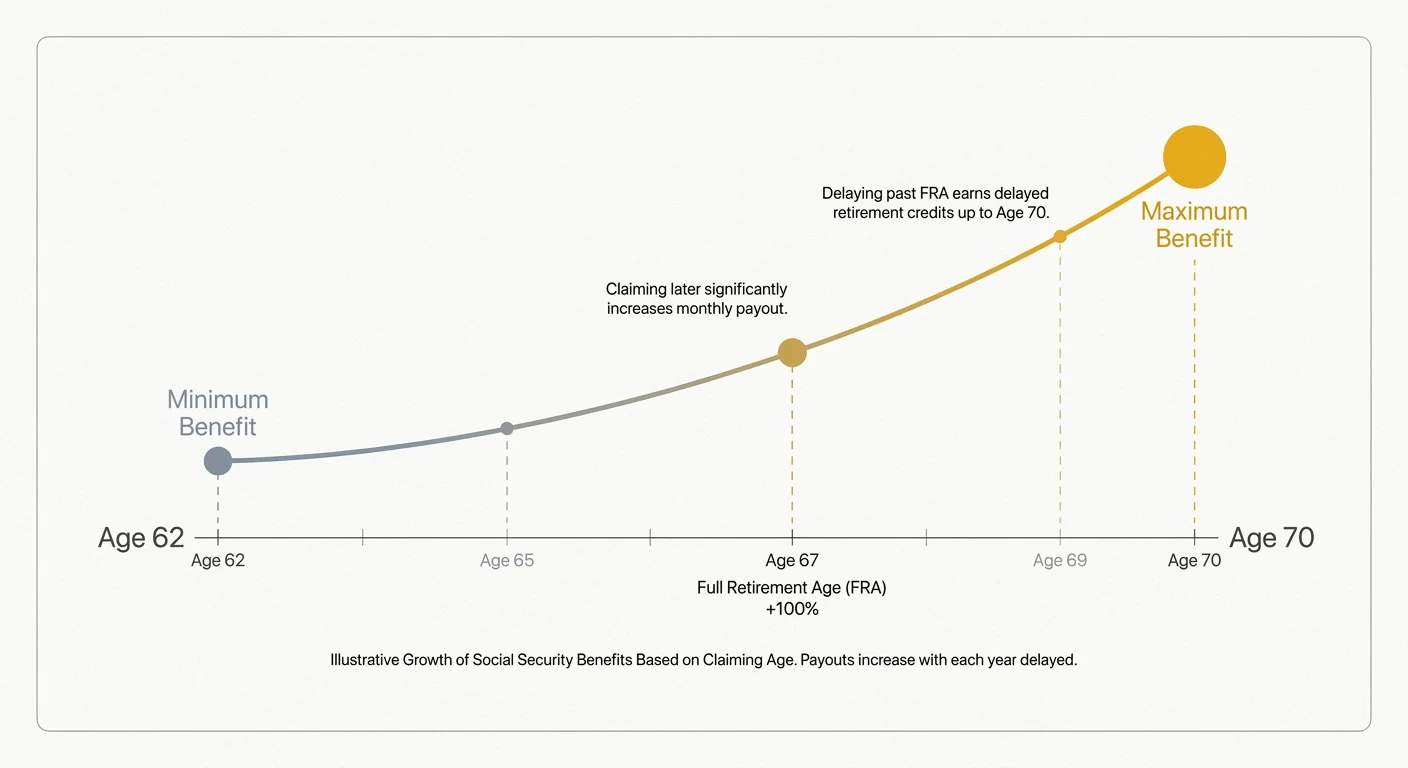

- Delay Claiming Past Full Retirement Age: You can claim benefits as early as age 62, but doing so permanently reduces your monthly check by up to 30%. Conversely, if you delay claiming beyond your Full Retirement Age (usually 66 or 67, depending on your birth year), your benefit grows by 8% for every year you wait, up until age 70. This guaranteed 8% annual return is one of the safest ways to increase your fixed income.

- Audit Your Earnings Record: Mistakes happen. Employers can misreport your income, or clerical errors can occur. You should create a free account on the Social Security website and review your earnings record annually. If you spot a year where your income is listed incorrectly, you can file a correction to ensure you get the full credit you deserve.

- Coordinate Spousal Benefits: If you are married, divorced, or widowed, you may be entitled to claim benefits based on your spouse’s earnings record rather than your own. In some cases, a spousal benefit can provide a larger monthly check than your personal work history, especially if your spouse was the primary breadwinner.

Common Financial Pitfalls for Retirees on Fixed Incomes

Navigating the transition to a fixed income requires careful planning and a realistic view of future expenses. Many seniors stumble into predictable traps that reduce their monthly cash flow and create unnecessary hardship. One of the most common mistakes is claiming benefits early out of fear that the Social Security trust funds will dry up. While the system does face long-term funding challenges, taking a permanent 30% reduction in your monthly income to secure early checks is rarely the best mathematical choice if you are in good health and have a normal life expectancy.

Another major oversight involves the hidden costs of healthcare. Many new retirees assume their Social Security check is entirely theirs to spend. However, experts at Medicare.gov clarify that standard Medicare Part B premiums are automatically deducted from your Social Security payments before the money ever hits your bank account. If you estimate your household budget based on your gross Social Security benefit, you will find yourself short on cash every month when the net deposit arrives.

Finally, working while receiving early retirement benefits trips up countless seniors. If you claim Social Security before your Full Retirement Age and continue to work, you are subject to the earnings test. If you earn more than the annual limit, the government will temporarily withhold a portion of your benefits. While you do get this money back eventually in the form of a recalculated benefit at Full Retirement Age, the sudden loss of monthly income can disrupt your budget severely. Always understand the earnings limits before deciding to mix part-time work with early Social Security claims.

Frequently Asked Questions

Does my Social Security check change if I move to a different state?

No. Your Social Security benefit amount is calculated based on your lifetime earnings record and the age at which you choose to claim. Relocating to a new state during your retirement will not cause your monthly payment to increase or decrease.

Are Social Security benefits taxed at the state level?

It depends entirely on where you live. While the majority of states do not tax Social Security benefits, there are several states that still do, though many have implemented exemptions based on your income level. You should consult a tax professional or review your state’s specific tax code to understand how your benefits will be treated.

At what age should I claim Social Security to get the maximum amount?

To receive the absolute highest monthly benefit available to you, you must wait until age 70 to claim. Delaying your claim past your Full Retirement Age earns you delayed retirement credits, which increase your base benefit by 8% for every year you wait. There is no financial advantage to delaying past age 70.

How does the Social Security Administration calculate my benefit?

The agency reviews your entire lifetime earnings history, indexes your past wages to account for inflation, and selects your 35 highest-earning years. They average those 35 years to find your Average Indexed Monthly Earnings (AIME) and then apply a standard formula to determine your Primary Insurance Amount.

Can I increase my benefit once I start receiving it?

Generally, your benefit amount is locked in once you begin claiming. However, there are two main exceptions. First, annual Cost-of-Living Adjustments (COLA) will incrementally increase your check to help keep pace with inflation. Second, if you continue to work while collecting benefits and your current earnings replace one of your lowest-earning years in your 35-year record, the SSA will automatically recalculate and increase your benefit the following year.

For additional senior resources, visit

Benefits.gov, National Institute on Aging (NIA), Centers for Disease Control and Prevention (CDC) and Medicare.gov.

Disclaimer: The information in this article is for educational purposes only and is not intended to be a substitute for professional financial, legal, or medical advice. Always consult with a qualified expert for advice tailored to your personal situation.

Leave a Reply